SWIFT is a telecommunications network that only banks and certain financial institutions are allowed to join (it has over 11,000 members in over 200 countries). The SWIFT network & its messaging standards are maintained by a non-governmental legal entity (S.W.I.F.T. SC) — a cooperative co-owned by its member banks & institutions and organized under Belgian law. The cooperative sells products and services to its member financial institutions, mostly related to use of its proprietary “SWIFTNet” (the actual implementation of the SWIFT network) and Business Identifier Codes (BICs). You can read about the history of when and why the SWIFT coop was formed and what technology SWIFTNet replaced here.

How is S.W.I.F.T. SC Regulated?

Because SWIFTNet is only a messaging system used to describe what money transfers have happened or will happen rather than a system to actually implement those money transfers, the SWIFT cooperative is not regulated as a payments or bank company. However, due to SWIFTNet’s critical role in the global economy, the SWIFT coop is still subject to oversight (and therefore control) by several central banks. The National Bank of Belgium (NBB) acts as the lead overseer, supported by the G-10 central banks. In addition, the SWIFT Oversight Forum provides the central banks of many other countries an avenue to exert more limited control and influence over SWIFT.

What is a SWIFT Code (BIC)?

Every bank on the SWIFT network is identified with a BIC (standardized under ISO 9362) that is either 8 or 11 characters. The terms BIC, BIC code, and SWIFT code are all equivalent terms that mean exactly the same thing and can be used interchangeably.

BICs have a structure: the first 4 characters (only English letters from A-Z) identify the bank and are usually closely related to the bank’s name or an abbreviation of the bank’s name (e.g. the first 4 characters of Chase Bank’s BIC are “CHAS”).

The next 2 characters of a BIC (also only letters) are the country code, identifying which country the bank is located in (e.g. “US” for the U.S., “GB” for the UK, or “RU” for Russia). It’s interesting to note that banks which operate internationally actually operate as different entities in each country, so e.g. when sending money to an HSBC bank in the U.S., sender banks would use a different BIC than if they were sending money to an HSBC UK bank.

The next 2 characters of a BIC (letters or numbers form 0-9) are the city location code for the bank’s main head office.

Finally, a BIC may or may not have an additional 3 characters (letters or numbers) to identify a specific bank branch office to be used instead of just the national office of the bank.

Note: Sometimes people confuse IBAN (International Bank Account Number) with BIC, but the two are NOT the same thing. BICs identify banks whereas IBANs identify accounts at a bank. Additionally, people sometimes confuse BICs with ABA (American Banker Association) Routing Numbers, but the two are separate and distinct numbers. ABA Routing Numbers are used for U.S. domestic wire transfers, and BICs are used for international wire transfers.

How does SWIFT messaging work?

The purpose of a network is communication, and the purpose of the SWIFT network, in particular, is to enable communication about money and the movement of money. To accomplish this, SWIFTNet actually comprises four separate communication channels:

FIN (which enables the transmission of messages formatted according to the traditional SWIFT MT standards)

InterAct (which enables the transmission of messages formatted according to the newer XML-based SWIFT MX standards)

FileAct (which enables the secure, reliable transfer of files — it is mostly used to transfer large batches of messages such as bulk payment files, very large reports, or operational data)

Browse (which, together with the previously mentioned channels, enables SWIFTNet users to securely browse financial websites available on SWIFTNet using standard internet protocols & languages such as HTTP-S and HTML)

Let’s dive a bit deeper into how each of these channels actually works.

What is SWIFT FIN?

SWIFT FIN is a communication protocol that can be used by SWIFTNet users. Every FIN message must be formatted as one of the “MT” formats. These formats are similar (but not identical) to the formats codified in ISO 15022 part 1 and part 2. Unfortunately, there is no free access to these standards, and if you are developing a banking or fintech tool that uses SWIFT then you’ll likely need to purchase them. However, you can find a pretty substantial overview of MT messages here, and I’ll also provide a more concise summary below.

There are nine proper categories of MT messages, each with a finite number of message types, and there is an additional category of “system messages” which is often designated “category zero”. Each category corresponds to a particular subset of the financial services industry, as shown in the table below.

Category

Message Designations

Description

Number of message types

0

MT0xx

System messages

–

1

MT1xx

Customer payments and checks

19

2

MT2xx

Financial institution transfers

18

3

MT3xx

Treasury markets

27

4

MT4xx

Collection and cash letters

17

5

MT5xx

Securities markets

60

6

MT6xx

Treasury markets — metals & syndications

22

7

MT7xx

Documentary credits & guarantees

29

8

MT8xx

Traveller’s checks

11

9

MT9xx

Cash management and customer status

21

SWIFT MT message types & categories

You can find an enumeration of the specific types from each category on this unofficial page, however, the SWIFT coop makes changes from time to time to message formats so ensure you check the official paid SWIFT MT documentation if you plan to develop a fintech tool that interacts with SWIFT.

