How much money should a search fund raise in 2023 for a traditional 2-year search? And how should that money be budgeted? In this article, I report the answers to those questions from over 20 search fund operators and investors. Here’s what they had to say:

$400k is the bare minimum

“Back in 2018 it was 300-400k for a solo searcher. [$500-600k] seem high. The key is building confidence and using templates in expensive processes like legal and diligence to reduce dead deal costs. I wouldn’t spend much on CRM and search tools — you can do most of that yourself or have tools given to you from investors.”

Reagan

“I have recently started to budget my search and am running into $430k as a minimum. This does include savings on rent and generally a low cost of living. I think [$500k] is a fair [number].”

Mohammad

Inflation has raised the average above $500k

“Inflation does push up [the raise amount] a little bit. I would say $550k is a fair number for 2 years search. I budgeted 1/3 of the cost to Legal and DD, 1/4 of the cost to search tools and brokers… It really depends on the industry [though].”

Raymond

Budget at least 1/3 of money raised for legal, due diligence, tools, and brokers

“For [legal, diligence, search tools, and brokers], I would allocate $100K for due diligence and $50K for search tools, and brokers. We could easily say this category forms at least 1/3 of the total expense among other planned/ unplanned events.”

Virbahu

Create a budget

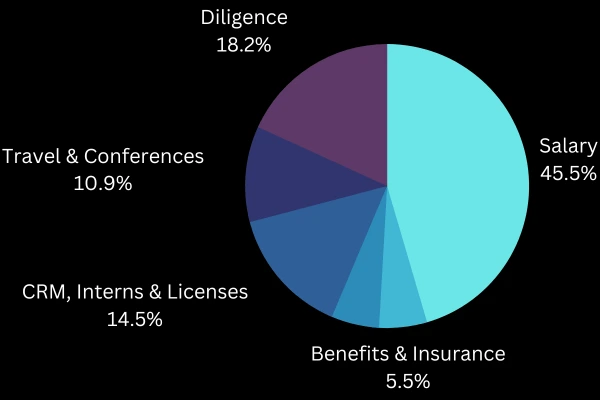

One searcher named Bhushan provided his detailed 2-year, $600k ($300k/year) budget for his search fund:

Category

Year 1

Year 2

Total

Total (%)

Salary

$150k

$150k

$300k

50%

Benefits & Insurance

$15k

$15k

$30k

5%

Legal

$15k

$15k

$30k

5%

CRM, interns, and licenses

$50k

$30k

$80k

13%

Travel & conferences

$30k

$30k

$60k

10%

Diligence

$40k

$60k

$100k

17%

Total Budget

$300k

$300k

$600k

100%

“Bhushan’s calculation is a safe bet, excluding the cost of acquisition. But in most cases such luxury may not be possible and you can probably manage with about $400k by being very careful on where you spend and with your reduced compensation.”

Damodar

“I will likely be around the $550-$575K range, but may have lower travel expenses than most as I will have slight bias to the east coast. Not exactly the same breakdown as Bhushan but close enough that I would point you to [his numbers].”

Ferdinand Chan

Budget accuracy is better than budget precision

“Your goal should be to be accurate, not overly precise. You can raise up to $600K without encountering significant pushbacks. Raising more funds doesn’t necessarily mean you need it, but in my experience, it’s more correlated with the opportunity costs of another job. Compensation: Aim for a salary around the latest Stanford study average: $120,000. “The range of annual salaries during the search phase was $30,000 to $200,000, with a median of $120,000 (and mean of $116,508) and no bonus.” – Stanford 2020 Search Study

Tech Stack- Here is what you will need:

Systematic Data Tools: Grata (~$1000 per month, seek discounts).

CRM & Marketing Automation: Streak (Free for one user), consider alternatives like Reply.io, HubSpot, Outreach.io.

Website Domain: Google sites (~$7 per month).

VoIP Phone: RingCentral (~$50 per month).

Deal Aggregation: Axial (Free, with a success fee based on Lehman formula if the deal closes).

Incorporation Fees: Allocate around $20K to $30K.

Accounting QoE: You need to budget $24k, $8K for broken deals and $12K to $18K if the deal closes. You will budget for 3 broken deals. (Shop around before you choose who you work with)

Legal Fees: Budget zero, most search fund lawyers roll their fees forward. (Less room to shop around).

Travel Expenses: Can vary, considering flights, hotels, dining, and entertainment as needed for your specific activity.”

