The EU failed to pass a proposed ban on proof-of-work crypto mining (e.g. Bitcoin mining)

Russia decided against banning crypto or crypto mining (possibly motivated by the sanction-bypassing ability of public blockchains while the Ukraine war is ongoing)

India decided against banning crypto (deciding instead to impose a hefty tax on both net income and transactions related to crypto)

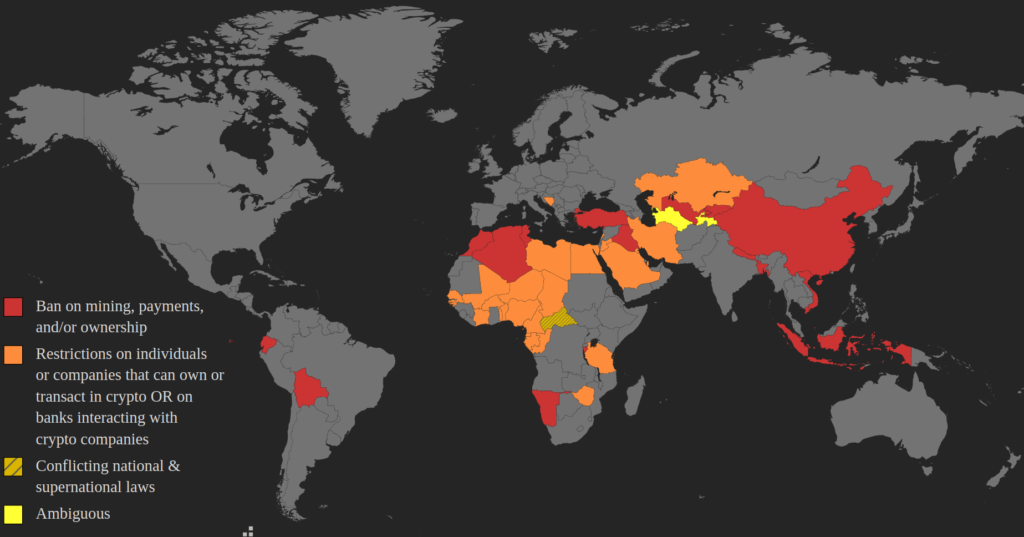

Neverthless, many countries have imposed bans or significant legal restrictions on crypto ownership, transactions, mining, and/or the ability of crypto companies to interact with banks. Here’s a map showing the current state of which countries have imposed some level of ban or restriction on crypto:

Color-coded map of countries that banned or restricted the use of cryptocurrencies

List of Countries with Bans or Restrictions

Algeria

Bangladesh

Bolivia

Burundi

China

Ecuador

Indonesia (religious law, but criminally enforced in some areas)

Iraq

Kyrgyzstan

Morocco

Namibia

Nepal

Tunisia

Turkey

Uzbekistan

Vietnam

Benin

Bosnia and Herzegovina

Burkina Faso

Cameroon

Chad

Congo

Côte d’Ivoire

Egypt

Equatorial Guinea

Gabon

Guinea-Bissau

Iran

Jordan

Kazakhstan

Kuwait

Lebanon

Libya

Mali

Niger

Nigeria

Saudi Arabia

Senegal

Tanzania

Togo

Qatar

Zimbabwe

Central African Republic

Turkmenistan

Tajikistan

References

Crypto laws & regulations have been changing at lightning speed across the globe during the past two years, which means each of the references below is no longer accurate. However, they provide a useful starting point and link to other resources that you can use to do your own research if you need to find the current legal situation in a particular country.

“That’s a pretty interesting result to anyone running a hedged long/short investment portfolio, especially with energy prices so high. It also means that if I personally held any private stock in Crypto.com, I’d be looking to offload it as quickly as possible since its stadium deal structure didn’t meet our “high-quality deal criteria”.

American Airlines Arena before its rebrand to FTX Arena in 2021

In January 2021, the fintech company “Q2 Holdings, Inc.” agreed to pay an estimated $26 million to name a Texas major league soccer stadium “Q2 Stadium”. That was just the beginning of what became a record-setting year for stadium name deals. Some of the largest deals included:

Intuit buying the naming rights to the L.A. Clippers’ new arena for $500 million

FTX buying the naming rights to the Miami Heat’s home arena for $135 million

Crypto.com buying the naming rights to the L.A. Lakers’ home arena for $700 million

These companies are willing to shell out massive piles of cash in order to build their brand and market themselves as important, trustworthy companies. However, given the massive size of the expenditures, it’s worth the time of any investor, executive, or board member of one of these companies to quantitatively estimate the ROI. In this article, I do exactly that by pulling data from SEC filings, historical stock performance, local government records of cities that have stadiums, company announcements, and media coverage of sponsorship deals. By the end of this article, you will know:

How companies that bought stadium naming rights in the past have performed relative to their competitors and the overall market.

How to know if you should sell a company that announces a naming rights purchase.

How to decide whether a company you run or advise should buy the naming rights to a sports venue (e.g. high school stadium, college stadium, major league stadium, etc).

Let’s jump in.

What do you actually get when you buy “naming rights”?

A naming rights deal is about intangible assets. A typical deal might include the sale of something like this list of assets:

The right to specify the name of the stadium

The right to have your chosen stadium name and/or your company logo written up to a certain size on various parts of the stadium’s exterior (e.g. the roof and/or over the main entrance)

The right to various signage throughout the interior and exterior of the stadium for use as advertisements

The right to advertise your company as “the official provider of <thing or service> to <name of team that uses the stadium>”

The right to have certain parts of the stadium painted and/or lit with your company’s colors

The right to have the stadium name used in all official press releases of the stadium’s home team

The right to have the in-game announcer say the stadium name and/or other sponsored messages about your company a certain number of times throughout every home game

The right to have your company logo and/or name on the backdrop of certain press conferences held at the stadium

The right to exclude anyone else from advertising on or within certain parts of the stadium

Discounted options on buying certain TV commercial slots during televised games

The right to use certain retail or vendor spots within the stadium and/or adjacent buildings

The right to exclude competitor companies from advertising in the stadium and/or adjacent buildings

Of course, deals will differ from one to another, but that list gives a pretty good idea of the type of assets that are often included in a naming rights purchase agreement.

How stadium name deals are structured

With rare exceptions, stadium names are not paid for with a single lump sum. Instead, the headline dollar amount (e.g. “SoFi buys stadium naming rights for $625 million”) is actually paid in quarterly installments over the course of decades. For instance, SoFi’s purchase will be paid over the course of 20 years.

Equally important to know is that despite these deals being referred to as “purchases”, naming rights are almost never actually purchased — they are rented. Returning to the example of SoFi, the “purchase” agreement is actually an agreement for the stadium to have the name “SoFi Stadium” for 20 years (i.e. the same length of time that SoFi is making payments). In other words, SoFi agreed to rent the intangible asset of “naming rights” for the L.A. stadium for about $30 million per year, for 20 years. That is a hefty subtraction of free cash flow for a very long time. And as anyone who has owned a business knows, free cash flow is the lifeblood of a company.

To accept that kind of rigid constraint, you better be damn sure that the ROI you’ll get will be substantially better than what you’d get from instead using an elastic marketing budget on digital ads. If a $30 million Facebook ad campaign doesn’t work, you can shut it off in a day and only lose $82,000. If a $30 million stadium marketing campaign doesn’t work, you’re stuck with not just $30 million this year but also for the next 19 years. That’s a lot of risk which can meaningfully degrade a company’s long-term performance if taken recklessly. However, an even more significant consideration is that how a company’s management team makes one $100M+ budget decision reflects on how they make all decisions. If stadium names don’t provide a good ROI, then a company that buys them probably makes lots of other bad purchases too. If stadium names *do* provide a good ROI, then a company that buys them probably has good decision making processes in place, which means they’re likely to make other good decisions as well. To figure out which situation is more likely, let’s take a look at the historical ROI of some companies that have bought stadium naming rights in the past.

These companies were randomly sampled from the set of publicly traded U.S. companies which are current or recently terminated sponsors of NFL stadiums, have been public for the majority of the deal duration, and have been involved in the deal for at least 5 years. The time window over which each company is analyzed starts briefly before major news coverage of the deal began. The time windows all end in 2022. The stock performance of each company (adjusted for any splits and dividends) is compared against various benchmarks such as the S&P 500, a subset of closest competitors, and same-sector ETFs which have existed throughout the entire time window under study.

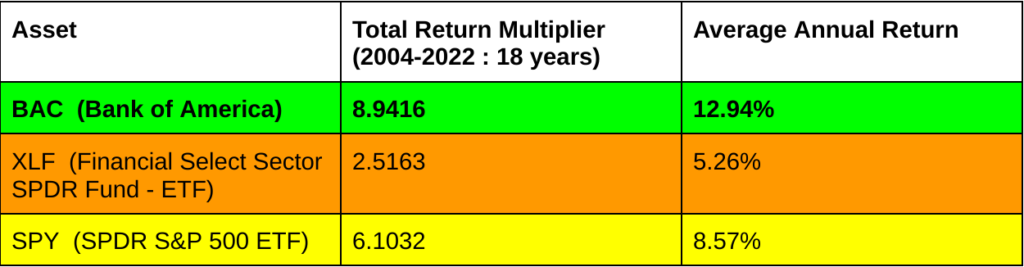

Case Study 1: Bank of America

VERDICT: Overperformed

Substantially outperformed S&P 500

Substantially outperformed sector ETF

On first look, it appears that Bank of America must have had great managers with great judgement about where to spend money. How else could they have performed so much better than both a financial sector ETF and the S&P 500 for almost two decades?

However, as you read through the next few case studies, you might start to wonder (as I did) whether Bank of America’s performance might not be as good as it first appears. The most obvious potential source of bias is the fact that the time period of our study includes the financial crisis. During the financial crisis, the federal government gave billions of dollars of assistance to Bank of America and certain other large banks. Not every company included in the XLF financial sector ETF received the same level of assistance. The discrepancy is even larger if we compare against the companies in SPY. To investigate this possibility, let’s re-run our analysis but this time just over the period after the financial crisis.

