“My outdoors Youtube business brings in $40-50k per month, but I knocked down my tax bill by buying 4 fishing boats.”

— Noah (a Florida man)

Unfortunately, Noah (not his real name) understood just enough about taxes to shoot his business in the foot. Noah understood that 100% bonus depreciation (a powerful tax loophole which begins phasing out on January 1, 2023) would allow him to write-off 100% of the cost of qualifying business equipment. Noah also understood that due to the nature of his business (an outdoors themed Youtube channel which featured lots of fishing), fishing boats would qualify as business equipment. What Noah didn’t fully understand is that depreciation of business equipment is only temporary–you have to repay it eventually either through real physical loss of value or through paying more taxes at a later date. In this letter, I’ll explain exactly how Noah went wrong, how much his mistakes will cost him in the long run, and how you can avoid making the types of mistakes Noah made.

Noah’s big mistake

Noah spent about $50k on each boat. Purchasing all 4 boats cost him $200k which allowed him a $200k deduction. Given Noah’s typical revenue of $40-50k per month, the entire $200k deduction probably took place in the 35% tax bracket. That means Noah’s boat purchases reduced his 2021 tax bill by $70k = 0.35 * $200k. It also means he locked up $130k that he would have otherwise had in cash. This latter fact is the primary cause of Noah’s future problems. Let’s consider the three possible outcomes that can happen over the next several years.

Scenario #1: Noah uses the boats for a few years and then sells them for the same amount he bought them for. When he sells the boats, Noah will owe taxes on the entire sale amount of $200k (because he took a full $200k deduction in the year he bought the boats). Furthermore, since he took the deduction against ordinary income, that $200k from the sale is now taxed at ordinary income rates, not long-term capital gains rates. The taxes are exactly the same as he would have owed in 2021 if he not bought the boats: $70k. The boat purchase only allowed Noah to accomplish two things: (1) delay paying the $70k for however long he owns the boats and (2) keep the $70k of capital locked into a business asset in the meantime. It’s basically like the IRS is giving Noah a 0% loan of $70k which he doesn’t have to pay back as long as the money is locked into business assets.

Whether or not scenario #1 results in a better outcome than not buying the boats depends on whether

the additional business revenue Noah can generate with the $200k worth of boats, or

the income Noah could have generated by investing the $130k he would have had if he just paid the tax and not bought the boats

is more money.

For example, suppose Noah keeps the boats for 5 years. Before purchasing those boats, he already had 2 others. When I asked, Noah didn’t have any particular answer for how exactly his new four boats would allow him to make more Youtube videos or get more views. Optimistically then, let’s suppose that after paying marina fees, slip rent, boat maintenance costs, and fuel costs, he earns an extra $2k / year in profit. In reality, boats are very expensive to keep and maintain so it seems likely that Noah may not even make $2k extra after all expenses are paid, but we will assume he does make that profit each year. Over 5 years, he racks up an extra $10k in pre-tax profit. After taxes at 35%, he ends up with an extra $6.5k in profit. His $130k has become $136.5k after taxes.

Now consider the hypothetical alternative: Noah paid the $70k in taxes and kept the $130k in cash. He then invests the cash into the stock market. The stock market doesn’t guarantee any particular return, but over decades it does consistently produce an average annual return of about 10% per year. If Noah invested all $130k for 5 years with a 10% average annual return, then he would end up with $209.37k. If he chose to sell at the end of that period, he would pay long-term capital gains tax on the $79.37k profit. Assuming a 20% capital gains tax rate, that means Noah would have a post tax profit of $63.49k = 0.8 * $79.37k. In the end, he has turned his $130k into $193.49k after all taxes. That’s ***WAAYYYY*** better than if he had bought the boats!

Scenario #2: Everything is the same as Scenario #1, except we add in the reality that boats depreciate over time (physically wear down I mean, not just depreciate for tax purposes). If the boats depreciate 20% over the 5 years that Noah owns them, then what he bought for $200k he can only resell for $160k. Noah then owes ordinary income taxes on $160k instead of on $200k. Staying with our assumption that the proceeds fall into the 35% tax bracket, that means Noah owes $56k = 0.35 * $160k in taxes on the sale. Post-taxes, the sale leaves him with $160k – $56k = $104k. If we include the $6.5k in extra post-tax profit we calculated in Scenario #1, then at the end of the 5 years after all taxes are paid, Noah has $104k + $6.5k = $110.5k. He could have had $130k if he had just paid the taxes originally and put the cash in a zero interest bank account, or he could have had something like $193.49k if he had invested the $130k in the stock market (as we calculated before). This is an even worse outcome than Scenario #1!

Scenario #3: Noah keeps the boat forever. I won’t even do the exact math on this, because it would be so bad. The entire $130k Noah would have had if he had just paid the tax initially will eventually go to near zero as each boat’s real physical value diminishes and requires more and more maintenance. The combination of never paying the $70k in taxes and the tiny ROI on the boats ($2k / year) will be vastly outweighed by the real loss of value in the boats over time and the massive opportunity cost of not investing the $130k he could have had in the stock market. Compounding $130k at 10%/year for 10 years results in $795k before taxes… Noah tried to avoid $70k in taxes and by doing so, lost out on 10 times that amount in future opportunity.

What Noah could have done

Noah’s mistake can be summarized in one sentence: he made a financial decision based only on this year’s tax situation rather than a proper comparison of tax savings vs opportunity cost of getting those tax savings over the next several years.

When it comes to depreciating business equipment, the single most important thing to understand is that net benefit or cost depends on the time value of money. In other words, using equipment depreciation to delay taxes is only beneficial to the extent you can generate meaningful additional revenue from the equipment. If the equipment has little potential to increase revenue and moderate potential to incur extra maintenance costs, then delaying taxes to purchase the equipment is probably a bad idea. Stated like that, it sounds simple. It is simple, but you have to actually take the time to estimate revenues and maintenance costs. You’d probably be surprised how many entrepreneurs make the same sort of mistake as Noah.

Here is a basic decision process you can use to help you decide whether or not to buy a particular piece of business equipment that’s eligible for 100% deduction (note: this doesn’t include any type of inventory, consumables, or real estate — those each have different tax treatment).

Does the equipment cost more than $1,000 or does it seem expensive to you? If yes to either, then go to step 2. If not, buy the equipment–no need to proceed further.

Do you *need* the equipment to operate your business? If so, buy it. The tax deduction is just a bonus in this case since you need to buy the equipment no matter what in order to operate the business. If you don’t *need* it, then go to step 3.

Did you arrive at the idea to buy the equipment by thinking about how to grow your business or how to reduce taxes? If your original motivation was to grow your business, without considering taxes, then buy the equipment. You might still be wrong to do so, but if so that’s not so much a finance problem as an opportunity to learn from the mistake and develop your general business judgement. On the other hand, if your original motivation did involve tax considerations to partially or wholly justify the idea, then go to step 4.

Estimate the amount of tax money you’d save by multiplying your top marginal tax bracket by the cost of the equipment. I’ll call this number “Tax”. (e.g. for Noah’s $200k purchase at a 35% tax rate, Tax = $70k = 0.35 * $200k).

Calculate the amount of your own non-tax-savings money that would be put into the purchase. I’ll call this number “Equity”. (e.g. Noah spent $200k with Tax = $70k which means Equity = $200k – Tax = $130k).

Estimate how much additional annual revenue the equipment could enable your business to generate. I’ll call this number “R”. Estimating R is the hardest step with the most uncertainty, but it is necessary. A very simple, rough estimate is fine if it’s all you can manage.

Estimate your annual maintenance costs for this piece of equipment. I’ll call this number “M”. Again, a simple rough estimate is better than nothing.