Each SWIFT MT message consists of the text literal “MT” followed by five blocks of data: three headers, message content, and a trailer.

MT103 is the SWIFT message type used by financial institutions to signal an international/cross-border wire transfer. Every MT103 has a number of data fields in its main message data block which are labeled with alphanumeric “tags”. Each field’s tag, together with a short description of what the data value represents, is provided in the table below (don’t expect to understand the meaning of each field name — just appreciate the parts you can understand for now).

Tag

Field Name

20

Transaction reference number (sender’s reference)

13C

Time indication

23B

Bank operation code

23E

Instruction code

26T

Transaction type code

32A

Value date / currency / interbank settled amount

33B

Currency / original instructed amount

36

Exchange rate

50A, F or K

Ordering customer (payer) or address of the remitter

51A

Sending institution

52A or D

Ordering institution

53A, B or D

Sender’s correspondent (bank)

54A, B or D

Receiver’s correspondent (bank)

55A, B or D

Third reimbursement institution (bank)

56A, C or D

Intermediary institution (bank)

57A, B, C or D

Account with institution (bank)

59 or 59A

Beneficiary customer 4×35

70

Remittance information

71A

Details of charges (OUR/SHA/BEN)

71F

Sender’s charges

71G

Receiver’s charges

72

Sender to receiver information

77B

Regulatory reporting

MT103 message fields (tags)

Not all fields are well-typed, but there are at least recommended best practices for the fields. For instance, tags 52-57 should preferrably have values which are ISO 9362 BICs, tags 50 and 59 should preferrably have values that are either BICs or account numbers, and account numbers are to be in either IBAN or BBAN format.

What is SWIFT InterAct?

The SWIFT FIN protocol together with its MT messages based around ISO 15022 are imperfect. SWIFT InterAct is a next-generation protocol that uses XML-based “MX” messages based around the ISO 20022 standard. InterAct & MX messages improve on FIN & MT messages in four ways: richer data can be transmitted & exchanged, increased robustness reduces the number of instances when manual intervention is needed, regulatory compliance is easier, and consistency amongst how the protocol is used by different institutions is designed to be higher with MX than MT messages.

MX is the future of SWIFT and it is expected that many participating banks will migrate largely or entirely to using MX messages during a protocol transition scheduled for November 2022.

SWIFT has provided an detailed PDF with equivalence tables for MT and MX messages. For full information, you’ll need a SWIFT website account to get access to the SWIFT knowledge center with complete official documentation.

What is SWIFT FileAct?

SWIFTNet FileAct is a protocol for transmitting bulk files in any combination of the various formats that banks may use for wire transfers, ACHs, or other protocols, without needing to go outside of SWIFTNet’s highly secure internet-based network. For example, you can read a short report about the various ways PNC bank uses FileAct in this document.

What is SWIFT Browse?

Browse is a bundle of products offered by the SWIFT coop to enable more general secure communication between SWIFT network members beyond the structured messages of FIN or InterAct. SWIFT Browse makes use of Alliance WebStation (a desktop app serving as an interface) and various other products to enable secure web-based browsing of websites enabled on SWIFTNet.

How to Use and Compute Dates & Times in Airtable Formulas

Airtable has many built-in functions to get the dates and times of different events as well as to compute durations, add durations to dates, compare dates and times, and more. This post contains two parts: the first part is a table that lists all of the important date & time functions that are built into Airtable, together with descriptions and instructions on how to use them, and the second part of this blog post is a series of answers to common questions about how to effectively work with dates and times in Airtable.

Function

Inputs & Outputs

Notes

NOW()

Inputs: None

Output: current datetime (e.g. “2/27/2022 5:17pm”)

TODAY()

Inputs: None

Output: current date (e.g. “2/27/2022”)

TODAY() is like NOW() except it doesn’t include time of day information

CREATED_TIME()

Inputs: None

Output: The datetime when the record containing the output cell was created

LAST_MODIFIED_TIME()

Inputs: None

Output: The datetime of the last user modification to a non-computed cell of that record

IS_AFTER( date_1, date_2)

Inputs (2): Can be dates and/or datetimes

Output: 1 if date_1 is after date_2, otherwise 0

If one input is a date and the other is a datetime, then the date will be interpreted as a datetime with time 12am

Example: If date_1 = “2/28/2022 10:15am” and date_2 = “2/28/2022”, then IS_AFTER(date_1, date_2) = 1