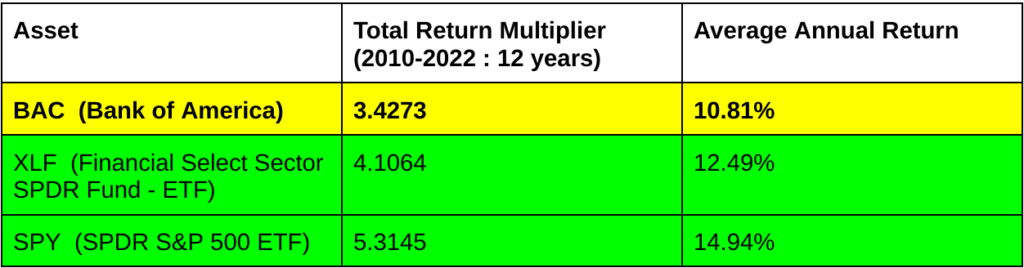

Case Study 1A: Bank of America (Post-Bailout)

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed sector ETF

These results are quite different from what we had before. This time, Bank of America’s stock noticeably underperformed both the financial sector specifically and the larger stock market in general. This isn’t enough data to definitively say that Bank of America’s overperformance measured in our first case study was entirely due to special treatment by the government. However, that explanation does seem entirely possible given the systematic underperformance after the special treatment was over.

Case Study 2: FedEx

*Note: UPS is a close competitor of FedEx but is omitted from comparison because it had not yet IPO’d at the time this comparison starts.

VERDICT: Underperformed

Moderate to substantial underperformance of most competitors

Similar performance to XLI (not the best comparison ETF, but the closest available that existed for the full length of the study)

Similar performance to S&P 500

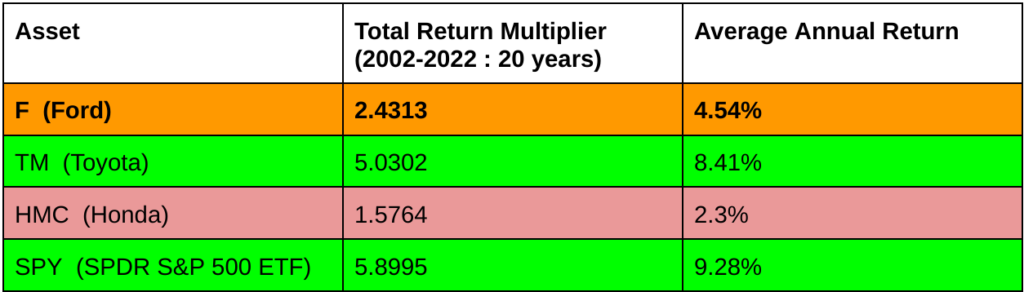

Case Study 3: Ford Motor Company

VERDICT: Underperformed

Substantial underperformance of S&P 500

Mixed performance relative to competitors

It’s hard to compare Ford to direct competitors since many competitors either have not been publicly traded since 2002, are foreign companies (and hence excluded from this study in an attempt to provide a more apples-to-apples comparison), have undergone substantial mergers or restructuring events, and/or also sponsor major league sports venues. However, despite those issues, it’s still clear that Ford has not performed well over the past two decades.

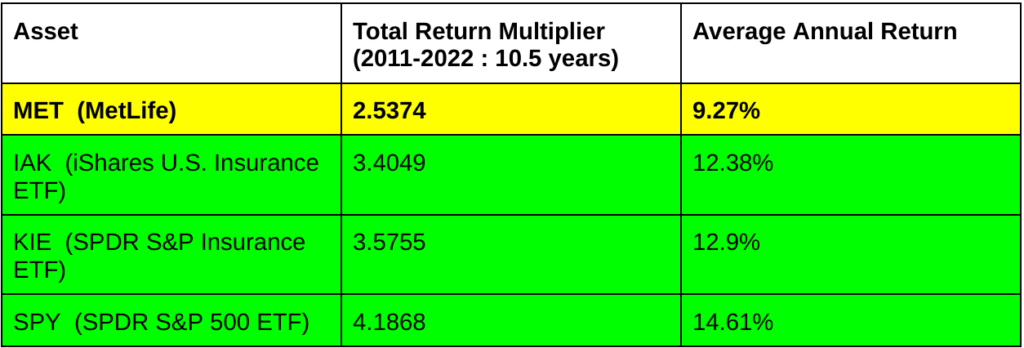

Case Study 4: MetLife

VERDICT: Underperformed

Substantial underperformance of S&P 500

Moderate underperformance of insurance sector ETFs

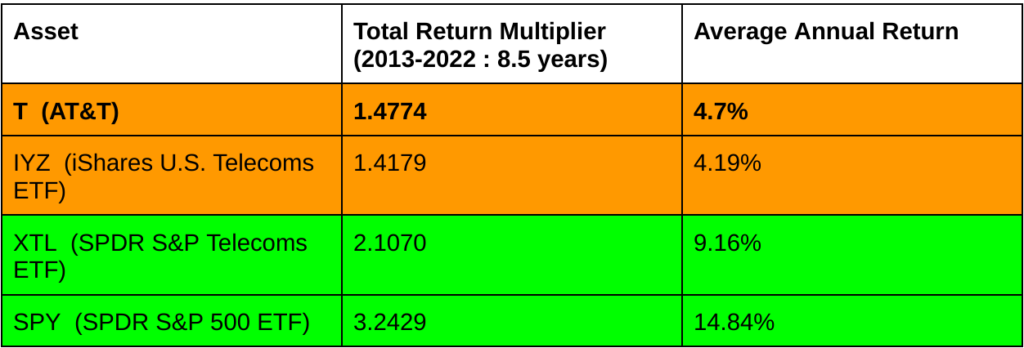

Case Study 5: AT&T

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed sector ETFs on average

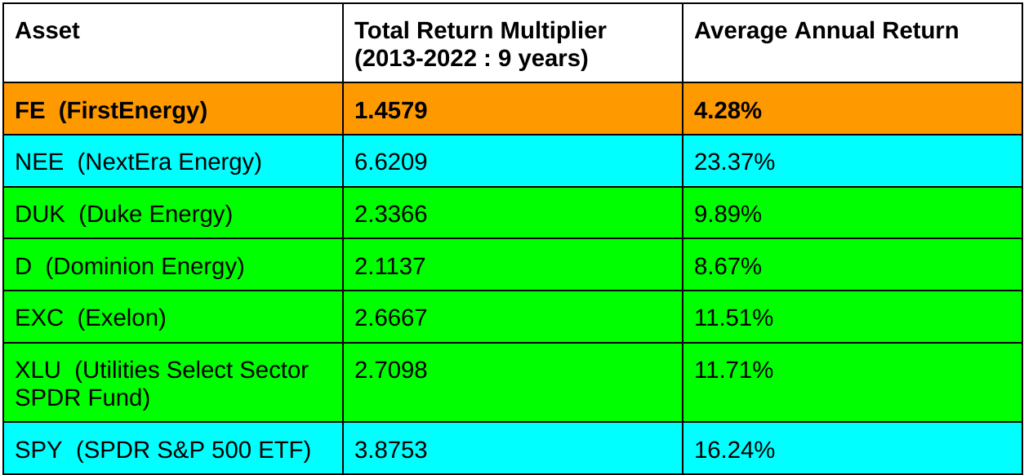

Case Study 6: FirstEnergy Corp

VERDICT: Underperformed

Substantial underperformance of S&P 500

Substantial underperformance of competitors

Substantial underperformance of sector ETF

It’s worth noting also that as of 2022, FirstEnergy is involved in serious legal issues after it came out that the company had spent $64 million dollars bribing state government officials. There seems to be a pattern of energy companies that sponsor major league stadiums getting involved in scandals. For a brief period, the Astros baseball team played their home games in “Enron Field”. Chesapeake Energy also put their name on an Oklahoma NBA arena before it later become involved in a price-fixing scandal. In fact, if you take away just one thing from this article, it should be to never buy stock in energy companies with their names on stadiums. And if you run a hedge fund, you might consider them as short positions against an energy-heavy portfolio. (To access my complete model & analysis for such a strategy, subscribe to Axiom Alpha Market Intelligence and I’ll include it with the next issue).

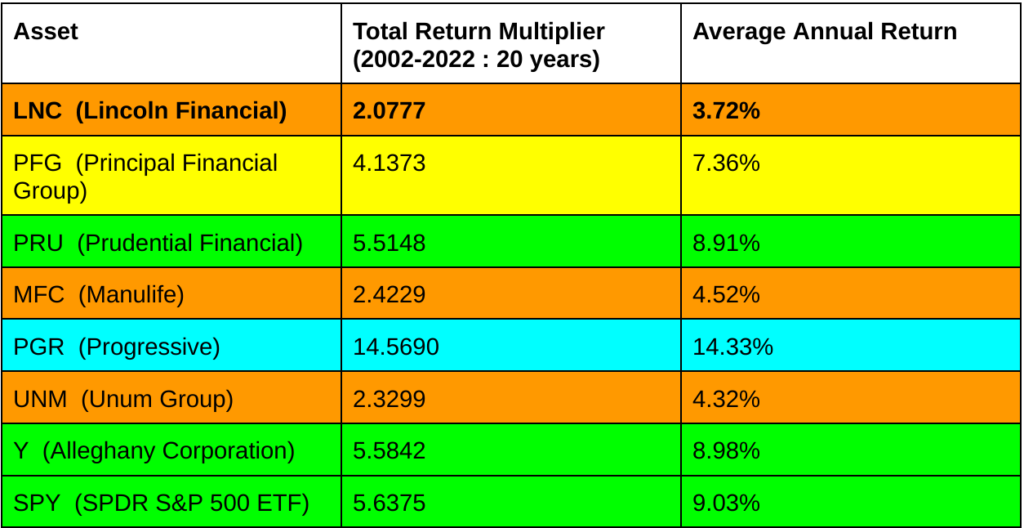

Case Study 7: Lincoln Financial

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed every competitor analyzed (many substantially)

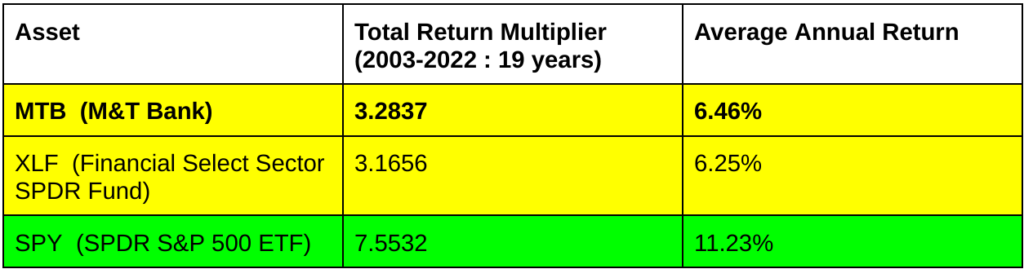

Case Study 8: M&T Bank

VERDICT: Underperformed

Substantial underperformance of S&P 500

Similar performance to sector ETF (even though M&T Bank got a government bailout during the 2008 crisis and not every company in the ETF did)

Unlike the situation we saw earlier with Bank of America, M&T Bank underperformed the S&P 500 even over a time window that includes the financial crisis. However, they still appear to perform similarly to the financial sector as a whole. Given that M&T also received more government assistance than your average finance company though, we have another opportunity to test our hypothesis. If stadium names are in fact generally bad purchases, then when we re-run our analysis for the period after the financial crisis, we should expect to see MTB flip to substantial underperformance relative to XLF. Let’s test.