Calculate the estimated additional annual profit “P” = R – M

Calculate the annual return on equity (ROE) as follows: ROE = P / Equity

If ROE is greater than 0.1, then buy the equipment. If not, then don’t.

If you’re good at math, you may have already noted several ways to improve the process as you were reading it. Even as it stands though, it’s a useful decision-making aid that can help you prevent enormous mistakes like Noah made with his boats. He would have gone through the process as:

Yes

No

Yes

Tax = $70k

Equity = $200k – Tax = $200k – $70k = $130k

R = $12k

M = $10k

P = R – M = $2k

ROE = P / equity = $2k / $130k = 0.015

Since 0.015 is NOT greater than 0.1, the answer is DON’T BUY

This process actually gives you more than just a binary answer. It gives you a framework to test different possibilities.

What if Noah could decrease maintenance costs to just $5k / year? Well, change the value of M in step 7 and then go through the remaining steps 8-10 to see what changes.

Or what if Noah hired a retired professional fisherman to do chartered fishing day trips, advertised as Airbnb experiences, without Noah ever being involved? That actually has the potential to scale Noah’s business enough to make the boat purchases worthwhile.

“Nobody owes any public duty to pay more than the law demands: taxes are enforced exactions, not voluntary contributions.”

— Judge Learned Hand (Yes, surprisingly that was his real name!)

Whether you’re a small business owner, the founder of a fast-growing startup, or a high-income individual, knowledge of the tax code is even more powerful than compound interest.

Start with $1 and grow linearly at $0.10/year for 30 years. You end with $4. That’s labor.

Start with $1 and compound at 10%/year for 30 years. You end with $17.45! That’s compound interest (i.e. that’s business growth or investment).

Start with $1 and compound at 7%/year for 30 years. You end with $7.61. That’s a 30% tax rate on your business growth.

Cheeky statements aside, the point I’m illustrating is that the difference between untaxed exponential growth and taxed exponential growth is often BIGGER than the difference between taxed exponential growth and boring straight-line financial growth. That means investing the time necessary to understand key aspects of the tax code & strategize with them can be one of THE BIGGEST needle movers for your long-term success. Jeff Bezos knew this, which is why Amazon has been tax-optimizing since the beginning. It’s also why some really smart people struggle financially while some pretty basic people are able to become millionaires. It’s also why most of the 25+ million small businesses that record taxes as their single largest expense are doomed to underperform their more tax-efficient competitors.

I’m going to go over each of the most useful and powerful tax rules and loopholes with all of the key details you need to know about each in order to use them. However, I cannot cover them all in a single article. So, this will be the first of several articles over the next couple of weeks that will constitute my “tax series” in honor of tax season. By the end, you’ll be a nearly lethal tax assassin: slaying rather than paying most taxes in your path.

Lesson #1: You’ll always be a sucker if you don’t own something.

Almost every “loophole” in the tax code is actually a purposefully added incentive to own or buy some sort of property (the term property includes not just real estate but also vehicles, machinery, equipment, stock in a corporation, a percentage ownership of an LLC, etc).

Loopholes generally fall into one of two categories: (1) deductions (also called “write-offs”) or (2) credits. They are not the same. A deduction is subtracted from your taxable income before computing taxes. A credit is subtracted directly from your taxes after computing them initially. That means a dollar of tax credits is almost 3 times more valuable than a dollar of deductions for individuals in the highest tax bracket (37%), and the difference is even larger for corporations and lower-income individuals.

Example:

A corporation makes $100k of income. Since the corporate tax rate is 21%, the company would pay $21,000 of federal income tax.

If the corporation found a $10k tax deduction, their taxable income would drop from $100k to $90k, and the taxes owed would be 0.21 * $90,000 = $18,900 (a $2,100 savings).

If instead the corporation found a $10k tax credit, their taxable income would remain $100k, but the federal income tax would drop to $21,000 – $10,000 = $11,000 (a $10,000 savings).

In the remainder of this article I’ll describe one of the best tax loopholes related to home ownership.

NOTE TO FIRST-TIME STARTUP FOUNDERS (Everyone else, skip ahead to the next paragraph): If you’re anything like I was 8 years ago, you may be tempted to ignore this homeowner stuff to focus entirely on your business. Here’s exactly why you shouldn’t. The average first round of funding (sometimes called the seed or pre-seed round) for startups is typically around $15,000 – $200,000 for 5-25% of the business’s equity. Many first-time founders don’t have that much money, so they take the investment. But that amount of equity is actually quite significant. After all the rounds of investment Amazon has taken, Jeff Bezos only owns 10% of Amazon. Yet he has a net worth of $100B+. If founders were able to bootstrap long enough to avoid that need for early capital, they would end up significantly better off in the future. That’s where home ownership comes in. With an FHA loan, you can put down just 3.5% on a home, and it will become your investor. Not only will you be able to pay less to live than you would have otherwise had to pay in rent, but even a 10% rise in home prices would give you access to 3x your down payment amount through a low-interest-rate home equity loan. You can also rent out spare rooms (or the entire house if you move) to cover the mortgage payments and live for free while you work on your startup. And that’s just the start.

The Mortgage Point Loophole

Applies To: Humans only (not businesses)

How it Works: If you take out a mortgage of less than $750k to buy or build a primary residence, then you can take a deduction for the interest you pay on that loan each year.

For example, if you take out a $500k mortgage with a 4% interest rate to buy a home in January, then you’d pay about 0.04 * $500k = $20k in interest that year. You can then deduct that entire amount on your tax return. It gets even better though.

The tax code allows you to deduct mortgage discount points (which are essentially prepaid interest) in the same way as you deduct mortgage interest, EXCEPT that you can only deduct mortgage points on a mortgage loan taken out to buy or build a primary residence. You cannot deduct points for a second home or investment property.

A mortgage discount point is a percentage discount in your mortgage rate (most typically 0.25% so that e.g. buying one point would drop a 4% mortgage rate to a 3.75% mortgage rate). The cost of buying a mortgage point is almost always 1% of the total mortgage loan amount.

The math works out so that buying a mortgage point is the same as paying a small sum upfront rather than a larger sum over the duration of the mortgage loan. However, even though buying a point saves you money over the long-term, it also costs you more money during the first year (because the 1% you spent is more than the 0.25% you saved during the first year).

This creates the perfect tax setup because not only do you pay less interest, but you simultaneously pull forward a huge chunk of interest expense that you can write-off in the current year to offset other income. If you take out the maximum mortgage size allowed for this rule ($750k) and buy 4 points, you’d get a deduction of 4 * 0.01 * $750k = $30k. And that’s just from the points! You still get to also deduct any interest payments you make on the house that year.

Example

Florida man Gus buys a primary residence with a $750k mortgage by June of this year. His initial mortgage rate is 4%, but he buys three discount points that each provide a 0.25% discount. That means he pays 3 * 0.01 * $750k = $22.5k for the points, and his final interest rate is 3.25%. Since he bought the home before June, he still has at least half a year’s worth of interest payments to make. Those payments are about 0.5 * 0.0325 * $750k = $12.2k.

Gus’s total deduction attributable to interest on his primary residence is then the sum $22.5k + $12.2k = $34.7k. Not bad!

Bonus Benefits

Bonus #1: When you try to get clever with taxes, you can sometimes run into the very annoying “Alternative Minimum Tax” (AMT). The AMT is a whole second method of computing taxes which has a lower top bracket rate but also disallows many deductions. However, the type of primary residence acquisition mortgage interest deduction described in this loophole is allowed under both the regular and alternative minimum tax methods — Hurray!

Bonus #2: If you don’t fall into AMT territory, you can also deduct up to $10,000 in property taxes in addition to the interest deductions.