Michael Tabet

Build the budget based on need, not on the max that will get approved by your investors

“I would recommend building the budget you need, not the budget you think will get approval. For established traditional search fund investors, my $500k budget has been perceived as being on the tighter side. I live in a cheaper city, have a second household income and assets, so the modest salary is not a problem for me. I have spent a lot of time before my search preparing, so feel confident that I can manage within the constraints I have set. The main risk for my budget will be the travel budget with flights looking like they will stay inflated for at least 12 more months. There may be additional paid tools for proprietary search that I may pass over, but over the past six months with a bit of experimentation I have now developed a system for building lists from scratch with free and cheaper tools that works well for me.”

Ben Page

“I agree with those saying to determine raise amount based on budget. Salary, set up costs, travel, diligence, intern costs – year 1 then year 2. Search capital is expensive capital so you don’t want to raise more than you need.”

Alexander Wallace

“$500k was standard in 2022 and is more than adequate. If you run out of capital towards the end but have a solid deal under LOI, I’m sure your investors would assist you in a smaller re-raise to get you to close.”

Doug

Graduating from a good school helps you raise more

“I know what a bunch of people from Kellogg budgeted this year and the range was $500-$600k skewed a little bit toward the high end of that range.”

Brett

Mid-career search fund operators get paid more than fresh MBA grads

“I just closed in June – it was $670k all-in. My salary was higher than average because I’m mid-career and live in the bay area. Investors want the salary to feel tight but not be a source of severe stress. For the costs you asked about:

Legal – I only budgeted $5k. My law firm charges $5k up front and all legal costs are rolled into the transaction (including any broken deal costs)

Diligence – mostly QoE (which, unlike legal, must be paid immediately if there’s a broken deal). I budgeted $30k / year.

Search Tools – I budgeted $30k / year for “search infrastructure” (software, paid interns)

Brokers – I didn’t budget for this – would be paid for in the deal costs”

Chris

How much should a European search fund raise?

“[In Europe] it is above EUR 650k. Roughly the distribution works as follows 40% salary, 20% DD, 40% other expenses…”

Michael

“My opinion, at least for Europe is that at least 600k€ are needed for 2 years search.”

Valerio

How much should a Brazilian search fund raise?

“In Brazil it might be lower than US, I have seen a range of 420k – 460k for a solo searcher.”

Everton

The $1 Billion Question: Did AT&T Poison People with Underwater Lead Cables?

Decades ago, AT&T buried thousand of miles of lead-lined cables across the U.S., and a Wall Street Journal investigation recently found thousands of those cables still under the soil and water tables of very populated areas.

The Journal’s investigation found that 80% of sediment samples taken next to underwater cables showed elevated levels of lead, with the lead levels highest directly under or next to the cables and dropping off within a few feet — a sign that the lead was coming from the cables.

The investigation also found examples of aerial cables, coated in lead, with lead flaking off into the sediment below.

However, assigning blame is difficult.

The company named AT&T today is a different company that the company named AT&T which laid the cables decades ago. Between then and now, the original AT&T was broken up into 8 different companies as part of an anti-monopoly lawsuit. Some of those companies later merged and rebranded into Verizon. Others ended up merging with internet companies, or dying. And one eventually bought the old AT&T trademark and rebranded as AT&T.

As companies split, merged, split again, and merged again over the decades, many cables were abandoned, and records were lost.

Several telecom companies have denied ownership of problematic cables, making it difficult for investigators or potential class action plaintiffs to track down who exactly they should be going after.

On top of that, it’s an open question of whether or not the lead contamination from the cables was actually high enough to significantly affect anyone.

Isotopic analysis showed with high confidence that the lead in at least some of the contaminated areas was coming from the cables, but we don’t yet have any medical or other data to show a causal link to actual health problems, which means telecom companies likely won’t be forced to pay anything for at least a decade, if ever.

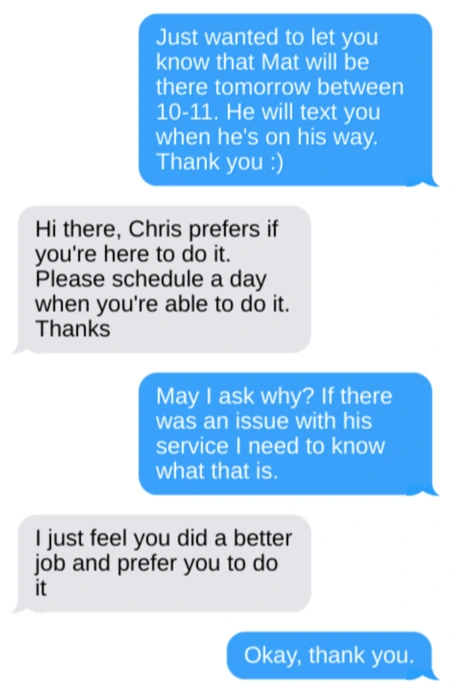

I hired my first employee, but my client wants me personally. What do I do?