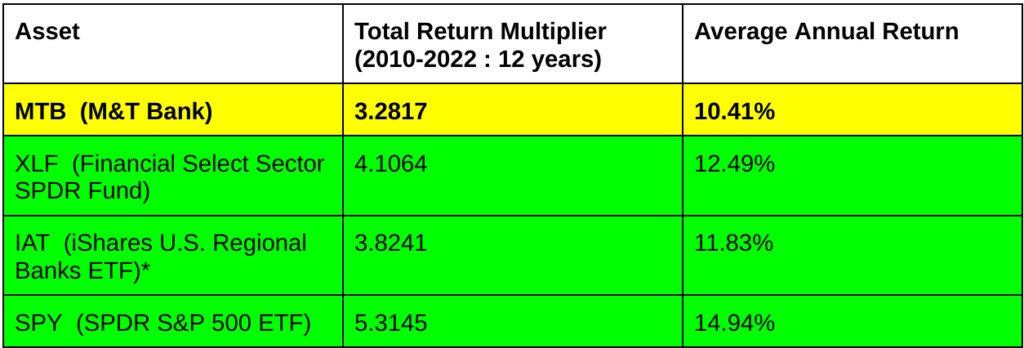

Case Study 8A: M&T Bank (Post-Bailout)

Exactly as expected, MTB consistently underperformed both the finance industry specifically and the market generally after the financial crisis. I even included another bank-specific ETF here (which wasn’t included in the previous comparison since it didn’t exist in 2003). MTB also underperformed that bank-specific ETF.

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed sector ETFs

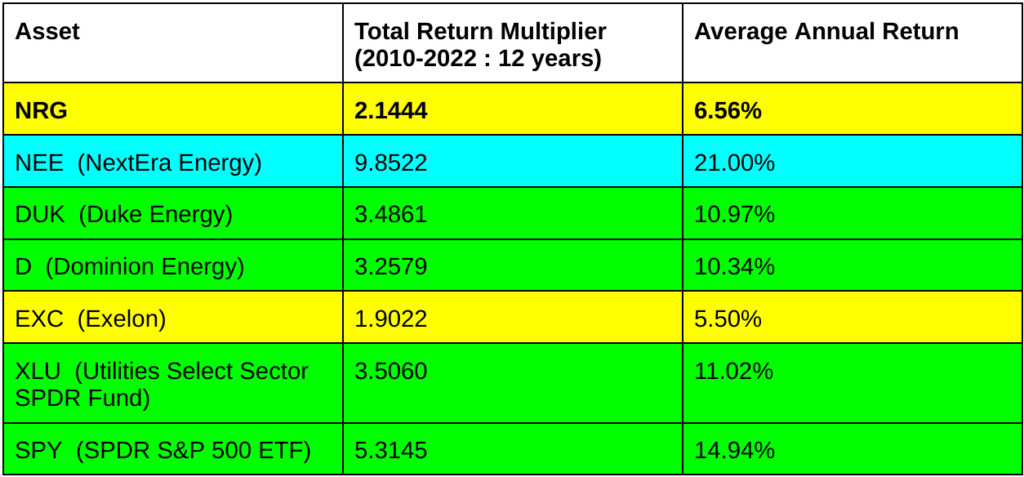

Case Study 9: NRG

NRG is an energy company with its name on a stadium, so you already know what to expect from our previous discussion.

VERDICT: Underperformed

Substantial underperformance of S&P 500

Substantial underperformance of most competitors

Substantial underperformance of sector ETF

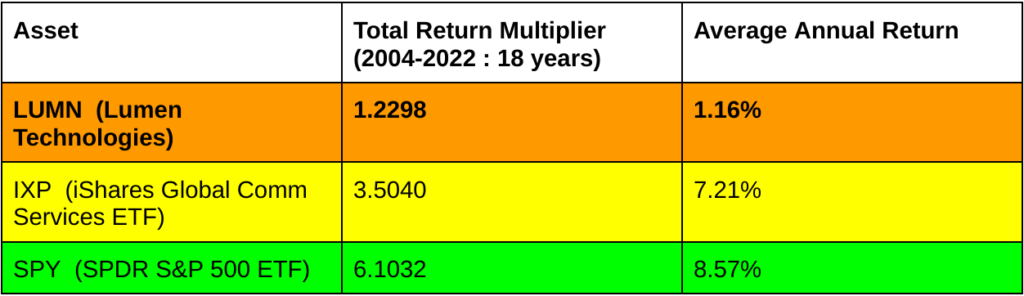

Case Study 10: Lumen Technologies

To accurately analyze Lumen Technologies, we have to account for several events. In 2002, a new stadium opened in Seattle with the name “Seahawks Stadium”. In 2004, Qwest Communications International bought the naming rights to the stadium which was renamed “Qwest Field”. In 2011, the stadium was rebranded to “CenturyLink Field” after Qwest was acquired by CenturyLink. In 2017, the company extended their naming agreement until 2033. Then in 2020, the stadium was rebranded to “Lumen Field” after CenturyLink restructured into three entities: Lumen Technologies, CenturyLink, and Quantum Fiber.

Ordinarily, I wouldn’t include a company that went through so many restructuring events because even if you can adjust stock prices accurately, you don’t know whether the merger event changed the management style. For example, Proctor & Gamble have been excluded because after they acquired Gillette, the new top level management did not clearly signal agreement with the original Gillette management’s decision to invest in the naming of Gillette stadium. In contrast, after each of the events Lumen and its predecessors was involved in, the post-event management team decided to reinvest additional dollars into the stadium sponsorship deal. For that reason, it seems fair to include them in our analysis. Here’s how they performed:

VERDICT: Underperformed

Substantial underperformance of S&P 500

Substantial underperformance of sector ETF

It’s also worth noting that in recent years Lumen has pivoted substantially into cloud and software more than its roots in telecom. If we were to compare them to their current competitors (which include companies like Microsoft and Oracle) rather than their historical competitors, their relative underperformance would have been even worse than it is in the chart above.

Total Return Statistics

Of the 10 companies we just analyzed, 9 underperformed a basic portfolio consisting of a 50/50 split allocation between their industry peers (represented as a sector ETF where one existed and by an equal weight index of direct competitors where one did not) and the S&P 500. Six of the companies underperformed the S&P 500 by more than 50%. Furthermore, if we adjust our analysis to only look at banks after they received financial assistance from the government, all 10 companies underperformed. That’s compelling, but not quite statistically significant. However, if we loosen our sampling criteria a bit, then we can look across a broader set of 98 publicly traded companies that bought naming rights for NFL, NBA, MLB, or NHL stadiums between 1973 and 2019. We stop in 2019 to avoid needing to analyze weird effects of massive government subsidies & fiscal stimulus during 2020 and 2021.

From this larger set of companies, two stand out for substantial overperformance: Qualcomm (QCOM) and Target (TGT). Given our earlier results being very subpar, it’s worth looking at what’s going on with these examples.

Qualcomm

Several things pop out of the details of Qualcomm’s agreement to purchase the naming rights to the San Diego Chargers’ stadium in 1997. The first is that Qualcomm paid a truly tiny sum ($18 million) for 20 years of naming rights. The second is that they paid this entire $18 million sum upfront rather than spreading it out over the duration of the agreement. The context for how this deal happened is that the city of San Diego was desperate for funding to finish an expansion of the stadium. Qualcomm stepped into the gap and got a 5-10x cheaper price than other companies paid around that time for similar name deals. In other words, Qualcomm didn’t go looking for a stadium naming deal. Instead, they acted opportunistically to seize an opportunity to make a deal with a desperate local government at a price that was only 10-20% of what other companies were paying for the same types of deals.

Target

Target has been very reluctant to release any financial information regarding their 1990 deal to name a Minneapolis NBA arena the “Target Center”. However, piecing together what we do know, it seems likely that the 25 year agreement carried a price tag of about $1-1.5 million per year. That’s about 25-50% of what companies were paying a decade later, adjusted for inflation, and just 10-20% of what companies were paying in 2021. Additionally, the Target agreement was deeper than just a name. The agreement also included provisions for certain NBA players to visit Target stores. Some basic modeling of retail customer behavior and attendance to NBA autograph events suggests that this provision alone might have been worth a substantial portion of the agreement. Target also hasn’t disclosed details about specific merchandise partnerships, but it’s quite possible that Target may also get a direct benefit in terms of discounts and/or exclusivity for certain branded merchandise. Finally, consider the fact that the Target Center is a mere 0.4 mile walk from Target HQ. How much cost could Target reduce in corporate employee churn & payroll by offering perks for NBA game tickets & events with players? All of that is in addition to the “standard” naming deal benefits including TV and in-person branding.

A RobustPattern

Based on our analysis of Qualcomm and Target (and verified against a few other companies that outperformed but to a much lesser degree), we can define a clear set of properties that constitute a “good deal” when it comes to naming rights. If we then analyze our set of 98 companies and eliminate all companies that meet those “good deal” criteria, we find that the remainder systematically underperform in a significant way. That’s a pretty interesting result for anyone interested in long/short hedged strategies. It also means that if I personally held any Crypto.com stock in the private market, I’d dump it because its stadium deal doesn’t meet the “high quality” deal criteria. Complete data & results for this extended study, along with a model investment strategy based on it, will be included in my next issue of the Axiom Alpha Market Intelligence newsletter (a paid subscription for deep market data & analysis). For the more casual reader, you can subscribe to the Axiom Alpha Letter (of which this article is an example issue) for free!