Bonus #3: If you are someone who typically takes the standard deduction, then buying a home without mortgage points may be wasteful from a tax perspective. To see why, you have to look at the big picture over several years rather than just one year. Suppose you take out a $250k mortgage at 4%. Your yearly interest payments will start off around 0.04 * $250k = $10k. If that was the only itemized deduction you could take, then it wouldn’t be worth even taking it since the standard, non-itemized deduction for an individual is over $12.5k. That means over the next 10 years, you’d have had tens of thousands of dollars of accumulated interest payments that couldn’t be deducted. However, if instead you purchased 4 mortgage points (costing 4 * 0.01 * $250k = $10k), then your total first year interest costs would be $10k (for points) + $7.5k (for interest payments at 3% since that is your final rate after buying 4 points) = $17.5k. Not only do you have an extra $5k deduction in that first year, but you also pay less interest and lose out on fewer deductions in later years. If that all seems confusing, just remember that if you typically take the standard deduction, then it benefits you to concentrate any non-standard deductions into a specific year.

Remember the big picture

Never forget that the high-level goal is to build wealth not minimize taxes. The deduction I’ve described is a DEDUCTION, not a CREDIT. It makes no sense to spend an extra $100k on a primary residence just to get a $100k deduction which saves you less than $50k in taxes. You can spend extra money buying points, but don’t buy a more expensive home than you otherwise would. The only exception to this would be if you plan to tax-hack by living in the house for the first year and then turning it into a rental property.

How many points should you buy?

After reading all of this, you may be tempted to buy as many mortgage points as your lender will sell you. Not so fast. Remember: The goal is to build wealth, not minimize taxes. The mortgage interest loophole is a DEDUCTION not a CREDIT. That means even if you’re in the highest tax bracket, only 37% of the amount you spend on points will be directly saved in taxes (even less if you’re in a lower tax bracket). Since 100% of the amount spent goes to reducing future interest expense, that means you’ve turned $1 into $1.37. BUT, that is dependent on one important assumption: that interest rates won’t drop significantly in the future. That’s because if interest rates drop, then you prepaid at a higher rate than you would have had to pay in the future which means rather than eliminating $1 worth of future interest rate payments for your $1 spent on points, you are maybe only eliminated $0.80 worth of future interest rate payments.

You can tolerate a small drop (e.g. using the numbers above, you paid $1 for $0.80 of interest benefits but also got $0.37 of tax benefits, leaving you with $1.17 overall). If interest rates drop significantly though, then maybe you prepaid $1 for only $0.50 of interest benefit, which means even including the tax benefit, you’re left with only $0.87 worth of value when you paid $1. That’s bad.

For the past 40 years, interest rates have been trending down. You can see that clearly in the chart below. The chart shows the interest rate on 10-year U.S. government treasury bonds (this rate is often just called the “10-year yield”). On average, 30-year mortgage interest rates tend to float about 2% over whatever the 10-year yield is.

All the way at the right side of the chart, you can see we are near all-time lows right now, so the risk of interest rate drops is not very large. However, as of 2022, the Federal Reserve has begun implementing a planned series of interest rate hikes. Those increases, together with the momentum of the increases (which will cause the gap between 10-year treasury rates and 30-year mortgage rates to likely remain higher than 2%), mean that mortgage rates will likely reach higher levels in 2023 or 2024 than the economy can withstand without a downturn.

Regardless of whether we officially enter a recession (definitely possible within the next 18 months) or just slow down a bit economically, it’s likely that interest rates will drop sometime thereafter in response. Then the cascade of interest rates will begin. The 10-year yield will come down from its highs, back to 2-3% at most. That in turn means 30-year fixed mortgage rates will probably fall down to 4-5% at most. It’s impossible to say what the exact timeframe of that rise and fall of interest rates will be, but I’d place odds that interest rates have fallen back to the levels I described within 5-10 years.

The reason I bring all of this up is that if 30-year mortgage rates rise to 7%, it doesn’t make financial sense to buy a fixed rate mortgage if you expect mortgage rates to fall back to 5% or lower (and it especially doesn’t make sense to prepay interest through points on that kind of mortgage). Instead, buying some type of variable rate mortgage loan would be preferable.

If I wanted to implement this strategy today, I would use a type of mortgage called a “10/6 ARM” and buy as many points as possible without pushing the “break-even” date of buying the points (vs just paying the interest) more than 10 years into the future and without the final interest rate dropping below 4%.

If you enjoyed this article, subscribe to the Axiom Alpha email newsletter which I publish 1-2 times a week typically. I write about tax strategies, the economics of different industries and business models, and more content aimed at giving entrepreneurs and investors superpowered nuggets of hyperpractical business & finance tactics. Join the community!

Appendix: Mortgage Point Limitations

Every great tax loophole has its limitations and compliance requirements. The IRS has 9 requirements that must be met in order for you to deduct mortgage points (some of these I’ve already mentioned):

The mortgage loan must be secured by your primary residence (the home where you ordinarily live most of the time).

You must use the loan money to buy or build your primary residence (so you can’t take out a mortgage to buy a second home NOR can you take a home equity loan out of your home to pay off credit card debt, for example).

Paying for points must be an established business practice in the area where the loan was made (you can check this by calling a bank or other mortgage lender in your area).

The points paid weren’t more than the points generally charged in the area.

You use the cash method of accounting. This means you report income in the year you receive it and deduct expenses in the year you pay them. Most individuals use this.

The points weren’t paid in place of amounts that are ordinarily stated separately on the settlement statement (e.g. appraisal fees, inspection fees, title fees, attorney fees, property taxes). The points MUST be “mortgage discount points” rather than any other type of “point” such as an “origination point” which doesn’t correspond to a deduction in interest rate.

The total amount of money you provided before or at closing (including down payment, an escrow deposit, earnest money, and other funds you paid at or before closing for any purpose) must be at least as much as the cost of all the points you purchased.

The points were figured as a percentage of the principal amount of the mortgage (i.e. 1 point costs 1% rather than 1 point costs $500 without regard for the total mortgage amount).

The cost of the points is clearly shown on the settlement statement (e.g. Form HUD-1) as points charged for the mortgage. The points may be shown as paid from either your funds or the seller’s.

Business conferences are profitable — How a noob made $57k in 2 months

“I put up a crappy website and started creating content. In just 7 weeks, somehow we had 400 ticket sales, and we made $50,000.”

Sam Parr

In 2014, the man behind the hotdog stand business “Southern Sam’s: Weiners as Big as a Baby’s Arm” decided to organize a conference for non-technical founders.

Sam had never before organized or even been to a conference. He had no personal connections with anyone qualified to speak at such a conference. In this letter, I’ll show you EXACTLY how Sam did this, including a spreadsheet breaking down what his exact expenses and sponsorship revenues were at the end.

Armed with nothing more than youth and blissful ignorance, Sam began trying to recruit founders of successful companies to speak at his conference. In his first pitches, Sam tried to convince them to come by explaining how fun the event would be or how they could grow their business because there would be an audience of 400 people. That strategy got him exactly nowhere.

So he made two changes to his pitch.

First, Sam increased the audience size with only a marginal increase to his costs by creating a Udemy course that would have video from the event. He managed to get a couple thousand people signed up for the course.

Second, he stopped telling founders how much business they would generate from the event. Instead, he asked them to “come spread your company’s gospel” to the conference’s audience of smart enterprising “do-ers”.

By simple word choice (religious words and phrasing), Sam’s message flattered prospective speakers by making them “god-level” business authorities. Even more importantly, the focus was no longer on the questionable amount of business that a small conference could realistically generate, given that the audience wasn’t the target customer for most of the speakers’ companies. Instead, the focus was placed on the much more valuable fact that the audience was composed of intelligent, action-oriented business people. This matters because one of the big issues that CEOs of growing startups face is hiring top talent. A few customers wouldn’t move the needle for these speakers, but a couple good recruits could. There is a reason, after all, that startups sometimes pay recruiters upwards of $30k for a single hire. (Note: After the first HustleCon, Sam realized the full extent to which this was true. He made the recruiting value proposition even more explicit when approaching potential speakers for the second HustleCon by offering to post any open job positions of a speaker’s company on the HustleCon website).