Fred, 58 years old, runs a pest control company. A few months ago, he hired his first employee, Mat. Mat had no previous pest control experience, so Fred spent two months training him before letting him service clients on his own.

“I’ve had many compliments from clients about [Mat]… Since I hired him, I’ve been able to answer calls as they come in, go do estimates in person and grow the business. I wasn’t able to do that before. Also, I’m about to make my second hire, someone with lots of experience…[But then I received the messages in the screenshot above]… I understand that I probably did do a better job, but that’s a very high standard. Did [Mat] do a bad job, or just not as good as me? I don’t want to lose the client, but I also don’t want them dictating how I run my business. It’s a $95 bi-monthly residential [job, which is underpriced] because they’ve been a client for a couple of years, big property. Is it just growing pains? Should I just let them go?”

Fred

Here’s what advice other pest control business owners had for Fred:

1. Don’t let clients choose which employee services them

“At some point you’ll have to make you doing it not an option. Some customers may not go with it, but your customer base will change as the business does.”

Braiden

“I’ve encountered this. Sometimes you have to trim the edges of the plant in order for it to grow properly. If they absolutely won’t do your service unless you’re on the property, you may consider replacing their account.”

Brandon

“This happens to me a lot since last year I stopped doing regular visits. People will ask for me. My first question is “Did (employee name) do something wrong”? The answer is always no, the employee didn’t do anything wrong. Then I explain to the customer that the coolest part of being a business owner is that you’re able to hire hard-working people and create a team to solve complex problems. I then tell the customer that I am part of that team still, but I have taken on a new role. 9/10 customers will stay on board after that explanation. The ones that stop service you didn’t want anyway.

The important thing to remember is this never ends. We only have two full-time technicians. I we have a few customers that only want my most experience technician. Customers will complain that they prefer employee number one or employee number two. I give them the same response. We’re all part of the same team and we all can solve complex problems.”

Jeff

“Yep, growing pains, every person that grows gets this and when you hire your next guy some of your customers will ask that only your first hire do there service. Congratulation on the growth!! There are some great suggestions already made. Best of luck as for move forward.”

Caleb

2. Use a phone survey to check if your tech has picked up a bad habit

Mate, this happens to every pest business as they grow…

There are a couple potential things that may have happened, and how you deal with this will vary accordingly.

Every single employee I have ever hired, no matter how much training I have personally given them; when they are on their own, their personality, their mannerisms, their personal comfortability around certain tasks come into play and they develop their own habits and ways of doing things… And I do mean every employee.

All it takes is one customer asking him to do something that you do not do on your regular service and your employee wanting to impress thinks – I can do that – so they do it and the customer is over the moon – and your employee gets a dopamine rush with their appreciation and so when they go to the next job… guess what… they do it there too and before you even know it’s happening they are doing something that you never wanted or taught them to do. That’s all it takes.

Don’t just assume your customer can pinpoint exactly what they didn’t like about the service. If they feel more comfortable with you – there is a reason and you just have to work it out. Don’t ever assume your employee hasn’t picked up a bad habit.

Maybe it was a once off issue – Maybe your employee was stressed or had a fight with his girlfriend or was running late or maybe he nearly got in an accident on the way to the job and when the customer answered the door – he wasn’t smiling. Maybe he didn’t engage or ask the questions this one time, and that is what made them feel less comfortable with him compared to you.

Maybe the employee got a phone call and someone doing work for your customer whilst on their phone is a pet peeve of theirs.

Or maybe they feel entitled and believe they deserve you as the business owner only… that’s a whole other issue.

Here is what I would do…

Phone the client and say this …

“Hi _____. How are you today?

I would like to ask for your permission to help me, would you be willing to help me?

Great, I am just doing a follow up and would like to run through a few things with you…

When ____ arrived did he park the vehicle in a convenient location that was of no inconvenience for you?

When he arrived did he introduce himself with a smile?

Did he explain what he was there to do and confirm with you about your specific issues and needs?

Did he then do the job in a professional manner?

Did he leave the site as he found it, closing any gate that was closed upon arrival, ensure that the tap was turned off?

Did he advise you that he was done with the job?

Did he remain professional at all times?

Did he drive away in a courteous manner?

(Word all questions in the positive)

If they answered yes to all questions – pause for several seconds – and come back with… I’m confused, why were you unsatisfied with my new manager? (Lift up your employee to a high status)

You might just get the real answer.