IS_BEFORE( date_1, date_2)

Inputs (2): Can be dates and/or datetimes

Output: 1 if date_1 is before date_2, otherwise 0

IS_SAME( date_1, date_2, “units”)

Inputs (2-3): – date_1 (may be a date or datetime) – date_2 (may be a date or datetime) – “units” is an optional third input that can be left out if desired; if included, it is a unit of time written as a string with quotes (e.g. “years”)

Output: 1 if date_1 is the same as date_2 (up to one “unit” of granularity, if “units” is included as an input); otherwise 0

Inputs (3): – date_1 (may be a date or datetime) – date_2 (may be a date or datetime) – “units” (one of the same options as above)

Output: a number (computed as the number of time “units” between date_1 and date_2)

TONOW( date ) or FROMNOW( date )

*The two functions are equivalent

Input (1): A date

Output: A duration of time written as a number plus a unit, representing the time between NOW() and the specified input date.

E.g. “20 hours” or “18 days” or “2 months”

DAY( date )

Input (1): A date or datetime

Output: A number from the range 1-31 representing the day of the month for the input date

MONTH( date )

Input (1): A date or datetime

Output: A number from the range 1-12 representing the month (1=January, 12=December)

YEAR( date )

Input (1): A date or datetime

Output: The four-digit year of the input date or datetime

HOUR( datetime )

Input (1): A datetime

Output: A number from the range 0-23 representing the hour of the specified datetime (0=12am, 23=11pm)

WEEKDAY( date )

Input (1): A date or datetime

Output: A number from the range 0-6 representing the day of the week (0=Sunday, 6=Saturday)

DATETIME_FORMAT( datetime, “format-specifier”)

Inputs (2): – a date or datetime – a character or string, with quotes, that represents a specified way to format a date or datetime (e.g. “M”, “d”, “ddd”, etc)

Output: A string of text that represents a date or datetime in the specified format

Example: DATETIME_FORMAT(“11/22/2022”, “M”) = 11

Example 2: DATETIME_FORMAT(“11/22/2022”, “D”) = 22

Example 3: DATETIME_FORMAT(“11/22/2022”, “Do”) = “22nd”

“dd” –> “Su”, “Mo”, etc (2-letter day of the week abbreviation)

“ddd” –> “Sun”, “Mon”, etc (3-letter day of the week abbreviation)

“dddd” –> “Sunday”, “Monday”, etc (full day of the week name)

“YY” –> last two digits of year (e.g. “89” or “02”)

“Z” –> timezone relative to GMT, including colons (e.g. “-07:00” or “+3:00”)

“ZZ” –> timezone relative to GMT, not including colons (e.g. “-0700” or “+0300”)

“X” –> Unix timestamp (in seconds)

“L” –> display date in format “MM/DD/YYYY”

“LL” –> display date in format “<month-name> day, YYYY” (e.g. “June 8, 2023”)

You can find a complete list of all format specifier codes here

Airtable Date & Time Functions

There are a few additional datetime functions available in Airtable that I have not included in the reference table above since they aren’t generally as useful. However, if you need to look them up, you can find them described on this page.

How can I compare two dates in Airtable?

The most useful functions for comparing two dates in an Airtable formula are the IS_AFTER, IS_BEFORE, and IS_SAME functions. You can find descriptions of how to use each of these functions in the reference table above.

How do you calculate a certain number of days after a known date in Airtable?

To find the date that is a certain number of days after a known date, use the DATEADD function which is built into Airtable. You can find a description for this function and how to use it in the reference table above.

How do you use Airtable datetime functions in Airtable Automations?

Unfortunately, you can’t use any of the built-in Airtable datetime functions directly within an Airtable Automation. However, you can usually find a work-around by creating extra computed fields which run the Airtable datetime functions you need and then referencing those fields from your Airtable Automation.

Videos & Maps from Inside Ukraine During 2022 Russian Attack

During the night of February 23-24 in American timezones (early morning of February 24 in Ukraine), Russia attacked Ukraine in multiple regions, including many areas outside the separatist regions in eastern Ukraine. The following videos show the perspective of people on the ground in Ukraine during these attacks.

Ivano-Frankivsk Missile Strike

Ivano-Frankivsk is a city located in western Ukraine, far from the separatist regions that Russia used as an excuse to invade.

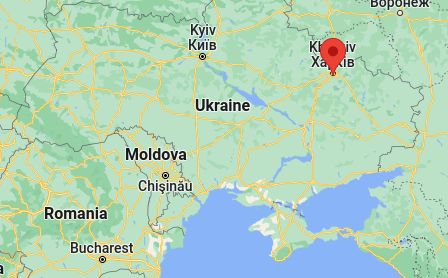

Minutes after President Vladimir Putin of Russia announced a military operation in eastern Ukraine, explosions were visible near the city of Kharkiv. By early Thursday morning, several Ukrainian cities were under attack.