Disclaimer: Nothing in this article should be considered investment or financial advice. This content is for information & educational purposes only. Neither Homology Group Inc. nor any of its representatives will be liable to you for any actions you take or don’t take based upon the information in this article or other Axiom Alpha content. Axiom Alpha is a brand name of Homology Group Inc.

How to increase revenue 46% by changing one character

“3 out of 4 of our target customers were in North America and when we made the change we saw a 5x increase in conversion — all by literally just changing the currency symbol.”

– Paul Farnell (CEO of Litmus, speaking on keys to their early successes)

Cosmetic price localization is a very low-hanging fruit to increase both revenue & profit for many eCommerce, SaaS, mobile app, and remote service companies. In its simplest form, it consists of just changing the currency symbol so that each potential customer sees your product’s price stated in their native currency. However, as Paul discovered when he started pricing North American customers in USD ($) rather than Euros (€), even this very simple change can be incredibly profitable.

Paul’s 500% increase in conversions is definitely above average, but almost any company with even a few percent of international customers can use this tactic to increase their monthly revenue growth rate by several percent — a difference which can compound substantially even during a single year. In this article, I’m going to explain:

How much extra revenue online startups can expect to add each year by using price localization

The simplest tools to implement cosmetic price localization on your website

How much can price localization increase revenue growth for a startup?

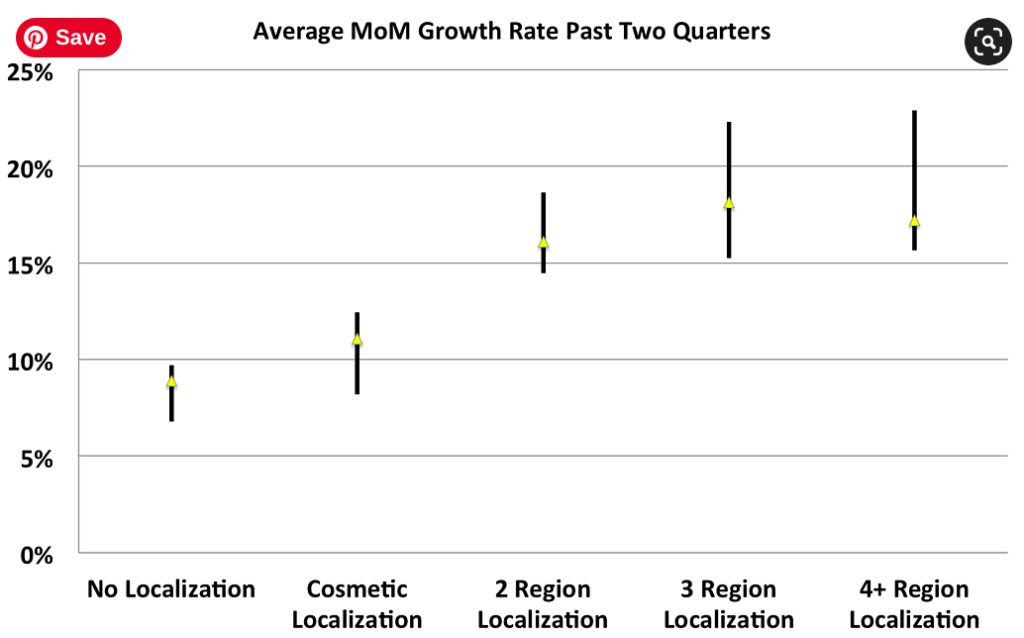

A study by Price Intelligently looked at 457 software startups which had at least 10% of their sales outside the U.S. The study found a 3.2% increase in median month-on-month revenue growth rate for companies doing cosmetic price localization when compared with companies doing no price localization. That means over the period of one year, the extra growth of the startups using cosmetic price localization will compound to put them ahead of their non-localizing counterparts by almost 46% (1.032^12 = 1.46). Keep in mind, these startups were only using cosmetic price localization — not any other type of price localization.

Startups that also used true price localization (i.e. setting prices in different countries based on the different ability & willingness to pay in different countries) did even better. In this chart from the study, you can see how progressively more localization tends to provide progressively faster company growth rates:

Even if only 2% of your sales are to customers outside the U.S. (rather than the 10%+ of the startups in the study), the statistics above suggest a median increase in monthly revenue growth of about 0.64% by using cosmetic price localization. Over one year, that would compound to put you ahead by almost 8%. You’d be hard-pressed to find another task that you can implement in less than half a day which can increase your startup’s annual growth by 8%. In reality there are many factors which will cause this number to vary for any particular startup (e.g. geographic customer distribution, level of existing company traction & product-market fit, pre-existing growth rate, etc). However, it does seem evident that whatever the number is, it is an impressive one for many startups.

There are two reasons why cosmetic price localization is so effective, and both are fundamental features of human nature. The first reason is that humans are hardwired to infer trustworthiness from familiarity. This means, for example, that a European immediately views a website with € prices to be much more relevant and trustworthy than one with £ prices. A Brit would assume the opposite.

The second reason why cosmetic price localization is so effective is that humans hate uncertainty, and foreign currencies are uncertain. If an American sees a price written with £ prices, they’ll be uncertain about exactly how much money that actually is until they are charged a $ amount. If the purchase is a subscription rather than a one-time purchase, the uncertainty is even higher because fluctuating exchange rates will mean a different $ amount will be charged every single month.

Both reasons mean that almost every potential customer in a country with a different currency than your pricing page will bounce rather than convert. However, the moment you communicate in terms they are familiar with, many will recognize your product as significantly more relevant, trustworthy, and predictable.

I’ll explain how to implement cosmetic price localization first for developers and then for non-developers. Skip to whichever section fits you and read that one. If you still feel like you’d rather hand off the task to an expert, shoot me an email. My team does this kind of thing all the time, and we’d be happy to help. I’m not paid to talk about any of the companies or tools discussed below.

Note: For complete cosmetic localization, you’d also want to translate the writing of your website into the local language of the region where a particular user is. There are numerous ways to implement that which I won’t discuss here, but that is another thing my team is happy to help with if you’re interested.

For Developers

Implementation requires two steps: (1) figure out which country a website visitor is in (and therefore what currency they use), and then (2) display & process any payments in that currency.

Step 1 can be accomplished by first identifying the IP address of the client device and then running an IP address lookup. One of the best IP address lookup services is IP Info. They are used by both startups and massive enterprises, have a free plan that allows for up to 50k queries per month, and have paid plans that enable VPN detection which you’ll need to prevent location fraud when you eventually graduate from purely cosmetic price localization to true market price localization.

Step 2 is typically handled by your payment processor. If you use Stripe, you can can create two different prices (each with a different currency) for the same product. For example, if you have a product named prod_A, you can give it price_1 = €19.00 / month and price_2 = US$20.00 / month. For more details, check out this documentation and this documentation.

You don’t have to use Stripe by any means though. Other options like Paypal advanced checkout offer similar capabilities.

For Non-Developers

How you implement price localization will depend on what web tools you used to create your website. I’ll go through several of the most common situations:

WordPress & Woocommerce

Woocommerce is a popular e-commerce plugin for WordPress. If your business website is WordPress, there is a good chance you handle payments with Woocomerce. One way to add price localization to Woocommerce is through the Price Based On Country for WooCommerce plugin. Just install the plugin and set the price for each country you care about.

Shopify

Shopify Markets is the easiest way to implement cosmetic price localization for Shopify stores. Shopify Markets is a centralized international management tool that lets you set prices in local currencies for any country or region.

An alternative to Shopify Markets is to set up multiple Shopify stores, each tailored to a different international market. This is probably the best option since you can also translate the writing into the appropriate language for each market.

A third option is available to entrepreneurs on the Shopify Plus plan. On this plan, your store automatically sets your customer’s country or region and currency based on their IP address.

Squarespace

Squarespace offers several different payment providers. Some providers such as Afterpay and Square offer very limited international availability. The most widely available payments option is Stripe. Stripe can be customized to provide cosmetic price localization in a huge number of countries, but it does require a bit of programming. Paypal is also widely available internationally but likewise requires a bit of programming to effectively set up price localization. If you don’t have the necessary programming skills, feel free to send me an email using the form below. My team would be happy to help.

“Including the sewer line replacement, pumping the basement, cleaning the basement, replacing the section of wet wood between first story floor and basement ceiling, and replacing the wooden stairs that descended from first story to basement, Lisa’s final cost came out to be just over $33,000.”

Lisa received a 17-second mp4 file from her tenant on Monday night. The video opened with a view of brown water slowly flowing out of the junction between basement ceiling and basement wall of Lisa’s rental house. The view then pans down the wall to reveal 2 inches of brown fluid covering the basement floor.

When the emergency plumber was finally able to diagnose the problem, the culprit turned out to be a solidified mass of “flushable” wet wipes, cat litter, and number 2. The mass had grown inside a sewer pipe joint located under the first story floor of the house, just adjacent to the staircase which descended to the basement. The mass was slowly built over the course of 10 months from two bad habits of Lisa’s tenant.

The first bad habit was using flushable wipes exclusively in place of toilet paper. The sad reality is that most wet wipes advertised as “flushable” shouldn’t really be flushed. The reason toilet paper can be flushed is that it easily disintegrates in water. If you place a “flushable” wipe in cold water and there are still large pieces in 5-10 minutes, then the wipe is not actually flushable. That was the case with Lisa’s tenant’s wipes. These wipes, flushed many at a time, accumulated in the joints and bends of plumbing pipe throughout the house, but particularly in the 90-degree angle joint under the first story floor.

The second bad habit was using a cat toilet trainer. Lisa’s tenant had two cats, and she used a type of toilet training device to train her cats to poop in the toilet rather than a litter box. Unfortunately, this training device used cat litter during the initial phases of training (something like the image below).

Some of this cat litter ended up in the toilet. Over time, this cat litter got caught in the flushable wipes that were accumulating in the sewer pipe joints. Once caught, the cat litter rapidly formed a sort of cement.

The combination of wipes and litter cemented into masses that partially choked multiple flow points in the house’s plumbing system. These choke points in turn created high-pressure zones in the middle-aged cast iron plumbing pipes. Eventually, the flushable-wipe-cat-litter-cement clog in the first story floor joint restricted flow so much that the pipe developed cracks. These cracks likely existed unnoticed for several weeks as they slowly leaked small quantities of sewer water into the wood beams of the basement ceiling and the wood stairs that descended from first floor to basement. Finally, the cracks widened enough to allow noticeable fluid flow to start draining out of the pipes, through the basement ceiling, and onto the basement floor. The damage to the house was substantial.