If they answered “no” to any of your questions – say this:

“Thank you so much for bringing this to my attention. You have helped me to know exactly what to work on in our training and I appreciate that so very much and I promise you that next time he will certainly not do that again.

Can I ask one last favour – would you please contact me next time and let me know how he did? You are such a valuable customer and your sacrifice of time and insight is helping our company to grow and provide the very best of service, and I really appreciate that. Now with inflation our prices are going up, but because you are now one of my advisory clients that’s helping to perfect our business I’m going to keep you at the same discounted rate”

Another tip – always refer to your staff as the manager… never a “new employee” or “trainee”…

They are a manager of their own jobs after all.

This builds credibility as well.

On a final note / it is so awesome when you do an audit ride along with a staff member after awhile and just observe and a customer assumes that you are the trainee – best internal giggle ever!

Danny

3. If one client voices dissatisfaction, other clients may be silently dissatisfied

They’re telling you the issue. “You did a better job”. Call them and ask for specifics on where your tech fell short in their eyes. Thank them for the feedback as your goal is to train your team to replace you (or better).

If one customer is having a subpar experience, others might be as well. Now.. if they are requesting you because you’re their favorite. They’ll need to get over that. Jeff Bezos doesn’t deliver my Amazon packages and Bill Gates doesn’t install my Windows updates.

John

So one client out of how many asked for you personally? Do you make follow up calls or site checks to verify his work? I believe in the trust but verify method. I would call or meet with the client and ask how your technician isn’t doing the same level service in their eyes.

Tom

4. Help forge a new trusted relationship between the client and the new tech

“My husband explains to them that he hand picks and hand trains each one of our employees and trusts their service. And that he is not available for standard services on a regular basis, but would be happy to come out as he can. We’ve lost a couple people over the years but nothing I’m too worried about.”

Jerika

Sometimes it takes a “formal handoff” where you go with your new hire to the concerned client’s house and walk them through how well he is doing the job. It builds confidence. I’ve had to do this with my home inspection company when I got out of the field. One or two supervisory ride alongs (without any tools) was sufficient for the clients to be comfortable with the new hire. Be sure to elaborate any experience, and let the new hire talk! He needs to be able to communicate and build confidence that he knows what he’s doing, or he won’t be successful.

Philippe

Go and do the service with your tech, even if just a couple times, to help the customer feel more comfortable moving forward.

Ryan

In my opinion this is most likely a relational issue.

One way I’ve had success overcoming this is to send out new tech letters or emails introducing the new person. This speeds up the process and starts the connection process.

Also, going with the tech a few times often helps (sounds like you probably did that)… the tech letter was a game-changer for us…

In many cases, the customer isn’t buying pest control, they are buying relationship that does a pest control service. If you understand this, then all you have to do is provide a platform for the relational transfer and the process becomes much simpler.

Alger

5. Have your customers sign longer term service contracts in advance of hiring new techs

If you’re not going to run the route anymore, tell them that. Ask them what he needs to do better to keep them happy and send him back out.

I’d also recommend (if you haven’t already) to get your customers to sign a contract or service agreement with an early cancellation penalty next time you plan on switching/adding techs. That way they are locked in regardless who comes.

I told my customers that I no longer have a truck as I’m transitioning from technician to manager. I lost maybe 5 customers total.

Eddie

What Percentage of Assets do Companies Hold as Cash?

I sampled a variety of companies to get an idea of how much cash typical businesses hold on their balance sheets. The data is in the table below.

Company

Industry

Cash & Cash Equivalents as % of FY2022 Assets

Apple

Tech

17.5%

Coca Cola

Consumer Goods

10.3%

IBM

Tech

4.4%

Crocs

Consumer Goods

4.3%

Alphabet

Tech

6.0%

Acorda Therapeutics

Biotech

9.5%

Optical Cable Corporation

Manufacturing

0.5%

MIND Technology

Tech

12.2%

Intrusion

Tech

32.5%

BlackLine

Tech

10.3%

Five Below

Retail

10.0%

Shake Shack

Restaurant

15.4%

Kronos Worldwide

Chemical Production

32.3%

Carlisle Companies

Manufacturing Conglomerate

5.5%

Installed Building Products

Installation Contractor

12.9%

This is important data to know if you want to create an opportunity zone business (because opportunity zone businesses need to comply with the 5% rule).

If you want to attract higher value clients, you’ll want to go after a niche where businesses are commonly missing out on important opportunities (or are commonly incurring significant extra costs) due to bad bookkeeping. You can then provide the solution. Look for businesses that are operationally complex and/or have high gross margins (ideally both). Here are some examples:

1. Doctors’ offices (Healthcare)

Medical billing and reimbursement is complex. Billing and bookkeeping are complex interconnected requirements for doctors. Insurance claims, insurance reimbursements, different rates for insurance and cash patients, and healthcare billing regulations and debt collection all come into play.