Closing Speakers

Sam’s effectiveness in closing speakers went from zero to IMPRESSIVE after implementing those two changes.

He still got some rejections. He still had to be persistent–sometimes following up with 5-10 emails before getting a response. But that’s the price of getting the attention of someone who’s very busy and successful when you’re a nobody, and it’s a pretty low price if you ask me. And it worked!

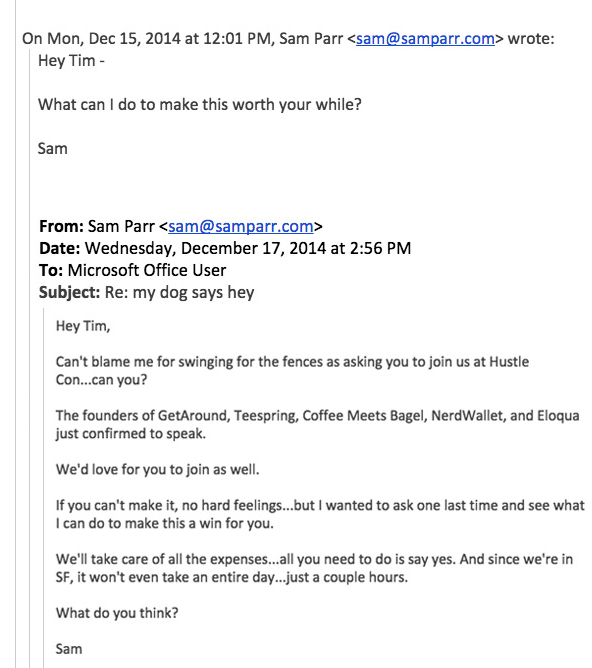

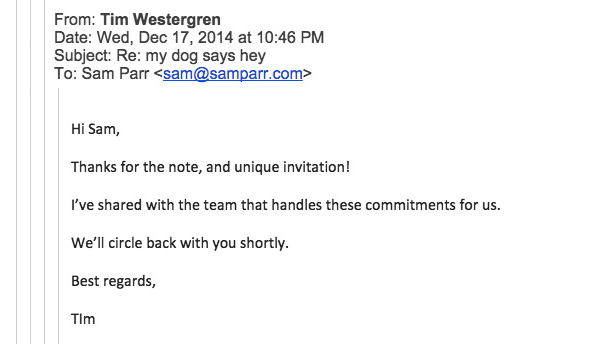

Sam got 12 successful founders to agree to come speak at his conference within a few weeks, even though none of them had ever heard of him or his conference before. And to make it even more impressive: He didn’t pay any of them, and only paid the travel costs for one of them.

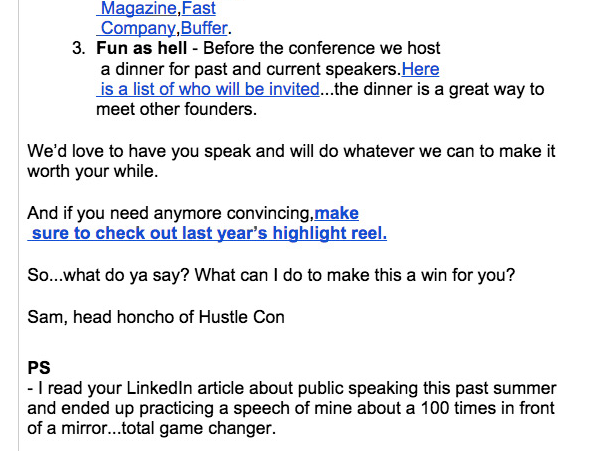

Here’s one of the real emails he sent to the founder of Pandora (he actually sent this one for the second HustleCon, but it’s the same strategy he used for the first one):

From the subject line to the personalized GIF to the “PS” message which communicates that Sam values and follows the advice of recipient, this is a perfect example of what Sam calls an “irresistable email”. But it still needed several follow-ups before it got a response.

But eventually the same persistence that drove Sam’s massive wiener business to success also brought Tim Westergren around!

How to Bypass Planning Problems

There are two main ways to make money from conferences: selling tickets and selling sponsorships.

However, many people who try to host a conference never get off the ground because conference planning can easily run into circular dependencies with regard to financing and negotiations.

How do you attract speakers without an audience, but also how do you sell tickets to build an audience without knowing who the speakers will be?

How can you choose a venue without knowing how many tickets you’ll sell, but also how can you know how many tickets you even can sell before you know the venue size?

How do you know what speakers you can get without knowing your budget to pay speakers, but also how can you know that budget without knowing how many tickets you’ll sell or how many sponsorships you’ll get?

How do you get sponsorhips without knowing speakers or audience size, but also how do you hire speakers without money from sponsorships?

How can you create an overall budget without knowing food costs, and how can you know food costs without knowing the audience size, and how can you know audience size without knowing venue size, and how can you know venue size without knowing the overall budget?

Sam cut through these issues like a hot knife through a hotdog.

Sam chose a relatively small maximum number of attendees (400), chose a venue just large enough to accomodate this number which required only a cheap deposit ($500), and spoke to potential speakers and sponsors as if all 400 tickets would sell.

Because Sam provided value to the speakers through the recruitment opportunity previously mentioned, he didn’t actually need to pay any of the speakers. That eliminated all the dependencies between budgeting and getting speakers. Sam did reach out to some prospective speakers who eventually said they would only speak for a fee, but he simply didn’t accept any speakers who required payment. This meant he turned down some famous people like James Altucher, but there are always more fish.

Sam spent a little under a month emailing potential speakers before launching the HustleCon website. By the time he launched and started advertising tickets for sale, he already had two speakers engaged. At that point, he advertised the conference with phrases like:

“…our amazing speakers for this year’s conference… these people are gonna blow your mind… I’m talking about guys like Rick Marini, who sold his business Tickle.com for $100+ million dollars. And Heitan Shah, who founded both KISSmetrics and Crazy Egg…two immensely successful startups.”

This type of marketing copy was effective at selling tickets even before most of the speakers were known.

Sales Strategy

Sam’s strategy for selling tickets was pretty straightforward: Emails and blog articles. Sam published one blog article about each speaker (he only wrote a couple himself and repurposed existing posts, with permission, from the speakers’ blogs for the rest). He then sent out a 12-email sequence to each person he was able to add to his mailing list. Each email in the sequence consisted of a short funny story about one of the speakers, a link to the article, and a call-to-action link to purchase tickets at the end of each email and article.

To get as many emails as possible, Sam used every tactic in the book. He shared each blog post in dozens of Facebook groups. He gave away 50 of the 400 tickets to Facebook friends who had the most Facebook followers in exchange for them sharing the HustleCon link as their status. He also harnessed the power of existing lists by messaging dozens of Meetup group organizers and bloggers who he knew had huge lists and offered them the opportunity to share a 35% discount with their subscribers. He took the same approach by contacting entrepreneur-focused companies with large newsletters such as StartupDigest, WebWallflower, and Fetch.