Hundreds of people, including many women and children are currently taking shelter inside a subway station in Kharkiv, #Ukraine as explosions are heard in the city. @washingtonpostpic.twitter.com/ZddeHqlMvU

A limited partnership is the standard legal structure for an investment fund such as a venture capital fund, private equity fund, hedge fund, or real estate investment fund. In this article, I’ll go through the specifics of how to properly set up a limited partnership in the state of Florida. At the end of the article, I’ve also included a fee schedule for all filing & document fees related to limited partnerships as well as a list of definitions relevant to limited partnership law (so if you don’t understand what a particular term in this article means, check the definitions at the end).

Choose a Partnership Name

Florida is one of the subset of states which allows you to create a variation of a limited partnership called a limited liability limited partnership (LLLP). At first glance, the LLLP appears to be an attractive business entity since it provides liability protection to the general partner (GP) unlike a traditional limited partnership. However, unless you are operating entirely within the state of Florida (which is nearly impossible given that you’ll likely at least be interacting with a bank, broker, or other financial company that isn’t based in Florida even if all your investors are in Florida), then I’d strongly recommend sticking to just a conventional LP structure and using another business entity such as an LLC for the GP. The reason for this is that not every jurisdiction has an entity equivalent to an LLLP which opens you up to potentially unprecedented lawsuits (expensive!). If you do insist on entertaining the use of an LLLP, I’d definitely recommend hiring an experienced lawyer to help you make that final decision and set everything up correctly.

For a limited partnership (LP) that is not a limited liability limited partnership (LLLP), the name must contain one of the following phrases or abbreviations:

“limited partnership”

“limited”

“L.P.”

“Ltd.”

“LP”

In addition, the name must NOT contain any of the following phrases or abbreviations:

“limited liability limited partnership”

“L.L.L.P.”

“LLLP”

The name must also be sufficiently distinguishable from all partnership names already on file with the state. You can check if your desired name or one substantially similar to it is already on record using the Sunbiz business name search engine. For reference, the full name rules are laid out in florida statute 620.1108.

File a Certificate of Limited Partnership

A certificate of limited partnership must be filed with the state, together with the necessary fees (described below in the “Partnership Fees” section and including both the filing of the “original certificate of limited partnership” fee and the “designation of registered agent” fee). The certificate of limited partnership must include the following items.

Partnership Name

Specify a name for limited partnership (in accordance with the name principles previously described).

Initial Designated Office

Specify both the physical street address of the initial designated office of the partnership as well as a mailing address. The mailing address can be the same as the street address, different, or even a P.O. box.

Initial Registered Agent & Office

Specify the name and street address of the initial registered agent for the partnership. If this registered agent is an individual, then they must sign the application accompanying the filing of the certificate of limited partnership. If the registered agent is a business entity, then a principal (individual) of that entity must sign to accept the obligations of registered agent.

When filing online, the signature requirement is fulfilled by having the registered agent type their name in the relevant signature block.

General Partner Information

Specify the name and business address of each general partner (GP). There must be at least one GP. Each GP that is not an individual must be organized or registered with the Florida Department of State, must maintain an active status, and must not be dissolved, revoked, or withdrawn.

Each general partner (or a principal of any GP which is a business entity) must sign the document. When filing online, the signature requirement is fulfilled by having each GP type their name in a designated signature block.

Limited Liability Limited Partnership Status

If the partnership is to be a limited liability limited partnership, then that must be specified in the certificate of partnership (or the same result accomplished by checking the relevant box in the online application).

Optional Other Items

A certificate of limited partnership may also contain other provisions, but may not override any of the non-waivable provisions specified in subsection (2) of Florida statute 620.1110.

Create a Strongly-Worded Written Partnership Agreement

Essentially, a partnership agreement is to a limited partnership what bylaws are to a corporation. We also have the following order of priority in application: if the partnership agreement conflicts with the certificate of limited partnership, then the partnership agreement prevails as to partners and transferees (see definitions section) whereas the certificate of limited partnership prevails as to persons, other than partners and transferees, that reasonably rely on the filed record to their detriment. Unfortunately, what provisions are actually included in a partnership agreement is a bit more ambiguous than is the case for corporate bylaws, as I’ll explain.

As defined by Florida law, “Partnership agreement” means the partners’ agreement, whether oral, implied, in a record, or in any combination thereof, concerning the limited partnership. The term includes the agreement as amended or restated.