Additionally, doctors earn a lot per hour so it’s not worth it for them to spend their time doing the books.

2. General contractors (Construction)

General contractors require subcontractor management, contract management, cash flow management (since construction projects often have long, staged payment cycles with financing from multiple sources and some payments depending on performance), and project cost estimating.

3. Foundation, structure, and building exterior contractors (Construction)

These types of contractors typically have over 2 month lags between when they bill for services and when they actually receive the money they are owed (the average age of accounts receivables for these companies is 67.5 days). That means cash flow, revenue recognition, and appropriate AR management are all more important here than for an “average” business.

4. Nonprofits

Nonprofits have a lot to lose (their tax exempt status) if they don’t keep good books. They also must track restricted funds, donations, and grants, and sometimes must produce financial statements for donors and regulators. They have to carefully avoid or track unrelated business income (UBI), and pay unrelated business income tax on any UBI they generate.

5. Car rental companies

A company that is renting at least 10 cars has a lot of depreciation as well as ongoing repair and maintenance costs. They also have operational and marketing costs. And they have a lot of cash flow. That is a good recipe to be a profitable bookkeeping client.

6. Heavy equipment rental companies

Like car rental companies, heavy equipment (e.g. cranes, bulldozers, etc) rental companies are operationally complex with a lot of ongoing depreciation, repairs, and maintenance.

What are the different types of bookkeeping?

Bookkeeping and accounting mean different things to different businesses. In general, there are several types of accounting tasks that may or may not be included in your bookkeeping services:

Categorizing transactions (from bank accounts and credit card accounts) using the labels from a chart of accounts. This is traditionally what “bookkeeping” meant.

Handling accounts receivable.

Zippia lists the median salary for AR clerks at $36,425/year ($17.52/hour). Zippia estimates the “typical range” at $29-45k / year.

Salary.com lists the average AR position (not just clerk) salary at $76,347/year.

Indeed lists the average base pay for AR clerks at $20.55 / hour.

Handling accounts payable.

Zippia lists the median salary for AP clerks at $38,333/year ($18.43/hour). Zippia estimates the “typical range” at $30-48k / year.

Salary.com lists the average AP position (not just clerk) salary at $77,726/year.

Indeed lists the average base pay for AP clerks at $20.37 / hour.

Managing payroll.

Paying & filing sales taxes.

Filing local, state, and federal income taxes.

Providing monthly or quarterly reports (P&L statement, cash flow statement, balance sheet, and possibly industry or business-specific KPI tracking)

Accounts Receivable

An accounts receivable (AR) clerk or specialist is responsible for making sure that customers pay their bills to the company, and that those transactions are recorded. Tasks included in these jobs are:

Generating invoices and sending them to clients/customers.

Following up with any clients/customers with unpaid invoices.

Maintaining and updating accounts receivable records to ensure aging (how long each client’s payment has been due), credits, and collections are applied and uncollectible amounts are accounted for.

Reconciling bank (and cash) accounts with AR accounts.

Preparing financial reports with AR KPIs so that the company’s management can gain insight into how collection efforts are going.

(For contractors): Preparing, issuing, and removing liens against the properties of customers who refuse to pay.

Hiring collection agencies or selling uncollected AR accounts when they go unpaid for a long time.

Accounts Payable

An accounts payable (AP) clerk or specialist is responsible for making sure that all valid bills are paid and that no invalid (or inaccurate) bills are paid. The various tasks often included under the umbrella of AP work include:

Verifying that invoices from vendors and suppliers are legitimate and accurate.

Is the invoice missing the invoice number? If so, you may need to ask the vendor/supplier to add the number.

If your business uses purchase orders, then you’ll want to match an invoice to a purchase order to verify that it’s legitimate and accurate (i.e. for the same dollar amount) before paying it.

Your business may have some other approval process that you need to go through before paying an invoice.

Communicating with vendors and suppliers to correct any inaccurate invoices.

Saving invoices (or a scanned copy of invoices in the case of paper invoices delivered by conventional mail) to an accounting system or computer storage system.

Coding invoices into your business’s accounting system (i.e. select the general ledger account, department, entity, location, etc).

Making payments on verified or approved invoices. This may be by sending a wire from your business’s bank website OR it may be via Bill.com or Tipalti or Coupa or from within your business’s ERP system such as NetSuite.

Near each month end, you’ll need to reconcile accounts

Cash account reconciliation: ending balance in books and records = ending balance from bank statement. This ensures that all cash disbursements during the month have been accounted for in the books and records.