Sponsorship Strategy

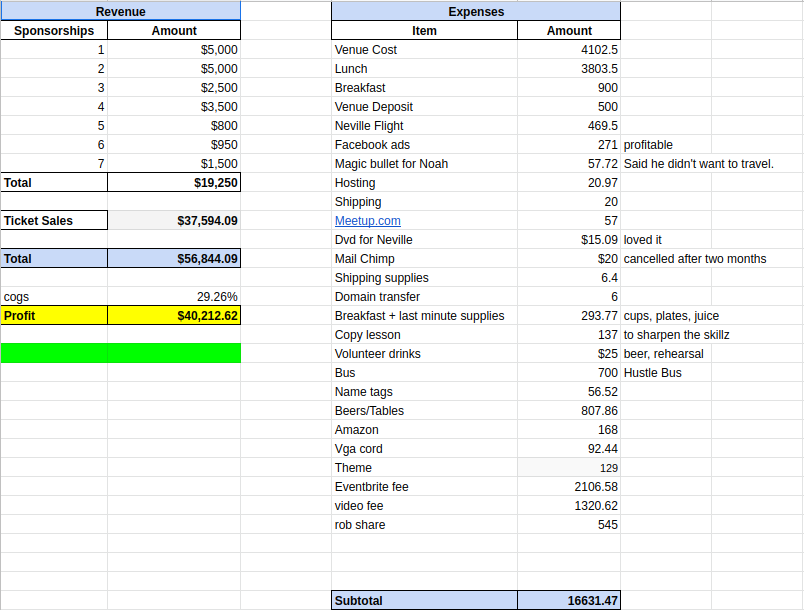

Sam raised about $19,250 from sponsors, although later when he had more experience he said he thought he undercharged and probably could have done around $50,000.

Sam classifies sponsors into 2 categories: those who want brand exposure and those who want leads.

Big companies like Google and Amazon have huge marketing budgets to spend on conferences. Those guys aren’t focused on getting a specific return on their investment but rather on building brand awareness.

Small companies like recruiting firms, startups, and local small businesses on the other hand are looking for a return on their investment.

Here’s Sam’s process for contacting potential sponsors:

Make a spreadsheet of 120 companies you like who have sponsored 2 or more conferences in the past. Record the head of marketing’s email address of each.

Email each company to set up a call.

During the call, don’t focus on actually trying to get sponsorship money but rather on getting them EXCITED about the conference. This led to many companies buying at least one ticket for an employee even if they didn’t decide to sponsor.

Through that process, Sam got about 20 calls with potential sponsors. Many of them sent at least one employee, and seven actually bought a sponsorship package.

Financial Breakdown

HustleCon brought in $37,594 in ticket sales and $19,250 in sponsorship package sales for a total of $56,844 in revenue.

Total expenses came in at $16,631 which left Sam with a hefty profit of $40,213. A detailed breakdown of expenses and sponsorship package amounts is shown in the spreadsheet below.

To achieve this, Sam spent about 2 months of 40-hour workweeks on this event plus one more month beforehand when he was just sending out emails to prospective speakers which is doable in under an hour a day. He also recruited 25 volunteers to work the event for free (this turns out to be much more common than you may expect in the event world). Volunteers are often motivated by free entry to the event and the potential “premium” access to speakers that backstage access to a focused business conference can provide. Sam recruited volunteers both through a HustleCon website sign up form and a Facebook post asking for help.

How You Can Use This Strategy

Sam demonstrated how you can put on a professional conference by working less than an hour a day on emails for one month plus working full time for 2 months. In the process, you can earn $40k in profit (or even $70k if you follow Sam’s later advice of charging 2.5x what he did for sponsorships).

Industry estimates are that anywhere from 10,000 to 1 million B2B conferences, conventions, and tradeshows are hosted in North America each year depending on what you use as the minimum event size. You can host a conference focused on an industry (dentistry, podcasting, whatever), a skill (e.g. negotiation or BRRRR investing), or anything else which a group of people will identify with or want to learn.

However, an ABSOLUTELY ESSENTIAL REQUIREMENT of Sam’s template is that the conference MUST be a BUSINESS OR FINANCE conference. Sure, lots of people make money through hosting conventions or tradeshows around hobbies, but that is a vastly more difficult and less profitable way to go.

Consider the example of the aquarium convention “Aquashella”. Saltwater aquariums are a relatively expensive hobby, so if any hobbies could be the basis of a profitable conference, aquariums should be on that list.

Aquashella was created by a long-time aquarium Youtuber with an existing audience of around a hundred thousand subscribers and his partner who worked for an aquarium company and had years of industry experience as a sponsor and vendor in aquarium conventions. Despite those advantages, it took those partners 8 months of work to put on a convention which appeared from the outside to be a success and yet in reality generated profits of slightly less than Sam’s small conference. Worse yet, those profits weren’t even real cash but just the value of the infrastructure assets (tanks, lights, inflatables, etc) needed to run the conference. It took them another 6 months of hard work to throw a second conference in another city just to get to $100k of total gain, and still a good portion of that was non-cash assets.

Which sounds more attractive: 28 man-months of total work with the stress of managing many thousands of attendees, dealing with fire marshals and city permits due to the large crowds, and moving lots of equipment from city to city all for maybe $80k of cash OR 2.5 man-months of total work with only a few hundred attendees for $40k cash?

The Moral? If you’re going to host a conference to make money, then be darn sure you choose a theme that is clearly business / finance focused so that you can charge ticket prices of at least $100 and deal with many fewer attendees and headaches.

And as a financial bonus which I haven’t even mentioned yet, you can also do what Sam did during the second HustleCon which is to launch a new product or promote an existing product you’re selling. Sam launched a general business daily newsletter which he eventually sold to HubSpot for many tens of millions of dollars.

This article is an example of one of my email letters so if you like this kind of material and want more, you can subscribe for free here 🙂

Investment Advisers Act: An Overview for Hedge Fund Startups

To avoid serious legal consequences, every hedge fund manager needs to know whether their fund management company qualifies as an investment adviser according to the Investment Advisers Act (IAA) or the rules thereunder.

If the hedge fund will only invest in commodities (including digital currency commodities such as Bitcoin) and/or other assets which are not securities, then the hedge fund manager is not an investment adviser and can ignore the Investment Advisers Act and most likely also the Investment Company Act (although they may still be subject to the Commodities Exchange Act and may need to register with the CFTC as a commodity pool operator and/or a commodity trading advisor).

However, if the fund will invest any of its capital into securities (including any digital currencies or assets which are deemed securities), then the fund manager will qualify as an investment adviser under the IAA. In that situation, the manager must legally operate in one of three roles: (1) an SEC registered investment adviser, (2) an SEC exempt reporting adviser, or (3) an exempt non-reporting investment adviser.

Three Categories of Investment Advisers

The first category (registered investment adviser or “RIA”) is the most difficult and expensive route. It requires credentials, a lot of paperwork and filings with the SEC, fees, strict record-keeping, audits, and compliance with various rules around how you can structure your fund management contracts, how you can advertise, etc. If you’re just getting into the hedge fund business, then you almost certainly can avoid this option and go for category (2) or (3) listed before. Consequently, this article will heavily focus on what it takes to qualify for and maintain compliance within those latter categories, and we will not go into much detail on the requirements for RIAs.

The second category (exempt reporting adviser or “ERA”) is somewhat deceptively named for those not already steeped in the jargon of securities law. As an exempt reporting adviser, you still need to make certain initial and periodic filings with the SEC and you need to create an account on the SEC’s IARD system. That sounds like “registration” to most English speakers, but for purposes of the Investment Advisers Act, it isn’t. The main differences between a registered investment adviser and an exempt reporting adviser are (1) once initial filings are submitted to IARD, they are automatically deemed accepted for an exempt reporting adviser whereas a registered investment adviser must wait for an “effective order”, (2) the initial and ongoing filing requirements for exempt reporting advisers are shorter and less regulated than those of RIAs, and (3) the IAA binds RIA’s to operate their business according to lots of specific rules which don’t all apply to exempt reporting advisers (more on this to come). It is important to note that ERAs must still comply with certain record-keeping requirements and that the SEC does have the authority to audit these records, although typically the SEC only does this for cause.