This incredibly broad definition opens up the general partner(s) to lots of potential issues where a limited partner may argue that a particular presentation or oral conversation over the phone implied something different than what was written in a partnership agreement. To prevent every word you speak needing to be couched in protective legal disclaimers, it would be prudent for GPs to create a written partnership agreement that contains strong “containment” language so as to specify that this written partnership agreement, together with the certificate of limited partnership (and any other initial documents such as a Private Placement Memorandum and/or Subscription Agreement), supersedes any and all prior written or oral communications or agreements, represents the totality of the partnership agreement, and shall not be modified by any future oral or written agreements unless such modifications are in writing, clearly labeled as “amendments to” or “modifications of” the partnership agreement, and signed by the GP(s).

When deciding on what substance to actually include in a partnership agreement, consider addressing the issues on the following checklist.

Checklist for Drafting Partnership Agreement

Partnership Governance & Management

What voting rights will the limited partners have?

What major actions can the general partner(s) take or not take without limited partner approval? How broad are the management powers of the GP(s) and are there any explicit limits different than the default powers and limits specified in Florida limited partnership law? (particularly relevant statutes: 620.1118 f.s. and 620.1406 f.s.)

Which amendments to the partnership agreement can be effected solely by the GP without consent of the LPs? How are other amendments to the partnership agreement (or other documents such as the Certificate of Limited Partnership) made? What notice and/or time requirements are imposed for such amendments?

If there is more than one GP, what actions require the consent of more than one? What is the consensus mechanism (e.g. unanimity, majority, etc)?

What are the specific duties of the GP?

Is the GP required to dedicate any particular amount of time to partnership matters?

Are there any restrictions on or explicit allowances for how the GP or its affiliates engage in activities outside the partnership?

Are there any restrictions on the GP’s right to form other partnerships?

What sort of liability protections, if any, will the GP be afforded both in general and/or for specific acts taken on behalf of the partnership? Under what circumstances would the GP be liable to the partners for acts or omissions?

Under what conditions can the GP withdraw as GP?

Under what conditions and/or process will the GP cease to be GP (either by removal, incapacity, etc)?

What happens to the GP’s interest in the partnership when it ceases to be GP? Does that depend on how the GP came to cease being GP (e.g. removal, resignation, death, etc)?

Under what conditions can the partnership be dissolved? When is the dissolution definite vs when is there a choice? What happens in the case of a technical dissolution (e.g. due to failure to submit annual report in a timely fashion)?

What power of attorney is granted to the general partner?

Is there an arbitration clause governing disputes among the partners?

Are there any conditions under which limited partners would be personally liable beyond their capital contributions? (A default answer is provided in 620.1303 f.s., but that can be overriden by choice in the partnership agreement if desired.)

Where/how will meetings be held? How will meetings be called and what sort of notice is required? What quorum is necessary for meetings to be held or actions to be taken? Can any actions be taken by written consent of the partners without a meeting? Are any meetings mandated?

Records & Reports

What books & records must be maintained by the partnership?

What access rights will the limited partners have to such books & records? (note: you cannot reduce or remove the rights afforded by Florida statute 620.1304)

What reports will the limited partners be guaranteed to receive? (e.g. annual statement of partner positions, etc)

How will taxes be handled? How and when will tax information be made available to the limited partners?

What are the initial capital contributions of each general partner and each limited partner?

Will partners be allowed to make additional capital contributions later if desired?

Will general or limited partners be required to make additional capital contributions if necessary? If so, what constitutes “necessary”?

What happens if a partner fails to make a required capital contribution? (e.g. perhaps a percentage penalty is imposed on the existing capital account of that partner)

Are limited partners brought on all at once or can additional limited partners be brought in after the partnership has begun operations? If new partners can be brought on, are there any limitations on how many or how often they can be brought in? Is approval of the general partner(s) sufficient to admit a new limited partner to the partnership or is limited partner approval also required?

Are partners allowed to withdraw their capital contributions? If so, what notice, time, and other conditions are required for such withdrawals to be allowed?

Is a partner entitled to interest on his or her capital contribution?

Does any partner have priority on distributions over any other partners?

How are distributions to be divided among the partners if such distributions are not in strict accordance with capital contributions?

How are tax allocations made?

Will the GP(s) be required to make up any deficits in capital accounts? If so, under what conditions would such requirement apply?

What is the timeline for distributions? Is it fixed or variable? If variable, what variables does it depend upon? Are there lock-ups during which distributions cannot be made? Do limited partners have the option to withdraw funds during this time anyway in exchange for a percentage penalty?

Will there be guaranteed distributions sufficient at least to cover taxes allocated to each partner?