Reconcile AP balance on the balance sheet to the AP balance on the Aging Schedule (a table of all a company’s accounts payables, ordered by their due dates)

An accounts payable clerk may be able to process anywhere from 30-120 invoices per day (excluding end of month days spent on reconciliation) depending on the skill of the clerk, the complexity and uniformity of the invoices, the percentage of invoices with errors, the business’s approval process for paying invoices, and the amount of automation that the company uses in the AP process. 32-45 per day is most typical. 120 invoices per day is absurdly high and is only possible for a company with highly uniform invoices that all come in through a standardized & heavily automated software system.

As a rule of thumb, if you run an outsourced AP service, you should charge at least enough for you to hire 1 full-time employee (whether that is a domestic or overseas employee) for each 500 invoices to be processed each month.

How much should I charge for bookkeeping services?

A quick search around various job boards shows that part-time bookkeepers in South Florida are being hired for $20-40 per hour. Full-time bookkeeper jobs often include more tasks such as payroll, accounts receivable, accounts payable, and sometimes additional tasks as well. These jobs typically carry salaries in the range of $40-50k per year (but can be up to $100k for some specialist roles at some companies).

Below is a table which shows the rates of various outsourced bookkeeping services.

– Free Quickbooks or Xero software included – Quickbooks Certified ProAdvisor Elite team (with overseas support most likely) – Monthly or weekly bookkeeping – Cash and accrual accounting – Login access for your CPA – Categorize all transactions (import bank statements; reconcile bank & credit card) – Monthly income / P&L statement – Monthly balance sheet * Easily manage your bill pay and payroll (how?)

Essential: – Monthly books – Monthly P&L and balance sheet – 1099 reporting – Year end financial report for your tax team – 30% discount on Gusto payroll – 30% discount on Stripe payments

Premium: – Everything in Essential plan – Annual state and federal income tax filings – Unlimited 1-1 income tax advisory services

*Add $100/mo if you want segment-level bookkeeping

– Monthly bookkeeping – Certified QuickBooks ProAdvisors and Xero-Certified Advisors – Accounting software included – Assigned a dedicated bookkeeper (probably overseas) and meet monthly with a lead accountant with a 4-year accounting degree

Core Service: – Weekly vendor payments (accounts payable) – Sales tax filings – Bookkeeping & reconciliations for up to 2 bank accounts, 2 credit cards, and one cloud-based POS system – Payroll system integration – Monthly P&L statement and balance sheet – Monthly inventory adjustment – 1 hour phone support each month – Unlimited email support

Pro Service: – Everything in Core, plus – Weekly “Flash Reports” (what are those?) – Customized period reporting – 2 hour phone support – Payroll processing (but you still pay for the payroll system’s fees) – A/R (up to 20 invoices/mo)

Premium: – Everything in pro, plus: – 4 hours phone support each month – Up to 3 connected bank accounts and 3 connected credit card accounts – A/R (up to 50 invoices/mo) – Weekly inventory adjustment – Customized reporting

Americans spend roughly $10 billion on payday loan fees each year because it takes banks 2-5 business days to actually deposit paycheck money into your account after you earn it. That’s changing in less than 3 weeks though because the Federal Reserve is launching their new 24/7/365 payment service, FedNow, before the end of the month.

FedNow has been called a blockchain, a government version of CashApp, and a central bank digital currency (CBDC). In reality, it’s none of those things.

What FedNow actually is is an instant payment network for banks to send money to other banks, 24/7, even on weekends and Christmas. Unlike a public blockchain like Bitcoin, FedNow is neither decentralized nor available to the general public. Only banks and credit unions which already have master accounts at the Fed can directly use the FedNow network.

Despite the deceptive photoshopped images published by many media outlets (see the example below), there is no government app that consumers can use to send payments over the FedNow network. Instead, each bank that wants to make FedNow available to their customers has to modify their own app or website to provide an interface for their customers to the FedNow network. That means FedNow instant payments will only be available to customers at certain banks in the beginning, but more banks will gradually join the network over time as part of FedNow’s phased roll-out strategy.

(Example of a photoshopped image by Forbes which has mislead many members of the public to believe that there will be a consumer-facing FedNow app.)

Faster payments help people, especially poor people, but some consumer advocates have raised concerns about how FedNow handles these payments. For starters, FedNow transactions are routed through the Fed which means the government can see the details of every payment that anyone sends on FedNow, not just payment amounts over $600 as will be the case for Venmo starting next year.

Additionally, some people are concerned that since FedNow is operated by the Fed, the Fed could abuse its power over the network to block transactions on political grounds. For example, the Fed could in theory refuse to process FedNow payments to certain political protesters or to firearm stores.