Multiple stretches of sewer line had to be replaced. A large section of first story flooring and basement ceiling had wood which had been soaked for weeks and had deteriorated to the point of needing replacement. The wooden staircase to the basement also needed to be replaced. The basement had to be pumped, cleaned, and sterilized. Some areas of basement ceiling and walls needed mold treatment. After everything, Lisa’s repair costs summed to just over $33,000.

Like many homeowner’s insurance policies, Lisa’s policy didn’t cover this type of sewer line damage. Like many renter’s insurance policies, Lisa’s tenant’s renter’s insurance policy didn’t cover this type of sewer line damage. To make matters worse still, Lisa didn’t have a particularly strong legal case. The rental property was in a very tenant-friendly jurisdiction where flushing wipes advertised as “flushable” was not considered negligent. In the end, Lisa paid the entire repair amount out of pocket.

Is there anything Lisa could have done to prevent this? Yes!

Lisa’s situation would have been very different if she had included a “do not flush” clause in the lease contract with her tenant. A “do not flush” clause describes what can and cannot be flushed, and clearly puts liability on the tenant for any damages caused by lack of compliance with the “do not flush” clause. Such a clause can often bypass considerations of whether or not a tenant was “negligent” if it can be shown that the tenant flushed something on the do-not-flush list.

If you ever own or operate a rental property, here is a “do not flush” clause that you can use in your lease contracts to avoid ending up like Lisa.

“Do not flush” clause sample

Toilet Flush Rules. Tenant agrees to only put human bodily waste and toilet paper down the toilet. Things Tenant agrees to NEVER flush down the toilet include, but are not limited to:

Wet wipes, baby wipes, disinfectant wipes, cleaning wipes, or other disposable wipes (including wipes advertised as “flushable”)

Paper towels

Toilet bowl scrub pads

Tissues

Cardboard toilet paper rolls

Swiffer pads

Tampons, pads, or other feminine products

Cotton balls

Q-tips

Underwear of any sort

Diapers

Hair (e.g. from a brush or comb)

Dental floss

Bandaids

Cooking oil or grease

Food

Napkins

Cat poop

Cat litter

Contact lenses

Fish (dead or alive)

Condoms or condom wrappers

Pee test sticks

Toys

Plastic bags or packaging

Drugs (prescription or otherwise), medications, vitamins, or dietary supplements

Tenant shall be liable for any and all damages caused in whole or in part by, or catalyzed by, any use of any toilet which is not in accordance with the afore-described usage restrictions.

Disclaimer

Nothing in this article should be considered legal advice, opinion, recommendation, or guarantee of any sort.

To receive more articles like this straight to your inbox at least once a week, subscribe to the Axiom Alpha email newsletter! We talk about the best finance strategies & tactics for entrepreneurs and investors, explained with stories and examples.

“What you thought was a 5-minute survey actually cost your client $100,000. Here’s how to avoid that.”

POV: You run a B2E (business-to-enterprise) consulting firm. Your current client is a 10,000-employee company that’s asked you to come up with a strategy to boost employee morale and also reduce last-minute absences from employees.

To develop such a strategy, you first need to understand why morale is low and why last-minute absences are so prevalent. I.e. you need to develop some empathy with your client and their employees so that you can propose a solution that will actually work for them. But how do you develop empathy with 10,000 employees?

You could start by sending a 5-minute survey to every employee. Given the psychological distraction of task-switching, that means a 5-minute survey will probably cost at least 10 minutes of lost productivity. 10 minutes of lost productivity multiplied by 10,000 employees is 100,000 minutes of productivity lost for the company. 1667 hours. Over 208 days of full-time effort lost. There are 250 workdays in a year, so that’s over 83% of an entire employee-work-year of productivity loss. If the typical employee makes $100,000/year, then after employer taxes, healthcare costs, etc, a typical employee likely costs at least $120,000/year. 83% of that is $99,600. In other words, your 5-minute survey has cost your client about $100,000. To add insult to injury, a 5-minute survey may help you identify possible problems that cause low employee morale, but it likely doesn’t give you quite enough to really understand the problem. You’ll have to send more surveys or conduct employee interviews later.

The problem with helping large enterprise clients solve large internal problems is that even diagnosing the problem can cost the client a lot of money. However, it doesn’t have to. I’m going to teach you a dirt-simple statistical trick that will allow you to answer lots of questions with minimal time & cost to your client. Not only will your consulting services be less intrusive, you’ll also be able to ask way more questions.

The rule of 5

The trick is called the rule of 5.

Suppose you hypothesize that employee morale may be low because many employees are stressed-out parents with young kids. Maybe adding daycare could boost morale and also decrease last minute call-outs caused by childcare issues?

You’d like to find out whether a lot employees actually do have kids under the age of 6 who are in need of better childcare. However, the employee database doesn’t track whether any particular employee is a parent. Here’s what you can do.

Start pulling random employees from the database. For each employee, shoot them a Slack / Microsoft Teams message asking if they are a parent. If so, ask them the age of their youngest kid. Repeat until you have 5 employees who respond that they are a parent and provide the answer of youngest child’s age.

Suppose the answers you get are 2 years, 2 years, 5 years, 1 year, and 6 years old.

Look at the lowest (1 year old) and highest (6 years old) of the 5 answers. There is a 93% chance that the median age of the youngest child of employee-parents is in that range. In other words, from just a few unintrusive Slack messages, you now know with high confidence that at least half of parents working for the company have a child aged 1-6 years old. Impressive! Company childcare might really help! It might now be worthwhile to send out some surveys.

How to use the rule of 5

The rule of 5 is an extremely general technique to estimate the average value (median) of any variable. Here is the distilled procedure:

Randomly sample 5 people or things you want to know about (e.g. employees who are also parents)

Record the value of a variable you care about for each sample (e.g. the age of youngest child)

Find the minimum and maximum value of the 5 results

If you follow those three steps, there is a greater than 93% chance that the minimum-to-maximum range you found in step 3 contains the median value of the variable you care about.

Why does the rule of 5 work?

The median is a special number: half of results are above it and half below it. That means each sample you collect is a coin flip: 50% chance it is above the median and 50% chance it is below the median. The chance of not sampling anything above the median 5 times in a row is then the same chance as flipping a coin 5 times and getting heads every time: (0.5)^5 = 0.03125 (.e. 3.125%).

The chance of sampling 5 times and not getting anything below the median is the same: 0.03125

That means that the chance of a random sample of 5 containing at least one value above the median and one value below the median is:

0.9375 = 1 – 0.03125 – 0.03125

I.e. 93.75%

This works whether you are sampling 5 employees from 10,000 or 5 cans in a warehouse from 1,000,000.

Some additional example use cases

The rule of 5 is useful to estimate the average value of all sorts of things in business. Here are some additional examples:

The expiration date of cans on the shelves of a grocery store

Order size of purchases through an e-commerce website

Age of a bar’s customers (e.g. if the bar wants to tailor its marketing to the demographics of its existing customer base)

The typical price of various competitors’ products at a retail store

How the average employee at a company would rate the competence of their boss on a scale from 1-10 (variations of this can be extremely useful ways to quickly gauge employee sentiment about various aspects of their work experience, even in huge organizations with tens of thousands or hundreds of thousands of employees)

“Kara sold her software company for $1.33 billion and paid ZERO capital gains taxes. I don’t mean the tax bill was deferred to a later year. I mean the tax bill was erased from existence. Permanently.”

Back in the good old days (1862-1986), the Homestead Act allowed U.S. citizens to claim up to 160 acres of government-surveyed land for free. Unfortunately that opportunity doesn’t exist anymore. However, something even better does: Opportunity Zones (OZs). That’s not hyerpbole either. Opportunity zone tax breaks ARE actually more valuable than getting 160 acres of undeveloped land, and I’m going to show you how.

People who have heard of opportunity zones before often have two misconceptions.

The first misconception is that opportunity zone tax loopholes are only useful to people who are already wealthy. That’s wrong. It will help if you have at least a few thousand dollars, but you certainly don’t need millions. In fact, opportunity zones are probably the most useful to ambitious people who want to create companies but haven’t started yet.

The second misconception is that the opportunity zone tax loophole is only useful for real estate investing. That’s also completely wrong. In 2019, the IRS published a 544 page document with painfully detailed commentary on all sorts of various things you can do with opportunity zones. That information made it very clear that many businesses and business owners (whether investors or founders) can benefit from opportunity zone tax breaks if they are willing to follow the relevant rules.

In fact, the very generality of opportunity zones sometimes confuses people. How can one tax rule be equally useful to Amazon, a Silicon Valley startup, a local ice cream shop, a crypto trader, a hotel investor, a one-woman services business, and an aspiring entrepreneur who hasn’t even created a company yet?

The answer is that there are actually a LOT of tax rules related to opportunity zones, most of which are unfamiliar even to professional investors. These rules are Legos that can be assembled to provide all sorts of different benefits to all sorts of different people and businesses. I’m going to teach you to wield these rules as a secret weapon to obliterate tax bills, get subsidized assets from the government, and destroy your competitors who aren’t using opportunity zone strategies.

This letter is different than my typical letters. It’s 5 times longer and 50 times more valuable. It’s a precise guide to opportunity zone strategies that can save you literal bricks of cash that would otherwise disappear to taxes. Some of the strategies are a bit complicated, but the cost reduction they provide is bigger than the differences that frequently dictate which of two competitor businesses survive. As Robert Frost once said:

“Two roads diverged in a yellow wood. At the end of one were the basic bitches, and at the end of the other was a qualified low-income census tract designated as an opportunity zone, and I took that less-traveled road.”

Maybe those weren’t his exact words, but it was something like that.

By the end of this letter, you will know:

How to pay zero taxes on a $1 billion cash exit

How you and your business can avoid paying taxes on 25 years worth of *realized* capital gains

How to eliminate depreciation recapture taxes

How a startup can raise more money, faster, at a higher valuation

How to find investors desperate to invest in your small business, even if you’re not growing like a VC-fueled Silicon Valley startup

Let’s dig in.