How are distributions made in the event of partnership liquidation?

Profit & Loss Allocations

What fees are paid to the general partner?

What profit & loss of the partnership are allocated to the general partner? How is such incentive compensation or carried interest structured?

Are the fees and allocations dependent upon financial performance of the partnership and/or upon financial performance of some external benchmark such as a stock, commodity, or real estate index?

What reimbursements is the GP entitled to?

Assignment of Interests

Does a GP have the right to assign its interest in distributions?

Does an LP have the right to assign its interest in distributions?

Under what conditions is assignment restricted or prohibited?

What rights (in terms of partnership governance, future distributions, etc) does an assignee of a general or limited partner’s interest have?

What are the procedures for any such assignments?

What happens on the death, incompetency, bankruptcy, or divorce of a limited partner?

Note: Subscription information is often packaged into a “Subscription Agreement” that is labeled separately from the “Partnership Agreement”, but as I shared earlier, the Florida law definition of “partnership agreement” would encompass both contracts as well as any other legally binding documents between the partners. Hence, the choice to label a “subscription agreement” as something separate from a “partnership agreement” is purely one of preference.

Maintain the Limited Partnership in Good-Standing

To keep the limited partnership in good legal standing, you must file an annual report with the Florida Department of State between January 1 and May 1 of the year following the calendar year in which the limited partnership was formed (or in which a foreign limited partnership was authorized to transact business in Florida), and every year thereafter during the same time window.

Additionally, you must keep records for all “required information” (as defined in the definitions section at the end of this article).

Partnership Fees

Fee

Amount

Type

supplemental corporate fee

$88.75

Due annually for both domestic and foreign authorized limited partnerships. Submitted with the filing of the annual report under section 620.1210

Filing an annual report

$411.25

Due annually

Filing an original certificate of limited partnership

$965

One-time fee, due at formation

Filing an original application for registration as a foreign limited partnership

$965

One-time, due upon application (for foreign LPs only)

Filing a certificate designating a registered agent

$35

One-time, due at formation (or upon application for authorization for a foreign LP)

Filing a certificate of change of registered agent or registered office address

$35

Event-based (upon filing a certificate of the change)

Filing a certificate of amendment or restatement of the certificate of limited partnership

$52.50

Event-based

Requesting a certified copy

$52.50 for the first 15 pages,

plus

$1 per additional page

Event-based (for each certified copy request)

Requesting a certificate of status

$8.75

Event-based (for each certificate of status requested)

Filing a certificate of conversion

$52.50

Event-based

Filing a certificate of merger

$52.50 for each party to the merger

Event-based

Filing for reinstatement

$500 for each year or portion thereof that the limited partnership was administratively dissolved

“Act” means the Florida Revised Uniform Limited Partnership Act of 2005, as amended.

“Limited partnership” includes the possibility of a “limited liability limited partnership” but not a “foreign limited liability partnership” which is an entity not organized under the laws of the state of Florida.

“Certificate of limited partnership” means the certificate required by section 620.1201. The term includes the certificate as amended or restated.

“Partnership agreement” means the partners’ agreement, whether oral, implied, in a record, or in any combination thereof, concerning the limited partnership. The term includes the agreement as amended or restated.

“Designated office” means the office that the limited partnership is required to designate and maintain under section 620.1114 (which need not be a place of its activity in Florida) OR, with respect to a foreign limited partnership, its principal office.

“Principal office” means the office at which the principal executive office of a limited partnership or foreign limited partnership is located, whether or not the office is located in this state. (Yeah, that definition seems a bit circular to me too.)

“Registered office” means the address of the registered agent meeting the requirements of section 620.1114. The registered agent must be either an individual residing in Florida or a company authorized to do business in Florida.

“Distribution” means a transfer of money or other property from a limited partnership to a partner in the partner’s capacity as partner or to a transferee on account of a transferable interest owned by the transferee.

“Transfer” includes an assignment, conveyance, deed, bill of sale, lease, mortgage, security interest, encumbrance, gift, or transfer by operation of law.

“Transferee” means a person to which all or part of a transferable interest has been transferred, whether or not the transferor is a partner.

“Transferable interest” means a partner’s right to receive distributions.

“Sign” means to: (a) execute or adopt a tangible symbol with the present intent to authenticate a record; or (b) attach or logically associate an electronic symbol, sound, or process to or with a record with the present intent to authenticate the record.

“Required information” means the information that a limited partnership is required to maintain under section 620.1111. More explicitly, it is the following information:

A current list showing the full name and last known street and mailing address of each partner, separately identifying the general partners, in alphabetical order, and the limited partners, in alphabetical order.