Currently, Fed officials claim the Fed will not censor any transactions, but Fed governor Lael Brainard also said that after phase 1 of the network’s roll-out, the Fed may start censoring transactions suspected of being fraudulent.

Several years ago, Facebook admitted to incorrectly censoring Trump supporters who were misflagged as Russian bots, so it’s not unreasonable to worry that automated Fed censoring of financial transactions may end up harming certain political groups. It’s also not unreasonable to assume that the Fed may provide some of this information to the IRS to help them target Americans suspected of under reporting their income. FedNow transactions even include metadata related to tax.

Instant payments in general also increase the risk of bank runs like we saw at Silicon Valley Bank earlier this year, and the risk of payment scams like we already have on CashApp and Zelle.

FedNow also poses an existential risk to some businesses, including payday loan companies and crypto companies.

One of the primary selling points of cryptocurrencies is that they enable nearly instantaneous 24/7/365 payments. If you can now accomplish the same thing directly from a U.S. bank account you already have, then what’s the benefit of paying via cryptocurrency? In fact, many cryptocurrencies are slower than FedNow.

FedNow transactions take a maximum of 20 seconds to complete, with a typical transaction only taking 2-5 seconds. In contrast, a Dogecoin transaction takes 2-5 minutes to finalize, and a Bitcoin transaction takes about an hour to finalize.

However, three crypto companies are embracing the FedNow roll-out as an opportunity to be a service provider to banks in a brand new market:

If the name “Nuvei” sounds somewhat familiar, it’s probably because Ryan Reynolds recently invested in and became a spokesperson for the company.

Nuvei is actually not a crypto-native company though. It’s just a regular payments company that happens to provide a way for businesses to pay in cash and pay out in crypto, or vice versa, and it allows traditional payments to also occur via FedNow.

Fluency and Tassat on the other hand both offer private blockchain platforms for banks to build upon.

Sadly, but not surprisingly, there are no Ethereum or other public blockchain based companies that are currently connecting to FedNow. However, one thing that does bring FedNow and many crypto companies together is a tendency to create expensive animated web pages for questionable projects:

How many tax dollars did it take to create this animated menu page for the Fed?🤦♂️💵🔥 pic.twitter.com/O3WSQydaOJ

A quick comparison of existing payment methods in the U.S.

Payment Method

Transaction Limits

Typical Transaction Cost to User

Typical Time

Availability

Wire Transfer

None (or bank specific)

$20

1 Hour

Monday to Friday, 9am to 4pm

Available at all banks

ACH

$10,000 or less per tx for consumer accounts

$25,000 or less per day for consumer accounts

*Chase offers the highest limits for consumers

Free for consumers

Free or <$1 for businesses

2 Business Days

Monday to Friday

RTP

$1 million per tx

Not directly available to end users

4.5 cents per tx for banks

Seconds

24/7/365

Available at ~300 financial institutions

Zelle

*Uses RTP, ACH, batching, and virtual transfers on the back end

$5,000 or less per day

Free

3 Minutes

10am to 10pm, 7 days a week, excluding certain holidays

*Not available for users of every bank

FedNOW

$500,000 per tx

Not directly available to end users

4.5 cents per tx for banks

<20 seconds

24/7/365

What IS FedNow, from an engineering perspective?

FedNow is a new software protocol operated by the Federal Reserve and made available to banks and other financial institutions. The purpose of FedNow is to allow banks to instantly (within 20 seconds) send payments back and forth.

In nerdier terms, FedNow is a messaging protocol where certain messages have the side effect of changing the values of participating master accounts at the Federal Reserve.

Will FedNow replace stablecoins?

FedNow provides instant payments that are as fast or faster than most stablecoins, are backed by FDIC-insured deposits, and are fully regulated and compliant with U.S. laws. In that sense, FedNow replaces one of the biggest use cases for stablecoins. However, FedNow does not directly interact with any blockchain which means it does not provide a solution for fiat-to-crypto trading via decentralized exchanges (DEX’s).

How does FedNow prevent fraud?

Faster payments enable faster fraud. If you send money to a scammer via a blockchain, via Zelle, or via FedNow, you have very little time to discover your mistake before the payment becomes irreversible. To combat the increased risk of fraud created by the introduction of FedNow, FedNow has built-in features to help banks limit their fraud risk. Those features are summarized in the table below.

Feature

Description

Network-level transaction limit

The maximum amount per transaction that a financial institution can send over the FedNow network.

This limit is set by the Federal Reserve.

Participant-level transaction limit

Participants (i.e. banks and credit unions on the FedNow network) can set a lower transaction limit for credit transfers they initiate based on their organization’s risk policies.