How opportunity zones work

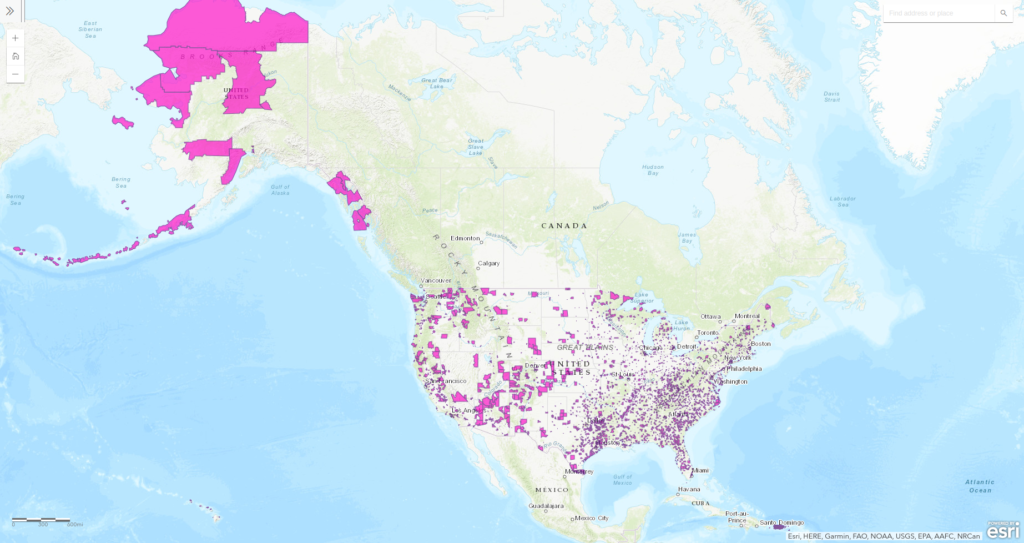

An opportunity zone is just a low-income census tract that has been designated as an opportunity zone by a state government. Here is a map showing all opportunity zones in the country:

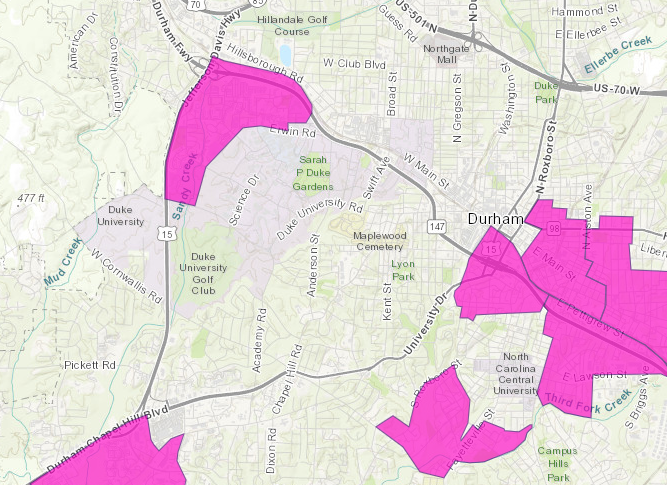

The various tax rules related to opportunity zones are all government incentives for investors and companies to come in and create jobs, infrastructure, and wealth in these areas. Some zones are vast swaths of barren land in the middle of nowhere. Others are run-down areas in the middle of cities. And still others are right next to universities where college student populations depress income levels even if the areas are developed. For instance, here is an opportunity zone located right next to Duke University in North Carolina:

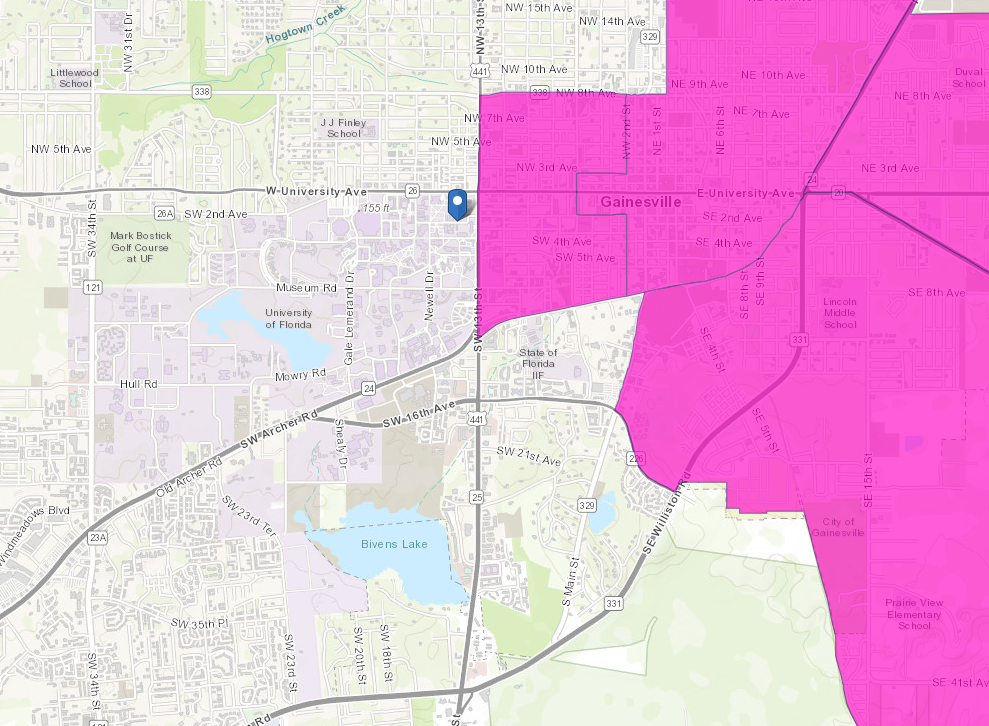

And here is a big block of opportunity zones right next the University of Florida:

The essence of the opportunity zone tax loophole is that if you reinvest capital gains into businesses or property located in an opportunity zone, then you can defer some taxes and eliminate other taxes altogether. However, there are certain strategies that will allow you to benefit from this loophole even if you don’t have any meaningful capital gains right now. I’ll explain how that works later in this letter.

The basic setup is that any person or company which can meet four sequential requirements will benefit from privileged tax treatment:

Sell property, stock, crypto, NFTs, or anything else that results in a capital gain before December 31, 2026.

Reinvest the amount of the capital gain (e.g. if you bought stock for $500 and sold it for $600, then reinvest the $100 gain) into a type of investment fund called a “qualified opportunity fund” (QOF) within 180 days of when the gain was realized. A QOF is a special-purpose business entity that must invest into businesses or property within one or more opportunity zones.

Hold your QOF investment(s) for at least 10 years.

Sell your QOF investment(s) before December 31, 2047.

If all four conditions are met, then you receive two tax advantages at different times.

The first tax advantage is a deferral of tax on the initial capital gains that you reinvested into the QOF. The deferral pushes that tax bill back until you file your return for 2026 (about 5 years from the time I’m writing this). In the meantime, those capital gains can be put to work in investments that go up in value. That brings us to the second tax advantage.

The second tax advantage is a complete elimination of capital gains tax on any increase in value of those QOF investments. Technically, this is accomplished by a law which resets the “tax basis” of the investment to “market value” when you sell. That should perk up the ears of anyone familiar with depreciation recapture because it means that you don’t have to ever repay depreciation deductions! More on that later though.

Example 1: simple QOF investment math

Bob has $2 million invested in the stock market. $1 million of that is unrealized capital gains. It doesn’t matter whether those are short or long term capital gains–either can be reinvested into a QOF.

Bob sells his entire stock portfolio in May 2022. If the gains are long-term capital gains, then Bob would owe $200k = 20% of $1M in capital gains tax for 2022 (if the gains were short term, that bill would be almost twice as much). However, Bob chooses to invest $1M in a qualified opportunity fund in August 2022. Since that is less than 180 days after he recognized his $1M gain, he has eliminated his entire $200k capital gains tax bill for 2022.

Over the next 5 years, Bob’s QOF investment goes up in value from $1M to $2M. He has to file 2026 taxes now, which means he owes his $200k tax bill. Note that it is still $200k, not $400k, despite the QOF investment doubling in value. For simplicity, I’ll assume Bob pays the $200k with money he has in a bank account outside the QOF. (There are ways to take tax-free distributions from a QOF to pay that $200k tax bill, but those would complicate our discussion more than is necessary.)

Bob continues to hold his QOF investments all the way until 2047 when he sells them for $6 million. That means over 25 years, his $1 million has turned into $6 million (a $5 million gain). If the long-term capital gains tax is still 20% in 2047, then Bob would normally owe $1 million = 20% of $5 million in taxes. However, because this gain was held for more than 10 years through a QOF, Bob owes ZERO dollars in taxes.

There is no deferral happening here. Bob never has to pay that million dollar tax bill — the tax bill is simply erased from existence as if Thanos had snapped his gauntleted fingers.

Example 2: the tax-free billion-dollar exit

Kara is an aspiring entrepreneur who wants to create a new word game app. She wants to put $1000 of her own money into the company to start it.

Kara could just transfer $1000 from her bank account to the business’s bank account. However, if her company becomes very successful and is eventually acquired, she would have to pay a huge amount in capital gains tax. So instead, Kara checks her Robinhood account. She’s been holding two shares of Tesla stock since right after the stock split in 2020 which means she’s sitting on $1120 of unrealized capital gains. She forms an LLC to serve as her QOF and deposits the $1120 into her new LLC bank account. Her LLC then forms a wholly-owned C corporation subsidiary which will be the startup that actually builds the new app. Importantly, she starts working at a coworking center located in an opportunity zone so that her C corporation immediately starts off as a QOZB (qualified opportunity zone business).

Kara’s company begins to grow. Over the next two years, she takes on one outside investor through another QOF which takes 20% of her corporation. She scales up to a team of 8 people. Five people work from her original coworking space (although now in a larger, dedicated office) and 3 people work remotely from another coworking space in a different opportunity zone. The app’s computing & data storage needs are supported entirely by cloud infrastructure rather than company-operated servers. By this time, the app is generating over $50 million / year in revenue.

Over the next 10 years, Kara’s company grows by acquiring other game & puzzle apps run by lean teams and relocating their teams to office spaces in opportunity zones. By the end of this period, the company is bringing in over $500 million in annual revenue. At this point, she decides to sell her company. She asks Goldman Sachs to look for buyers and eventually gets an all-cash offer from the New York Times for $1.33 billion. She takes the deal.