A copy of the initial certificate of limited partnership and all amendments to and restatements of the certificate, together with signed copies of any powers of attorney under which any certificate, amendment, or restatment has been signed.

A copy of any filed certificate of conversion or merger, together with the plan of conversion or plan of merger approved by the partners.

A copy of the limited partnership’s federal, state, and local income tax returns and reports, if any, for the 3 most recent years.

A copy of any partnership agreement made in a record and any amendment made in a record to any partnership agreement.

A copy of the financial statement of the limited partnership for the 3 most recent years.

A copy of the three most recent annual reports delivered by the limited partnership to the Department of State pursuant to section 620.1210.

A copy of any record made by the limited partnership during the past 3 years of any consent given by or vote taken of any partner pursuant to this act or the partnership agreement.

Unless contained in a partnership agreement made in a record, a record stating: (a) the amount of cash and a description and statement of the agreed value of the other benefits contributed and agreed to be contributed by each partner; (b) the times at which, or events on the happening of which, any additional contributions agreed to be made by each partner are made; (c) for any person that is both a general partner and a limited partner, a specification of transferable interest the person owns in each capacity; and (d) any events upon the happening of which the limited partnership is to be dissolved and its activities wound up.

Q&A

Question: Why does Florida code chapter 620 have TWO partnership acts? Which one applies to my limited partnership?

Answer: Florida chapter 620 has two parts: (I) the “Florida Revised Uniform Limited Partnership Act of 2005” (FRULPA) and (II) the “Revised Uniform Partnership Act” (RUPA). RUPA applies to general partnerships. FRULPA alone applies to limited partnerships (LPs) and limited liability limited partnerships (LLLPs).

You can read more about the history and intended context of these two acts here.

Question: What is the difference between the certificate of limited partnership and the partnership agreement?

Answer: The certificate of limited partnership is a specific document that must be filed with the state government of Florida in order for a limited partnership to have legal status as a business entity. The partnership agreement of a limited partnership is an abstract agreement that is the composite of all written and oral, express and implied agreements among the partners, including any amendments or restatements of such agreements.

Disclaimer

Nothing in this article constitutes legal advice. Make your own decisions and consult a lawyer if necessary or advantageous.

Axiom Daily keeps you up-to-date on crypto & web 3 in just 4 minutes each day.

Lightcoin gets a privacy upgrade

After two years of development, Litecoin has finally released its “Mimblewimble” (MW) upgrade which gives Litecoin users not only the opportunity to chuckle but also the power to opt into using certain privacy features. MW provides several technologies including the ability to make any particular transaction “confidential” (which hides the amount of the transaction) as well as “CoinJoin” (a “coin mixer” that obfuscates the recipient of a transaction). On the one hand, confidentiality of these types is available in the traditional financial system and is desirable in the cryptocurrency space to protect the private information of individuals. On the other, cryptographic confidentiality doesn’t have the backdoor that traditional banking confidentiality does for government regulators, and that is likely to incur the wrath of regulators if adoption is high enough. One certainty is that banks and money services businesses regulated under the Bank Secrecy Act will incur higher compliance risks if they choose to interact with Litecoin after the MW upgrade goes into full effect. Full story.

Gambling company Entain partners with Theta blockchain

Entain, one of the 100 largest companies listed on the London Stock Exchange (LSE: ENT), operates in the gambling industry both online and with physical partnerships around the world. Entain recently launched “Ennovate”, an innovation project to invest in and develop new interactive & VR gambling experiences. As part of this project, Ennovate has partnered with Verizon, BT, and Theta Labs (the company behind the Theta blockchain). Ennovate’s first collaboration with Theta Labs is to develop a white-labelled NFT platform for customers of partypoker, built atop the Theta blockchain. Full story.

Coinbase lists Solana-based project tokens for the first time

Coinbase announced that users would now be able to transfer Solana-based ORCA and FIDA tokens into Coinbase and Coinbase Pro accounts. Once sufficient liquidity is available, trading of certain pairs with fiat and stablecoin currencies will be enabled in phases. ORCA and FIDA are the governance tokens for the Orca and Bonafida decentralized exchanges, respectively. These two tokens are the first tokens from Solana-originating projects to be listed on Coinbase.

Chainlink releases tutorial on creating weather-dependent NFTs

Chainlink released a tutorial on how to create dynamic NFTs that depend on external data such as weather data. If you can work fast and launch a series of NFTs that sweat on hot days and shiver on cold days on OpenSea by tomorrow night, you can probably make some quick bucks.