Why would they want to do that? Are sending orgs responsible for fraud?

Participant-defined blacklists

Financial institutions can specify a list of suspicious accounts that their organization cannot send to or receive from.

What is ISO 20022?

ISO 20022 is a messaging standard for financial institutions developed by the Geneva-based International Organization for Standardization (ISO) in 2004. The ISO 20022 standard is used in various aspects of finance, including:

Payments

Securities

Trade services

Cards

Foreign exchange

Here is an example of the ISO 20022 message flow for a consumer credit transfer via FedNow:

What features differentiate different payment networks?

Does the network support request-for-payment-initiated payments or only payer-initiated payments?

Does the network support computational rules to compute whether or not a payment should take place based on the state of the network?

Example: Each day, check if Bob’s account is below $100. If so, check if Alice’s account is above $500. If so, send $100 from Alice to Bob.

How much does it cost to be a participant of the network?

Example: Creating and owning a Bitcoin wallet is free, but there is a monthly membership fee for financial institutions to be a member of FedNOW.

What is the cost per transaction? Is the cost charged for transaction submission, transaction settlement, or both?

Is the network directly available to end users (e.g. Bitcoin) or is it only available to financial institutions (e.g. FedNOW)?

How long does it take for a payment to reach finality?

*Finality means that the funds transferred officially become the legal property of the receiving party.

**All other things being equal, a faster payment network will reduce false claims fraud perpetrated by payers, whereas it will increase fraudulent charges fraud perpetrated by payees.

***Finality is correlated with the time it takes for money to show up in a payee’s account, but the two events are not actually the same. True finality is mostly a concern for financial institutions concerned with counterparty risk. Most consumers are satisfied when money hits their account and aren’t concerned with whether or not the money is actually theirs or is simply being credited to them a day early by their bank.

Who is responsible for operating the network and finalizing transactions? There are several reasons why this is important:

If a single company or small group of companies is responsible for operating the network, they could commit fraud, be hacked, or lose data in a power outage.

If a government agency operates the network, then the government may have access to a lot of sensitive information that could be abused for political purposes, such as spying on the financial activities of a political adversary (unless the network has strong cryptographic privacy protections in place).

What types of cryptographic, legal, contractual, and/or company policy based privacy protections are there for users of the network? Who can see (and under what conditions) the information about who sent money to who and what that money was for?

*If a payment network has no privacy features preventing a government entity (such as the Fed) from seeing all details about all transactions, then it is easier for the government to abuse any control it may have over transactions (e.g. by blocking payments to a group of political protesters).

What information is (mandatorily or optionally) sent with each payment?

Example: If a payment network supports request-for-payment-initiated transactions, then it is valuable to businesses (from a bookkeeping perspective) to have such transactions accompanied by text or other data which identifies what the payment was for. That’s so that the business has proof to show the IRS in the event they are audited. However, if the same payment network also makes all transaction directly to a government entity such as the Fed, then there is a concern that such additional data could be abused to selectively control how people can spend their data (e.g. by disallowing people to spend more than $100 per month on gasoline as a way to accelerate transition towards a green economy).

Can network participants choose whether to only receive payments, only send payments, or both?

Can network participants blacklist certain payment senders, recipients, or transaction types to limit its own risk (e.g. fraud risk, counterparty risk, or sanction risk)?

Example 1: My bank won’t accept any payments from Bob because Bob is suspected to be a terrorist, and I don’t want my bank to be fined for helping to fund terrorism.

Example 2: My bank won’t send any payments over $100,000 to limit our risk of being defrauded by scam businesses.

Example 3: Don’t accept more than 3 request-for-payment-initiated transactions from the same requester in any 2-hour period.

What type(s) of value can be transferred over the payment network?

Example 1: Federal Reserve master account dollars

Example 2: Bitcoins

Example 3: Title to a real estate property

What’s the difference between RTP and FedNow?

RTP is a real-time payment network operated by a consortium of large U.S. banks via The Clearing House organization. RTP was launched in November 2017 and is currently used on the backend of some consumer services like Zelle.

FedNow is also a real-time payment network, but it is operated by the Fed rather than by private banks. FedNow is set to launch before the end of this month (July 2023).

What is FedLine?

FedLine is essentially a computer system that banks use in order to complete bank-to-bank wire transfers and FedNow payments.

What is Fedwire?

Fedwire is the protocol (accessed via FedLine) that banks use to complete domestic wire transfers. As of 2023, the fee charged by the Fed for a bank to transfer funds via Fedwire ranges from 3.6 cents to 92 cents per transaction.