At the time of sale, 20% of the corporation has been sold to an outside investor and another 5% has been given to various employees over the years. That leaves Kara (through her QOF) with a 75% stake in the corporation.

75% of $1.33 billion is $1 billion: Kara has a $1 billion exit. Ordinarily, Kara would owe long-term capital gains taxes on that entire amount of $1 billion minus her $1120 of initial capital. At today’s long-term capital gains rate of 20%, that’s a two hundred million dollar tax bill! If Biden succeeds in raising the long-term capital gains rate to 39%, that would be a $390 million tax bill! However, since Kara’s initial investment was through a QOF, she owes ZERO TAXES.

This strategy is applicable to the MAJORITY OF STARTUPS. Most modern tech startups are asset-light internet companies or internet service agencies which can easily comply with opportunity zone business requirements. Most media businesses (including social media, newsletter & influencer businesses) are also flexible enough to comply with opportunity zone business requirements. Most e-commerce businesses can qualify. Many small local businesses can qualify if they are willing to be flexible on location. Real estate businesses can often qualify. Even some asset-heavy businesses such as manufacturers can qualify.

Let’s talk about exactly how to execute on this. (Also, this article is a real issue of the Axiom Alpha newsletter so if you want to learn about more financial strategies like this, subscribe to join our community of entrepreneurs & investors!)

How to create a QOF

A qualified opportunity fund (QOF) is a business entity used for a specific purpose and which satisfies certain conditions. Here are the five requirements and best practices to create your own qualified opportunity fund:

The QOF should be an LLC, LP, or C corporation. If it is an LLC or LP, then it must have at least two members/partners (single-member LLCs are not allowed).

It is incorporated in a U.S. state, DC, or a U.S. territory. If the business is incorporated or formed in a U.S. territory (rather than a state or DC), then it must be formed for the purpose of investing in opportunity zones only within that territory.

The business entity may be a pre-existing business entity. However, to minimize the chance of an audit, it’s highly recommended to form a new entity and include in its formation document that the entity is formed for the specific purpose of investing in qualified opportunity zone property.

The business entity must elect QOF status by filing form 8996 annually with its tax return.

At least 90% of its assets must be “qualified opportunity zone property” which can be any combination of (1) stock in a QOZB corporation, (2) partnership interest in a QOZB structured as an LLC or other pass-through partnership entity, and/or (3) qualified opportunity zone business property. However, this requirement doesn’t take effect immediately which means the QOF has time to find qualifying investments without rushing. Additionally, the 90% rule temporarily loosens if you deposit more cash into the QOF.

What is “qualified opportunity zone business property” (QOZB Property)?

(I know… I’m sorry for the word salad. Blame Congress.)

Qualified opportunity zone business property is tangible property that (1) has been or will be owned or leased (starting in 2018 or later) by a corporation or partnership, (2) is used in the active business of such corporation or partnership, and (3) falls into one of the allowed categories. The most common allowed categories are the following:

OZ real estate that you purchase and then “substantially improve” within 31 months. In this context, substantial improvement means spending as much in renovations as the cost of the original real estate minus the land value. Note: the 31 month requirement can be extended for government-caused permitting delays.

New construction real estate in an OZ.

Leased real estate in an OZ. You must have started leasing the property no earlier than 2018. Nobody is required to “substantially improve” such leased property in order for it to qualify as QOZB Property.

OZ real estate that you purchase from a local government who obtained the property through an involuntary transaction (e.g. due to nonpayment of tax by the homeowner).

OZ real estate that you purchase after it has been vacant for several years.

Any type of (new or used) machinery, equipment, or other tangible property which (1) can be depreciated or amortized and (2) has never been used in that particular opportunity zone by any business before. The property can be either owned or leased. There are even several safe harbor rules to include in this definition certain property which spends substantial time outside of an OZ. (e.g. a company truck which is normally parked at an office in an OZ but which is frequently driven out of the OZ for business).

Inventory produced by the business.

Some examples of property that are NOT qualified opportunity zone business property are:

Undeveloped land in an OZ which is not put to any significant active use. For example, someone purchases land primarily just to benefit from appreciation of the land over time, but they also let people pay $10 to park there during football games. (This fails to be QOZB Property because it fails requirement 2 above — it isn’t being used in an “active” business.)

OZ real estate leased out under a triple net lease. The IRS reasons that triple net leases are not an “active” business since the entire burden of property ownership is essentially transferred to the lessee.

A used commercial riding lawnmower bought from a landscaping company currently located in the same opportunity zone.

How to meet the QOF partnership requirement

Earlier, I mentioned that single member LLCs cannot be QOFs which is an annoyance to many people. However, the solution is very simple. Find a friend (or form an empty shell corporation if you have no friends) to buy a tiny fraction of the QOF (e.g. 0.01% or $1 or something like that). Wa-La — you now have a 2-member LLC which will be taxed as a partnership rather than a disregarded entity. I didn’t mention this technicality in my example of Kara, but she would have had to do this for her QOF.

How to create a QOZB

To create a qualified opportunity zone business, you’ll need to create a business entity that meets seven requirements:

The QOZB should be an LLC, LP, or C corporation. If it is an LLC or LP, then it must have at least two members/partners (single-member LLCs are not allowed).

It is an active business. Most “normal” businesses are active businesses. However, as previously mentioned, leasing real estate under a triple-net-lease is not.

At least 50% of the total gross income is derived from the conduct of a business in a qualified opportunity zone. There are several ways this requirement can be fulfilled (only one needs to be met): (a) at least 50% of the hours worked by partners, contractors, and employees could take place in an OZ, (b) at least 50% of compensation to partners, contractors, and employees could be for services performed within an opportunity zone, (c) the tangible property and management operations within an opportunity zone are necessary for the generation of at least 50% of the gross income of the business, or (d) the “facts and circumstances” (legal jargon) dictate that at least 50% of gross income is derived from active opportunity zone business operations.

At least 40% of the intangible property (e.g. patents, trademarks, etc) must be actively used inside a qualified opportunity zone. This is a slightly gray area since it’s difficult to assign a location to something like the use of a patent. In general though, things like using a trademark on the website of a business that has its office and employees in an OZ will probably count towards the 40%. On the other hand, a patent that was developed by a company operating outside of any OZ and which is later acquired by a QOZB might not count towards the required 40%.

At least 70% of the tangible property owned or leased by the business must be qualified opportunity zone business property. (We covered the definition of qualified opportunity zone business property in the previous section on QOFs).

No more than 5% of a QOZB’s assets can be “nonqualified financial property”. Nonqualified financial property includes most types of financial assets such as stocks and bonds but excludes cash, loans with a term of 18 months or less, and accounts receivable acquired in the ordinary course of business. There are some additional details around this rule, but they aren’t that important to most businesses. If you want to create any sort of business that relates to finance though, you’ll need to carefully look at all details.

The business is not a “sin” business or a company that leases property to a “sin” business. Sin businesses are: any private or commercial golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack or other facility used for gambling, or any store the principal business of which is the sale of alcoholic beverages for consumption off the premises.

Example 1

A landscaping company is set up as a C corporation. The company rents a small office with an adjacent fenced area of land where they store all of their trucks, driving lawn mowers, and other equipment. The office & land are inside an opportunity zone. All administrative work is done from the office. Every day, employees come pick up equipment and use it to service customers both inside and outside of the opportunity zone before returning the equipment at the end of the day. The business is a QOZB (unless it does something unexpected like buy a million dollars of stock which might jeopardize the 5% limit on nonqualified financial property).

Example 2

Amanda & Mike live together in an opportunity zone. They decide to create a Youtube channel together. They create a 2-member LLC (they are the two members) to run their Youtube business. They operate from a home-based office and earn revenue through youtube ads, sponsors, and Amazon affiliate sales. The business is a QOZB.

Example 3

Joe sets up a C corporation that buys some barren land in an OZ in Colorado. He contracts engineers and developers to level the land, to build a small office building, and to add gravel roads and RV sized parking spaces. He also plumbs in a septic system and RV hookups for water, sewage, and electricity. He then begins operating the new RV park. The RV park is a QOZB.

Example 4

The IRS’ Final Regulations on QOZB’s gave a rather interesting but nuanced example of an intellectual property holding company with a headquarters in an QZ which DID qualify as a QOZB despite concerns about the 40% intangible property rule. This is a very relevant example for many tech companies which may be able to structure either themselves or a subsidiary as a similar IP holding company that can generate major tax breaks.

How startups & small businesses can find eager investors

There are a lot of investors who are aware of opportunity zones but don’t want more real estate exposure and don’t know of any good businesses which are both QOZBs and currently raising money. In fact, many investors don’t fully understand the regulations. They think of QOZBs as being hair salons in bad neighborhoods. Now that you know how flexible the definition is, you can use it to your advantage. If you can become a QOZB, then go knock on some doors or cold email some inboxes. Target family offices in your area. Family offices are special investment businesses which manage the wealth of one very wealthy individual or family. They are always looking for new investment opportunities, and because they Many family offices are more flexible than VCs and would be very interested in investing in a QOZB. You can also approach angel investors and alumni from any universities you’ve attended.

You can pitch that your business will be a QOZB and that you will set up a QOF through which they can easily invest. If you actually want to run with this strategy and have questions, feel free to email me using the form at the end of this letter.

How a company can directly benefit from an OZ

We’ve talked about how the people who start and invest in companies can benefit from OZ tax breaks, but OZs can also help companies themselves. One way OZ tax rules can help is by making it easier to get investors as I just mentioned. However, another way is for a company to simply use the rules in the same way a human would: by reinvesting realized capital gains.

Capital gains for a company could be from selling real estate it previously used in its business, from selling stock in a subsidiary, or from selling a partnership interest in a joint venture.

For companies that have more than a couple months of cash in the bank, it’s also very advantageous to hold a portion of that excess value in stocks or other assets expected to generate more return than the 0.1% interest rate a bank might offer. From time to time, such holdings would be adjusted which can generate capital gains for the company.

Once the company has capital gains to reinvest, it might purchase a new office building or warehouse in an opportunity zone through a QOF. Alternatively, it might start a new line of business through a two-tier QOF-QOZB subsidiary. Doing so is prudent for new lines of business which are somewhat experimental or adjacent to the company’s primary line of business. Then if the new line of business doesn’t work out for the company for some reason or if the company falls on hard times and needs cash, it can sell the subsidiary tax-free.