The third category (exempt non-reporting adviser) is usually the most desirable category for fund managers as it typically comes with the smallest compliance burden. These investment advisers must qualify for one of the exemptions listed in 80b-3(b) or 80b-3a(a) of Title 15 of the U.S. Code. We’ll cover exactly what those exemptions are later in the article.

Note: This article only covers the Investment Advisers Act and the SEC regulations promulgated thereunder. However, individual states often have their own laws for investment advisers which may or may not be preempted by the federal law of the Investment Advisers Act. Further complicating the situation is the fact that states may use slightly different definitions of “investment adviser”, so it’s important to know what the situation is for your state and any states you have investors in.

Also, it is important to remember that many terms have different definitions even in different parts of federal law (e.g. “security” has a very different meaning in the tax rules regarding wash sale trading than it does in the Investment Advisers Act). Any definitions provided in this article should only be interpreted as relevant to the Investment Advisers Act and no other section of law unless explicitly stated.

Finally, throughout this article, the term “person” means either an individual (often called a “natural person”) or a company.

Investment Adviser Registration & Exemptions

The first and most important determination for a fund manager to make under the IAA is whether or not they must register with the SEC as an investment adviser. Investment adviser registration is described in section 203 of the Act (codified as section 80b-3 of U.S.C. title 15), and the exemptions from registration are broken up across that section as well as section 203A.

The IAA essentially starts from the position that any investment adviser must register, and then the IAA works backwards by exempting various types of advisers from the registration requirement. The following is a list of types of investment advisers that are exempted from the need to register with the SEC (some exemptions are not listed since they are unlikely to apply to fund managers of any type):

(Per section (b)(1) of 80b-3) Any investment adviser, other than an investment adviser who acts as an investment adviser to any private fund, all of whose clients are residents of the state within which such investment adviser maintains his or her principal office and place of business, and who does not furnish advice or issue analyses or reports with respect to securities listed or admitted to unlisted trading privileges on any national securities exchange

(Per section (b)(2) of 80b-3) Any investment adviser whose only clients are insurance companies

(Per section (b)(6)(A) of 80b-3) Any investment adviser that is registered with the CFTC as a commodity trading advisor whose business does not consist primarily of acting as an investment adviser and that does not act as an investment adviser to (1) a registered investment company or (2) a company that has elected to be a business development company pursuant to section 80a-53 of the Investment Company Act and has not withdrawn its election

(Per section (b)(6)(B) of 80b-3) Any investment adviser that is registered with the CFTC as a commodity trading advisor and advises a private fund, provide that, if after July 21, 2010, the business of the advisor should become predominately the provision of securities-related advice, then such adviser shall register with the SEC

(Per section (l)(1) of 80b-3) “Exempt reporting advisers to VC funds”. Any investment adviser that acts as an investment adviser solely to 1 or more venture capital funds (as defined here).

(Per section (m)(1) of 80b-3) “Exempt reporting advisers to AUM-limited private funds”. Any investment adviser that only acts as investment adviser to private funds and that has assets under management in the United States of less than $150 million. However, investment advisers taking advantage of this exemption must still comply with the record-keeping and reporting requirements authorized by section (m)(2).

(Per section (a)(1) of 80b-3a) “Small advisers”. Any investment adviser that is regulated or required to be regulated as an investment adviser in the state in which it maintains its principal office and place of business, unless the investment adviser (A) has assets under management of at least $25 million, or such higher amount as the SEC by by rule deem appropriate, or (B) is an investment adviser to a registered investment company

(Per section (a)(2) of 80b-3a) “Mid-size investment advisers”. Any investment adviser that (1) is not an investment advisor to any registered investment company or company which has elected to be a business development company pursuant to section 54 of the Investment Company Act, (2) is required to be registered as an investment adviser with the securities commissioner (or any agency or office performing like functions) of the state in which it maintains its principal office and place of business, and that, if registered, would be subject to examination as an investment adviser by any such commissioner, agency, or office, and (3) has assets under management between $25 million (Or the higher number specified by the SEC in accordance with section (a)(1)) and $100 million (or such higher numer as the SEC may deem appropriate). However, if by effect of this paragraph, an investment adviser would be required to register with 15 or more states, then the adviser may register with the SEC under the Investment Advisers Act.

For U.S.-based private fund managers, the most useful exemptions are typically (1) The registered commodity trading advisor exemptions in 80b-3(b)(6)(A) and (B), (2) the capped private fund exemption in 80b-3(m)(1), (3) the state-regulated small advisor exemption in 80b-3a(a)(1), and (4) the state-registered mid-sized advisor exemption in 80b-3a(a)(2).

SEC Exempt Reporting Advisers

If you are a fund manager taking advantage of either the 203(l) (i.e. 80b-3(l)(1) for venture capital fund advisers) or 203(m) (i.e. 80b-3(m)(1) for private fund advisers with under $150 million in AUM) exemptions previously mentioned, then you must comply with the reporting requirements specified in 17 CFR 275.204-4. These types of investment advisers are known as “SEC Exempt Reporting Advisers” (ERAs) rather than “SEC Registered Investment Advisers” (RIAs).

ERA Reporting Requirements

Exempt reporting advisers must submit an abbreviated form ADV but are not required to prepare or deliver a brochure to clients. After the initial form has been submitted through the IARD system, exempt reporting advisers must update the form at least once a year within 90 days of the firm’s fiscal year end (and more frequently in certain circumstances based on material developments, in accordance with the form ADV instructions).

ERA Record-Keeping Requirements

The SEC is authorized to require exempt reporting advisers to maintain certain books and records. There is slight ambiguity as to what exactly those requirements are, but the conservative answer is that exempt reporting advisers should maintain all records described in rule 204-2.

Exempt Non-Reporting Advisers

If you operate your hedge fund in a way that you do qualify as an investment adviser under the IAA but you fall under one of the exemptions listed in 80b-3(b) or 80b-3a(a), then you are not required to either register or perform the reportings that ERAs have to do. You must still comply with the anti-fraud provisions of the IAA, but those requirements don’t impose the same type of burden that registration or reporting do. Additionally, you may or may not need to register and comply with various state-imposed record-keeping and reporting requirements, but those topics will not be covered in this article.

National De Minimis Standard

Having now covered the three categories of investment advisers under the IAA, I will turn to another issue which is that of federal preemption of state law. A priori, it is possible that an investment adviser may be regulated by different rules in every single state in which the adviser operates or has a client or even an investor to a private fund. That could impose an enormous compliance burden which would have the effect of stifling small businesses acting as investment advisers. The authors of the IAA thought of this, and they included in the IAA a provision, the “national de minimis standard”, to reduce the amount of multi-jurisdiction regulation that an investment adviser must comply with.

Essentially, the IAA provides a uniform standard for the amount of business that an investment adviser must be conducting in a state before that state is allowed to require registration of the investment adviser. The law (section 222(d) of the Act, or equivalently, 15 U.S.C. 80b-18a(d)) is as follows:

No law of any state or political subdivision thereof requiring the registration, licensing, or qualification as an investment adviser shall require an investment adviser to register with the securities commissioner of the state (or any agency or officer performing like functions) or to comply with such law (other than any provision thereof prohibiting fraudulent conduct) if the investment adviser satisfies the following two conditions:

The investment adviser does not have a place of business located within the state

During the preceding 12 month period, the investment adviser has had fewer than 6 clients who are residents of that state

Investment Adviser vs Investment Adviser Representative

One common confusion for people new to securities law is confusion as to what the difference is between an “investment adviser” and an “investment adviser representative” and whether an investment adviser is always a company or whether a person employed by an investment adviser company is also an investment adviser. I’ll do my best to answer those questions here.