USDC launches on Flow blockchain

Circle is launching support for their USDC stablecoin on the Flow blockchain. Flow is most well-known as the blockchain that hosts the NFT collections “NBA Top Shots”, “NFL All Day”, and “Matrix World”, although it has ambitions to play a much larger role in scalable metaverse applications. With USDC having already launched natively on Ethereum, Algorand, Solana, Stellar, Tron, Hedera, and Avalanche, Flow will be the eighth blockchain to be so honored. Full story.

ConsenSys acquires MyCrypto to enhance MetaMask

ConsenSys, the company behind MetaMask, has acquired MyCrypto with the intention of integrating MyCrypto with MetaMask. MyCrypto provides a dashboard to manage all your Ethereum accounts in one place as well as tools to interact with and deploy contracts and manage ENS domains. It’s easy to see how MetaMask would benefit from these capabilities, especially with Solana’s Phantom wallet having just raised $109 million and vocalizing ambitions of expanding to Ethereum.

Axiom Daily: How does crypto affect children & more

Keeping you up-to-date on crypto & web3 in just 4 minutes each day with Axiom Daily.

UNICEF considers how crypto might affect children

UNICEF (the United Nations Children’s Fund) is a UN agency tasked with providing humanitarian aid to children worldwide and recently put out a report entitled “Prospects for children in 2022“. In part of the report, the agency enumerates three possible positive effects of crypto on children: (1) greater financial inclusion which would increase the livelihood of families and therefore children, (2) more frictionless remittances, and (3) more instant, transparent, and efficient social assistance programs. Additionally, the agency enumerates three possible negative consequences of crypto: (1) financial instability, (2) facilitation of transactions for child trafficking, sexual exploitation, and child pornography, and (3) defrauding of children.

Altogether, the crypto section of the report reads with a bit of a negative bias, with very little elaboration of benefits and more emotionally charged language in the discussion of risks. Additionally, the report provides no data to estimate relative magnitudes of the different effects and no discussion of how the greater transparency of most blockchain transactions often empowers law enforcement to trace criminals such as child traffickers more easily than the existing financial system does.

Solana wallet Phantom raises $109 million at $1.2 billion valuation

Phantom is the most popular crypto wallet for use on the Solana blockchain. Founded less than a year ago in March 2021, the company’s product gained 70,000 users by July when it raised $9 million in a Series A round. This month (January 2022), the company raised over 10 times that amount: $109 million at a $1.2 billion valuation in a Series B round led by Paradigm and with participation from a16z, Solana Ventures, and other big-name VCs. Full story.

FTX raises $400 million at $32 billion valuation

Just a few days ago, it was announced that FTX US raised a $400 million Series A at an $8 billion, and today it was announced that its international sister company FTX raised $400 million in a Series C round at a valuation of $32 billion. For reference, the company NASDAQ has a market cap of only $29.7 billion, and the Intercontinental Exchange (the parent company of the NYSE and other exchanges both in and outside of the U.S.) has a market cap of $70.8 billion.

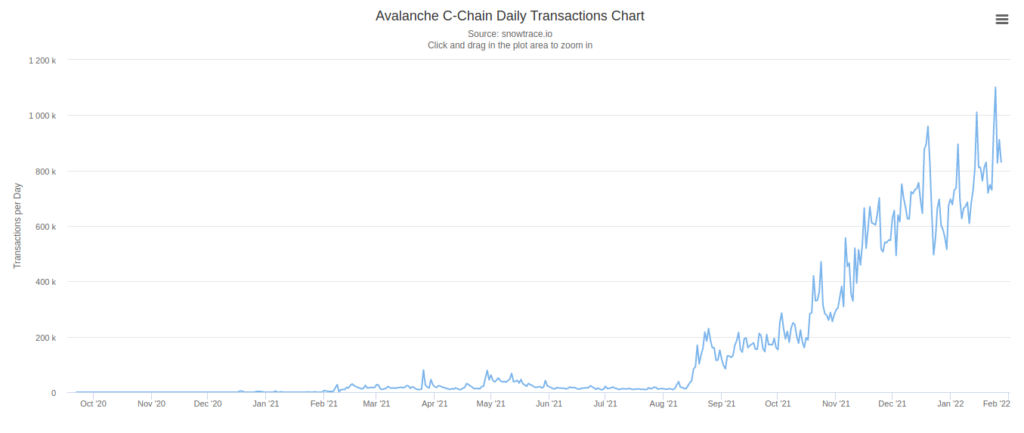

BTC, ETH, AVAX, and just about every other cryptocurrency has seen a major price dip during the last few months. AVAX, the native cryptocurrency of the Avalanche blockchain, fell from an all-time high of over $146 on November 21 of last year down to around $55 earlier this month. However, despite the 62% price drop, Avalanche smart contract transactions have continued to grow at a relatively unaffected pace.