Big corporations also frequently have venture capital arms where they invest in new companies in their industry. This gives them a way to hedge the risk that one of those companies becomes a serious threat to their own. It also gives them a foot in the door to acquire that startup if they do become a threat or if they have some technology that the big corporation needs. If the startup can qualify as a QOZB, then the big corporation would be foolish not to invest through a QOF to obtain the extra tax benefit.

The more successful a business becomes, the more capital gains it is likely to have and thus the more incentive it has to take advantage of opportunity zones. However, even small companies can directly profit from OZs by compartmentalizing any aspect of their business which is separable from the whole into a QOF-QOZB two-tier subsidiary. In fact, you as a founder can even simultaneously hold your main company through a QOF while your main company itself has one or more QOF subsidiaries. I know that sounds a bit convoluted, but it’s very possible to do and can enable both you and your company to retain huge amounts of money that would otherwise be paid in taxes. However, if your company gets big enough to justify owning real estate, you can get all of that plus MORE by combining the benefit of tax-free gains with the benefit of real estate depreciation.

The double benefit of OZ real estate

Penelope buys a residential duplex for $1.25 million in 2022. According to the tax appraisal, 20% of the value ($250k) is attributable to the land while 80% of the value ($1 million) is attributable to the building. Penelope operates the property as a rental property until the year 2047 when she sells the property for $3.75 million ($2.5 million over her original purchase price).

Assuming Penelope qualifies (via her income or real estate professional status), she can take a deduction of 3.64% of the building’s value each year for 27.5 years. Since Penelope bought in 2022 and sold in 2047 (a 25 year holding period), her cumulative deduction is 91% of the building value. That’s $910k = 91% of $1 million.

However, when Penelope sells her property, she isn’t just taxed on the $2.5 million appreciation of the property. She is also taxed on $910k of “depreciation recapture” (and this recapture is taxed at a rate up to 25% rather than the maximum 20% long term capital gains rate). That’s how ordinary real estate depreciation works — it’s merely a tax deferral mechanism not a tax elimination mechanism.

Now let’s compare what would happen if Penelope were to do exactly the same thing except this time she bought her property through a QOF.

In this case, since 25 years is more than 10 years, we already know that Penelope won’t owe capital gains taxes on the $2.5 million of appreciation. However, the OZ tax rule doesn’t just apply to capital gains. It also applies to depreciation recapture. This means Penelope doesn’t have to pay 20% long term capital gains on her $2.5 million appreciation AND she doesn’t have to pay 25% depreciation recapture gains on the $910k of deductions she took. Penelope pays ZERO taxes on anything AND she still gets to deduct depreciation.

That is unlike any other tax loophole. The no-payback deductions alone are equivalent to getting a massive government subsidy on purchases of OZ property. Imagine getting to buy a stock that generates dividends, write off the cost of the stock, receive dividends for 25 years, and eventually sell the stock at a gain without paying any taxes on that gain or repaying the deduction. That’s exactly what this is but for real estate & rental income rather than a stock & dividends.

How to use QOFs for a startup if you don’t have capital gains

If you have $1000 in your bank account and want to create a startup with that $1000, you won’t be able to benefit from the QOF tax-free exit. The reason is that you can only invest money coming from capital gains into the fund. Unfortunately that means just having money isn’t enough to create your tax-privileged startup. However, there are some creative ways you can try to get around this.

The fortunate thing is that most startup founders don’t put much of their own money into a startup (because most founders don’t even have much money). That means you don’t need much capital gain to benefit from the eventual tax break. In fact, hypothetically you could probably make do with as little as $10. Many founders will have that already in the form of unrecognized gains from crypto or Robinhood stocks. If you truly have zero capital gains though, then try this:

Buy 10 different stocks. Choose randomly if you know nothing about stocks. The more volatile the stocks, the better. Watch them each day and whenever one is up by more than 3%, sell it and then reinvest the principal (but not the gain) into a new stock. Don’t sell anything at a loss until the next year.

That’s not the best strategy for investing generally, but it’s a great way to get at least $10 in realized capital gains. Once you have those realized capital gains, you can contribute it to your startup through a QOF. Of course, you may need more than just $10, and that’s fine. As long as you have SOME realized capital gains, you can contribute the remaining money needed to your startup as a loan rather than as an equity purchase. QOZBs can take loan money without any issue about whether or not the loan money comes from capital gains or not.

Note: If you are finance nerd who regularly trades stocks or crypto, you can do better than this by simply using wash sale gains that would normally be an annoyance. If you don’t know what that means but want to use the strategy in this section, email me what your situation is, and I’ll give you my thoughts. If you don’t execute on the strategy appropriately, you risk losing your tax privileges under the “anti-abuse” regulations for OZs.

Future political risks & opportunities

Political winds can always change the tax law. Opportunity zone tax laws had huge bipartisan support when they passed a few years ago so it’s unlikely that those will be substantially changed. However, there are definitely strong political battles ongoing about taxes. Here are 6 changes to the tax law that can indirectly affect opportunity zone businesses & investments:

Long-term capital gains may lose their tax-privileged status and become taxable at ordinary income rates. This change is currently included in Biden’s proposed tax changes. If this happens, it makes the tax-free haven of OZ investments substantially more valuable since you would save about twice as much in taxes as currently.

The corporate tax rate may increase. For the same reason as above, this would make OZ investments much more valuable to corporations which have capital gains.

Individual ordinary income tax rates may increase. If this happens in conjunction with long term capital gains being classified as ordinary income (both things are included in Biden’s current proposal), it would make OZ investments more valuable. Additionally, in this scenario it’s likely that the maximum real estate depreciation recapture tax rate would increase from 25% to the ordinary income tax rate. That would strongly incentivize real estate investors to move into OZs. That in turn would create an opportuntiy for QOZBs already set up to quickly & easily accept more investment. It also could lead to significant local disparities in real estate performance as investors pile into opportunity zones and dump buildings in adjacent, non-OZ census tracts. This is an opportunity for fast-moving QOZB small businesses and startups but also a risk to real estate investors holding property in OZ-adjacent census tracts.

Tax deferred 1031 exchanges may be eliminated or capped at a low threshold. If you are a real estate investor, diversifying into opportunity zone investments is a valuable way to hedge this risk. Additionally, holding OZ property would be an interesting way to speculate on legislative elimination of 1031 exchanges. If 1031 is eliminated, investor demand will shift heavily towards OZ’s which will drive up your property value and enable you to profitably exit your OZ investment early (without the tax benefits but with lots of profit). If 1031 is not eliminated, you still own the OZ property and can generate both cash flow and long-term tax-free gains. It’s a win-win scenario for people and companies getting into OZs early enough.

In April 2022, a new bipartisan bill was introduced to Congress which would modify the opportunity zone laws in a few ways. These bills are currently just early-stage proposals, but here are the most important changes they could have: (1) phasing out certain opportunity zones based on new income criteria and updated 2020 census data, (2) adding new reporting requirements for QOFs, and (3) extending the tax deferral window from 2026 to 2028. The first two are minor annoyances but are easily handled with appropriate planning. The third point is very interesting because not only would it increase the direct tax deferral benefit, it would also reactivate an old opportunity zone benefit which already expired under the current law. If reactivated, the new version of that benefit would give anyone who gets into OZ’s before the end of 2022 a 15% discount on their deferred taxes when they eventually paid them. It would also give a 10% benefit to anyone who gets into OZ’s before the end of 2023.

If Biden’s “billionaire” tax proposal (which has been cleverly named so that people don’t realize it doesn’t only apply to billionaires) is passed, it could have a substantial effect on OZs. In its current form, the tax is actually a prepayment of a portion of capital gains tax. This leaves open the possibility for wealthy individuals and companies to avoid the billionaire minimum tax by migrating assets into OZ property and businesses which are not subject to capital gain tax if held long enough.

The summary version of all those points is that political winds towards higher & more taxes just make opportunity zones more valuable. Furthermore, the fact that opportunity zones have strong bipartisan support means they are probably the best safe harbor for wealthy individuals and companies to ride out a decade or two of tax law tightening.

And if you’re interested in using QOFs or QOZBs, shoot me an email with a brief description of what you’re interested in doing. My company consults & partners with entrepreneurs and investors to help them make more money by structuring businesses & deals, helping them to develop and execute tax and financial strategies, and helping them identify new opportunities. Unlike many internet forms, this one will get you a real response from a real human being with deep financial competency.

Appendix A: Business model risk factors

There are three important issues that startups are likely to come across if they want to maintain QOZB status as they grow.

1. Avoid cloud infrastructure agreements that may be deemed “leases”

Cloud computing & data storage is provided through “service contracts” or “service level agreements” (SLAs) which can have very different terms. The more control over the hardware and the more liability for performance that you assume rather than the cloud provider, the higher the risk that the IRS will deem the agreement to actually be a “lease” even if it’s called a “service contract”.

Since a successful asset-light software business will typically use far more cloud machinery than onsite machinery, it’s very important for such a business to NOT have cloud infrastructure count as “leased tangible property” since most of that property is not located within opportunity zones. Feel free to email me if you’re thinking of adopting a QOZB strategy and want to get an idea of whether your company’s cloud usage is likely to be problematic or not.

2. Be cautious with acquisitions

If you anticipate growing your company through acquisitions, then you’ll need to take precautions. There are four possible routes to take without entirely losing your OZ benefits.

The first route is to not use this hierarchy of ownership:

You –> QOF –> main company C corp

but instead this hierarchy of ownership:

You –> holding company C corp –> QOF –> main company C corp

Any acquisitions of other businesses would then be done through the holding company above the level of the QOF. This is a very flexible approach because it also frees you to form other operating subsidiaries of the holding company if your company needs to expand to include offices or teams outside opportunity zones. The main drawback is that you no longer can sell your (top level holding) company tax-free. However, your holding company will still have the ability to sell its QOF subsidiaries (including your original main company) tax-free.

The second route is to structure any acquisitions as asset purchases. That can be very difficult to do if you’re acquiring a large company with a lot of employees and/or tangible assets, but if you’re acquiring relatively lean startups with few employees and few tangible assets, it’s very feasible to accomplish this. There are some considerations regarding the “location” of intangible intellectual property such as patents and trademarks that you’ll need to account for though so consult with an expert if you reach this stage if you don’t want to read the hundreds of pages of regulation yourself.