Any organized group of persons (whether incorporated or not)

Any receiver, trustee in a case under title 11 (bankruptcy), or similar official

Any liquidating agent for any of the foregoing, in his capacity as such

However, in the realistic situation where you operate all investment adviser services through an official business entity (you should never do anything else for liability reasons), then the business entity is the investment adviser, and the individuals owning or working for the investment adviser are not. In that situation, the individuals controlling or working for the investment adviser may be classified as “investment adviser representatives” (IARs) though. As a rough rule of thumb, unless the employee of the investment adviser is doing secretarial or other work that has no influence on investment decisions, then the employee is an investment adviser representative for the investment adviser company. You can find a more precise definition of investment adviser representative in the glossary at the end of this article.

Normally, investment adviser representatives are individual humans. However, the legal definition (the same definition as in the glossary) of IAR leaves open the possibility of convoluted scenarios where you may have one company providing the investment advice on behalf of another controlling company, and in such scenarios, one company could be deemed an IAR of the other. As a startup hedge fund, you almost certainly won’t have such a scenario so you can consider your company that manages the fund as the investment adviser and the key employees of the company as the investment adviser representatives.

Investment adviser representatives of RIAs or ERAs may have to be listed on parts of the reports or registrations submitted to the SEC, but they will not themselves be required to register as individuals with the SEC. However, IARs of any investment adviser (including RIAs, ERAs, and exempt non-reporting advisers) may need to be licensed, registered, and/or regulated by state laws and regulations. Be sure to check the specific laws and regulations regarding investment advisers and their representatives in every state in which your business either has a client, investor, employee, or place of business.

Glossary: Key Investment Advisers Act Definitions

This next section is intended as a reference guide where you can find the definitions of various important terms mentioned in the Investment Advisers Act. Don’t feel you need to read the entire section at once.

What is a “client”?

For purposes of the Investment Advisers Act, a private fund is a single “client” of the fund manager acting as investment adviser, regardless of how many investors the fund has. This can be very useful to fund managers, and the Act specifically guarantees that the SEC cannot reinterpret this definition (see section (a) of 15 U.S.C. 80b-11).

For example, if a fund manager advises a single fund that has 85 investors, then that fund manager is an investment adviser with a single client for purposes of the Act.

NOTE: It’s useful to draw a comparison here to the Commodities Exchange Act since the two most common regulated classifications for a hedge fund manager are “investment adviser” as well as “commodity pool operator”. The definition of “client” under the IAA is critical to some of the SEC-registration & state-regulation exemptions available to investment advisers. Analogously, the Commodities Exchange Act uses the term “participant” to define somewhat similar registration exemptions for commodity pool operators, but do not be fooled. The exemptions are actually critically different with regard to hedge funds. As pointed out above, a fund with 85 investors would be a single “client” for IAA purposes and might qualify for many exemptions, but the same fund would have 85 “participants” for purposes of the Commodities Exchange Act, and as such, the fund manager would not qualify for certain commodity pool operator exemptions that cap out at 15 “participants”.

What is a “security”?

According to the Investment Advisers Act, “security” essentially means any type of stock, certificate of indebtedness, interest in a profit-sharing arrangement, investment contract, security future, fractional interest in oil, gas, or mineral rights, an option, straddle, or privilege on any security or group or index of securities or which relates to foreign currency and is entered into on a national securities exchange, any certificate of deposit of a security, any transferrable share, or any type of receipt, guaranty, warrant, or right to subscribe to or purchase any security, or any instrument commonly known as a “security”.

What is an “affiliated person”?

In both the Investment Company Act and Investment Advisers Act, a person Y is an “affiliated person” of another person X if any of the following are true:

Y directly or indirectly owns, controls, or holds with power to vote, 5% or more of the outstanding voting securities of X (or vice versa with the roles of X and Y reversed)

X is directly or indirectly controlling, controlled by, or under common control with Y (note: this is symmetric in X and Y)

Y is any officer, director, partner, copartner, or employee of X

X is an investment company, and Y is any investment adviser of X, OR Y is any member of an advisory board of X

X is an unincorporated investment company not having a board of directors, and Y is the depositor of X

For purposes of the definitions above, an “advisory board” means a board, whether elected or appointed, which is distinct from the board of directors or board of trustees, of an investment company, and which is composed solely of persons who do not serve such investment company in any other capacity, whether or not the functions of such board are such as to render its members “directors” within the definition of that term, which board has advisory functions as to investments but has no power to determine that any security or other investment shall be purchased or sold by the investment company.

What is an “affiliated company”?

A person Y is an affiliated company of a person X if Y is both (1) a company and (2) an affiliated person of X.

Persons associated with an investment adviser

Within the Investment Advisers Act, the term “person associated with an investment adviser” means any partner, officer, or director of such investment adviser (or any person performing similar functions), or any person directly or indirectly controlling or controlled by such investment adviser, including any employee of such investment adviser (except that for the purposes of 15 U.S.C. 80b-3–the section of the Investment Advisers Act regarding registration of investment advisers–other than subsection (f) thereof, persons associated with an investment adviser whose functions are clerical or ministerial shall not be included in the meaning of such term).

The SEC may by rules and regulations classify, for the purposes of any portion or portions of the Investment Advisers Act, persons, including employees controlled by an investment adviser.

any partner, director (or other person occupying a similar status or performing similar functions), or employee (including an independent contractor who performs investment advisory services on behalf) of an investment adviser, OR

any other person who provides investment advice on behalf of the investment adviser and is subject to the supervision and control of the investment adviser

What is an “investment adviser representative”?

According to this SEC rule, an “investment adviser representative” (IAR) of an investment adviser company is any of the company’s supervised persons who meets all four of the following criteria:

The supervised person does NOT only provide impersonal investment advice (impersonal investment advice consists of investment advisory services that do not purport to meet the objectives or needs of specific individuals or accounts)

The supervised person regularly solicits, meets with, or otherwise communicates with the company’s clients

The supervised person has more than five clients who are natural persons and not hight net worth individuals (where “high net worth individual” means an individual who is a “qualified client” under rule 205-3 of the IAA or a “qualified purchaser” as defined in section 2(a)(51)(A) of the Investment Company Act)

More than 10% of the supervised person’s clients are natural persons and not high net worth individuals

NOTE: If the investment advisor (i.e. the company) is registered with a state securities authority rather than the SEC, then the company may be subject to a different state definition of “investment adviser representative”. Investment adviser representatives of SEC-registered advisers may be required to register in each state in which they have a place of business

In general, the term “dealer” means any person engaged in the business of buying and selling securities (not including security-based swaps, other than security-based swaps with or for persons that are not eligible contract participants) for such person’s own account through a broker or otherwise.

However, the term excludes any person that buys or sells securities (with the same caveat as above for security-based swaps) for such person’s own account, either individually or in a fiduciary capacity, but does not do so as part of a regular business. Also excluded from the definition are banks engaged in certain banking activities.

The Investment Advisers Act uses the same definition but with two very important modifications: insurance companies and investment companies are excluded from the definition of “dealer“.

What is an “investment adviser”?

Investment adviser means any person who, for compensation, engages in the business of advising others, either directly or through publications or writings, as to the value of securities or as to the advisability of investing in, purchasing, or selling securities, or who, for compensation and as part of a regular business, issues or promulgates analyses or reports concerning securities. However, the following persons are explicitly excepted from the definition:

A bank or bank holding company which is not an investment company and which does not serve as an investment adviser to any registered investment company

Any lawyer, accountant, engineer, or teacher whose performance of the previously described investment advisory services is solely incidental to the practice of his/her profession

Any broker or dealerwhose performance of such services is soley incidental to the conduct of his business as a broker or dealer and who receives no special compensation therefor

The publisher of any bona fide newspaper, news magazine, or business or financial publication of general and regular circulation

Any person whose advice, analyses or reports relate to no securities other than securities which are direct obligations of or obligations guaranteed as to principal or interest by the United States, or securities issued or guaranteed by corporations in which the United States has a direct or indirect interest which shall have been designated by the Secretary of the Treasury, pursuant to section 3(a)(12) of the Securities Exchange Act of 1934, as exempted securities for the purposes of that Act

Any nationally recognized statistical rating organization, as that term is defined in section 3(a)(62) of the Securities Exchange Act of 1934, unless such organization engages in issuing recommendations as to purchasing, selling, or holding securities or in managing assets, consisting in whole or in part of securities, on behalf of others

Any family office, as defined by rule, regulation, or order of the SEC, in accordance with the purposes of the Investment Advisers Act of 1940 (the SEC has defined “family office” here)

Such other persons not within the intent of the IAA, as the SEC may designate by rules, regulations, or orders

What are “investment supervisory services”?

Investment supervisory services mean the giving of continuous advice as to the investment of funds on the basis of the individual needs of each client.

What is a “place of business”?

As the term is used in the Investment Advisers Act (which is NOT the same as everywhere else in law that the term is used), a “place of business” of an investment adviser is (1) an office at which the investment adviser regularly provides investment advisory services or solicits, meets with, or otherwise communicates with clients or (2) any other location that is held out to the general public as a location at which the investment adviser provides investment advisory services, solicits, meets with, or otherwise communicates with clients.

What is a “principal office and place of business”?

The term “principal office and place of business” of an investment adviser means the executive office of the investment adviser from which the officers, partners, or managers of the investment adviser direct, control, and coordinate the activities of the investment adviser.

What is a “private fund”?

A private fund is an issuer that would be an investment company, as defined in section 3 of the Investment Company Act of 1940 (15 U.S.C. 80a-3), but for section 3(c)(1) or 3(c)(7).

Section 3(c)(1) provides an exception from the definition of investment company for companies with 100 or fewer beneficial owners (or 250 persons for a qualifying venture capital fund) and which does not plan to make a public offering of securities. If “public offering” is interpreted in the same sense as in section 4(a)(2) of the Securities Act of 1933, then a fund that raises money from investors under rule 506(c) of the Securities Act would not be engaged in a public offering and therefore should still qualify as a private fund for purposes of the IAA. That may be important to a hedge fund that trades commodities in addition to securities because one of the commodity pool operator registration exemptions requires that pool participations be sold under rule 506(c).

Section 3(c)(7) provides an exception from the definition of investment companies for companies whose securities are only issued by qualified purchasers (there are some additional details). The most common types of qualified purchasers are (1) individuals or family-owned businesses or trusts with at least $5 million in investments or (2) any legal entity with at least $25 million in investments.

Disclaimer: This article does not constitute legal, accounting, or investment advice.

How to Authorize a Delaware Corporation in Florida

Florida in general (and southeast Florida in particular) is one of the fastest-growing startup hubs in the United States.

“New York South” a.k.a. West Palm Beach

For Florida founders wishing to build scalable businesses that may need to raise outside capital, Delaware incorporation is still the recommended first step, but after that, you’ll need to authorize your Delaware corporation to transact business in the state of Florida. This article takes you through exactly how to do that step by step.

Step 1. Ensure your Corporate Name is Compliant

Every state has specific naming rules for corporations, and the Delaware naming rules are slightly different than the Florida naming rules, although there is significant overlap in acceptable names. If your Delaware corporation has a name that already satisfies the Florida naming rules (e.g. if it is a normal name that ends with “Inc” or “Incorporated”) AND if your name is not already taken by another corporation in Florida (which you can find out by searching here), then you can skip to Step 2.

However, if your Delaware corporation has a name that does not satisfy the Florida naming rules (e.g. because of an incorrect or missing suffix or because a corporation already exists in Florida with a substantially similar name), then you must choose an alternative corporate name for use within the state of Florida (you can still use the existing name both outside of Florida and for Delaware legal purposes). Once you have decided what alternative name you’d like to use, proceed to the next step.

Step 2. Choose a Registered Agent

If you have an existing Delaware corporation, then you already have a registered agent in Delaware. However, in order to operate in Florida, you’ll need another one with a registered office in Florida. You can either choose to serve this role yourself (keep in mind this will load you personally with certain inescapable liabilities) or you can choose to hire a company to serve this role.

If you hire a company, be certain you are hiring a reputable company. In addition, realize that most online registered agent companies will try to upsell you on services such as “virtual mail service” without making it clear that even without that service, they are still required by law to handle your mail regarding lawsuits (which is, after all, the precise job definition of a registered agent).

Unfortunately, Florida has not updated its out-of-state authorization procedures in a long time, so there is no way to request authorization online. Instead, you have to mail in your application, and to complicate matters, the application must be signed by your registered agent. That leaves you with three options: (1) find a registered agent who is willing & capable of filling out the application correctly and filing it on your behalf (no cheap online registered agent service I’ve ever found can do that), (2) find a registered agent with real customer service who is willing to coordinate with you via email to sign the application and then return it to you to file yourself (CSC Global for example), or (3) hire a lawyer or other business with the necessary expertise to coordinate and handle the entire situation on your behalf.

Step 3. Order an Official Certificate of Good Standing

Order an official “certificate of good standing” from the Delaware Division of Corporations. Take note that a certificate of good standing is NOT the same as the corporate status available to order online. You can order the certificate of good standing either at the same time as you file for incorporation in Delaware or afterward. In either situation, you’ll complete the order by going to the Document Upload Service webpage. If you’re doing this after already incorporating, then choose the “certificate request” option. If you’re doing all of this on your own, then have the certificate mailed to your address.

Step 4. Fill out the Application

Complete this cover letter AND application form and then coordinate via email or otherwise with the Florida registered agent you hired to get the application signed by them. Print out the cover letter and application once complete, and sign yourself where indicated.

Step 5. Mail in the Application

Once you have received the official certificate of good standing from Delaware, you’re ready to actually mail in your application. Your submission should include each of the following:

The completed cover letter from step 4

The completed application from step 4, signed by both you and your registered agent

The official certificate of good standing you received from Delaware

A check or money order, payable to the “Florida Department of State”, for the amount of the registration fee (at the time of writing, that amount is $70)

Mail in your submission with all of the items just enumerated to the mailing address specified on the cover letter form from step 4.

Step 6. Maintain Compliance Going Forward

Once you receive a letter of acknowledgment from the Florida Department of State, you’ll be able to legally transact business in the state. Keep this letter of acknowledgment in your corporate records.

To maintain your business’s legal right to operate in the state, you’ll need to file an annual report just as all companies actually incorporated in Florida must do. The report must be filed electronically between January 1st and May 1st every year, starting the year AFTER your corporation was formed.

Additionally, to stay compliant with Florida law, you’ll need to file and pay both annual state corporate income taxes and quarterly estimated state corporate income taxes. You can find more information about that here.

If you are a beginner to OBS Studio and have a Blue Yeti microphone that you wish to use for audio input, then here are the audio filter settings I recommend you try. Start with these and then adjust as necessary to fit your specific recording environment and desired output.

Filter 1: Noise Supression

Add a “Noise Suppression” filter with “Method” set to “RNNoise (good quality, more CPU usage)”.

Filter 2: Noise Gate

Add a “Noise Gate” filter. Set the Close Threshold to -32 dB and the Open Threshold to -26 dB. Adjust those two as necessary based on the ambient noise level in your recording environment.

Set the Attack Time to 25 ms, the Hold Time to 200 ms, and the Release Time to 150 ms (these may already be the default settings for those three variables).

Filter 3: Compressor

Add a “Compressor” filter. Set the parameters for the filter as follows:

Ratio 6:1

Threshold -18 dB

Attack 6 ms

Release 60 ms

Output Gain 0.00 dB

Sidechain/Ducking Source None

Filter 4: Limiter

Add a “Limiter” filter with the following parameters: