“That’s a pretty interesting result to anyone running a hedged long/short investment portfolio, especially with energy prices so high. It also means that if I personally held any private stock in Crypto.com, I’d be looking to offload it as quickly as possible since its stadium deal structure didn’t meet our “high-quality deal criteria”.

In January 2021, the fintech company “Q2 Holdings, Inc.” agreed to pay an estimated $26 million to name a Texas major league soccer stadium “Q2 Stadium”. That was just the beginning of what became a record-setting year for stadium name deals. Some of the largest deals included:

- Intuit buying the naming rights to the L.A. Clippers’ new arena for $500 million

- FTX buying the naming rights to the Miami Heat’s home arena for $135 million

- Crypto.com buying the naming rights to the L.A. Lakers’ home arena for $700 million

These companies are willing to shell out massive piles of cash in order to build their brand and market themselves as important, trustworthy companies. However, given the massive size of the expenditures, it’s worth the time of any investor, executive, or board member of one of these companies to quantitatively estimate the ROI. In this article, I do exactly that by pulling data from SEC filings, historical stock performance, local government records of cities that have stadiums, company announcements, and media coverage of sponsorship deals. By the end of this article, you will know:

- How companies that bought stadium naming rights in the past have performed relative to their competitors and the overall market.

- How to know if you should sell a company that announces a naming rights purchase.

- How to decide whether a company you run or advise should buy the naming rights to a sports venue (e.g. high school stadium, college stadium, major league stadium, etc).

Let’s jump in.

What do you actually get when you buy “naming rights”?

A naming rights deal is about intangible assets. A typical deal might include the sale of something like this list of assets:

- The right to specify the name of the stadium

- The right to have your chosen stadium name and/or your company logo written up to a certain size on various parts of the stadium’s exterior (e.g. the roof and/or over the main entrance)

- The right to various signage throughout the interior and exterior of the stadium for use as advertisements

- The right to advertise your company as “the official provider of <thing or service> to <name of team that uses the stadium>”

- The right to have certain parts of the stadium painted and/or lit with your company’s colors

- The right to have the stadium name used in all official press releases of the stadium’s home team

- The right to have the in-game announcer say the stadium name and/or other sponsored messages about your company a certain number of times throughout every home game

- The right to have your company logo and/or name on the backdrop of certain press conferences held at the stadium

- The right to exclude anyone else from advertising on or within certain parts of the stadium

- Discounted options on buying certain TV commercial slots during televised games

- The right to use certain retail or vendor spots within the stadium and/or adjacent buildings

- The right to exclude competitor companies from advertising in the stadium and/or adjacent buildings

Of course, deals will differ from one to another, but that list gives a pretty good idea of the type of assets that are often included in a naming rights purchase agreement.

How stadium name deals are structured

With rare exceptions, stadium names are not paid for with a single lump sum. Instead, the headline dollar amount (e.g. “SoFi buys stadium naming rights for $625 million”) is actually paid in quarterly installments over the course of decades. For instance, SoFi’s purchase will be paid over the course of 20 years.

Equally important to know is that despite these deals being referred to as “purchases”, naming rights are almost never actually purchased — they are rented. Returning to the example of SoFi, the “purchase” agreement is actually an agreement for the stadium to have the name “SoFi Stadium” for 20 years (i.e. the same length of time that SoFi is making payments). In other words, SoFi agreed to rent the intangible asset of “naming rights” for the L.A. stadium for about $30 million per year, for 20 years. That is a hefty subtraction of free cash flow for a very long time. And as anyone who has owned a business knows, free cash flow is the lifeblood of a company.

To accept that kind of rigid constraint, you better be damn sure that the ROI you’ll get will be substantially better than what you’d get from instead using an elastic marketing budget on digital ads. If a $30 million Facebook ad campaign doesn’t work, you can shut it off in a day and only lose $82,000. If a $30 million stadium marketing campaign doesn’t work, you’re stuck with not just $30 million this year but also for the next 19 years. That’s a lot of risk which can meaningfully degrade a company’s long-term performance if taken recklessly. However, an even more significant consideration is that how a company’s management team makes one $100M+ budget decision reflects on how they make all decisions. If stadium names don’t provide a good ROI, then a company that buys them probably makes lots of other bad purchases too. If stadium names *do* provide a good ROI, then a company that buys them probably has good decision making processes in place, which means they’re likely to make other good decisions as well. To figure out which situation is more likely, let’s take a look at the historical ROI of some companies that have bought stadium naming rights in the past.

These companies were randomly sampled from the set of publicly traded U.S. companies which are current or recently terminated sponsors of NFL stadiums, have been public for the majority of the deal duration, and have been involved in the deal for at least 5 years. The time window over which each company is analyzed starts briefly before major news coverage of the deal began. The time windows all end in 2022. The stock performance of each company (adjusted for any splits and dividends) is compared against various benchmarks such as the S&P 500, a subset of closest competitors, and same-sector ETFs which have existed throughout the entire time window under study.

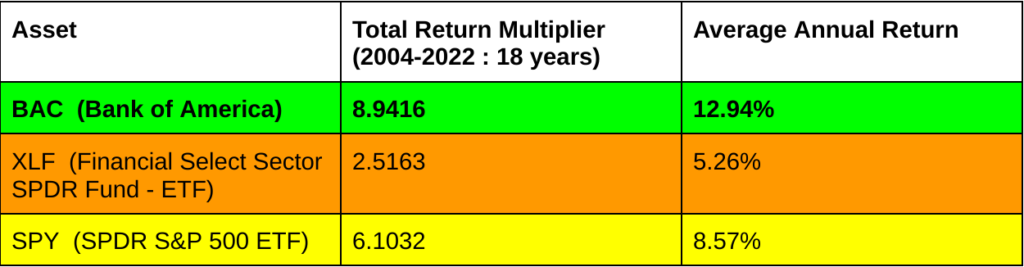

Case Study 1: Bank of America

VERDICT: Overperformed

- Substantially outperformed S&P 500

- Substantially outperformed sector ETF

On first look, it appears that Bank of America must have had great managers with great judgement about where to spend money. How else could they have performed so much better than both a financial sector ETF and the S&P 500 for almost two decades?

However, as you read through the next few case studies, you might start to wonder (as I did) whether Bank of America’s performance might not be as good as it first appears. The most obvious potential source of bias is the fact that the time period of our study includes the financial crisis. During the financial crisis, the federal government gave billions of dollars of assistance to Bank of America and certain other large banks. Not every company included in the XLF financial sector ETF received the same level of assistance. The discrepancy is even larger if we compare against the companies in SPY. To investigate this possibility, let’s re-run our analysis but this time just over the period after the financial crisis.

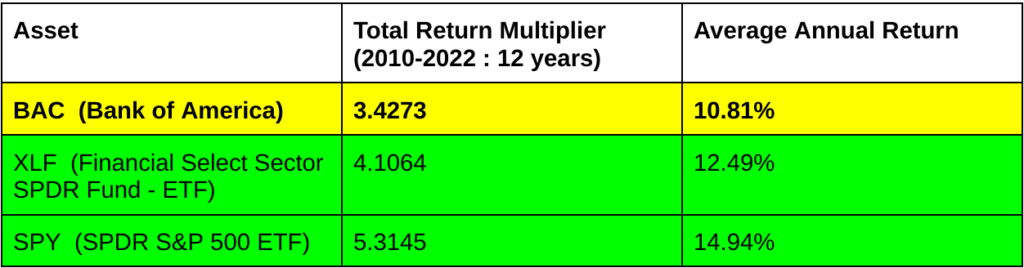

Case Study 1A: Bank of America (Post-Bailout)

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Underperformed sector ETF

These results are quite different from what we had before. This time, Bank of America’s stock noticeably underperformed both the financial sector specifically and the larger stock market in general. This isn’t enough data to definitively say that Bank of America’s overperformance measured in our first case study was entirely due to special treatment by the government. However, that explanation does seem entirely possible given the systematic underperformance after the special treatment was over.

Case Study 2: FedEx

VERDICT: Underperformed

- Moderate to substantial underperformance of most competitors

- Similar performance to XLI (not the best comparison ETF, but the closest available that existed for the full length of the study)

- Similar performance to S&P 500

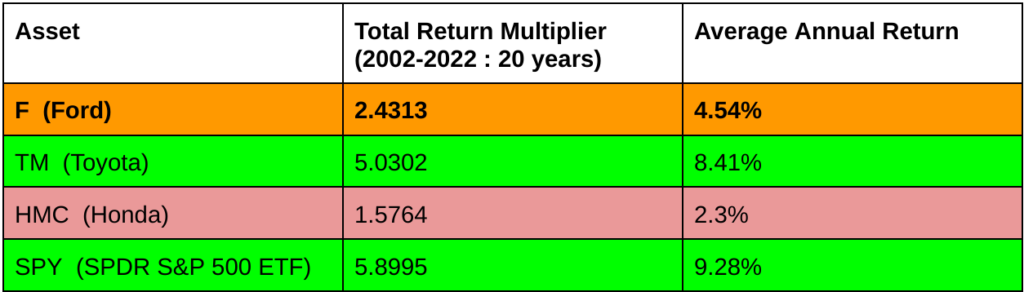

Case Study 3: Ford Motor Company

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Mixed performance relative to competitors

It’s hard to compare Ford to direct competitors since many competitors either have not been publicly traded since 2002, are foreign companies (and hence excluded from this study in an attempt to provide a more apples-to-apples comparison), have undergone substantial mergers or restructuring events, and/or also sponsor major league sports venues. However, despite those issues, it’s still clear that Ford has not performed well over the past two decades.

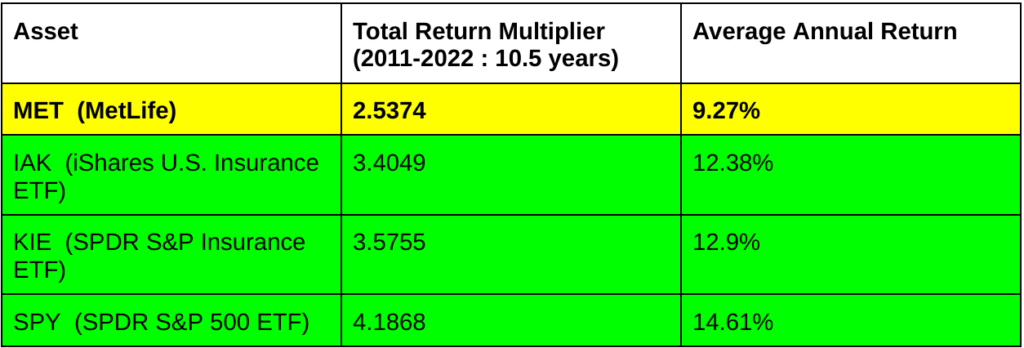

Case Study 4: MetLife

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Moderate underperformance of insurance sector ETFs

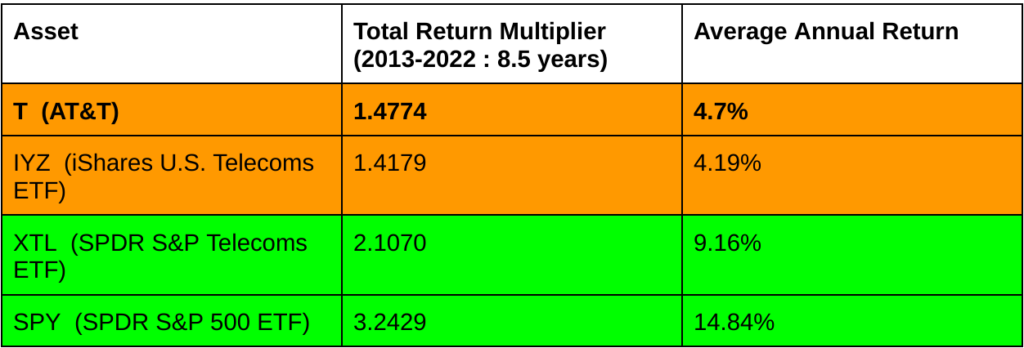

Case Study 5: AT&T

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Underperformed sector ETFs on average

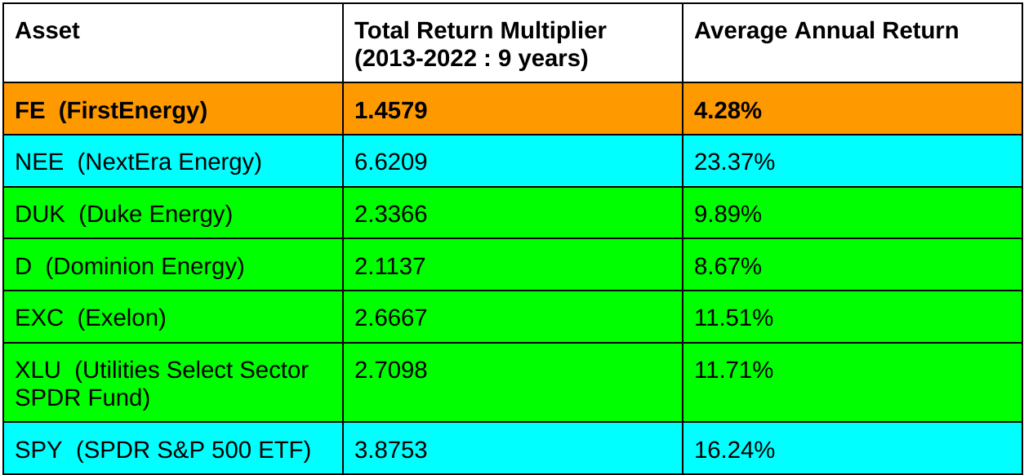

Case Study 6: FirstEnergy Corp

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Substantial underperformance of competitors

- Substantial underperformance of sector ETF

It’s worth noting also that as of 2022, FirstEnergy is involved in serious legal issues after it came out that the company had spent $64 million dollars bribing state government officials. There seems to be a pattern of energy companies that sponsor major league stadiums getting involved in scandals. For a brief period, the Astros baseball team played their home games in “Enron Field”. Chesapeake Energy also put their name on an Oklahoma NBA arena before it later become involved in a price-fixing scandal. In fact, if you take away just one thing from this article, it should be to never buy stock in energy companies with their names on stadiums. And if you run a hedge fund, you might consider them as short positions against an energy-heavy portfolio. (To access my complete model & analysis for such a strategy, subscribe to Axiom Alpha Market Intelligence and I’ll include it with the next issue).

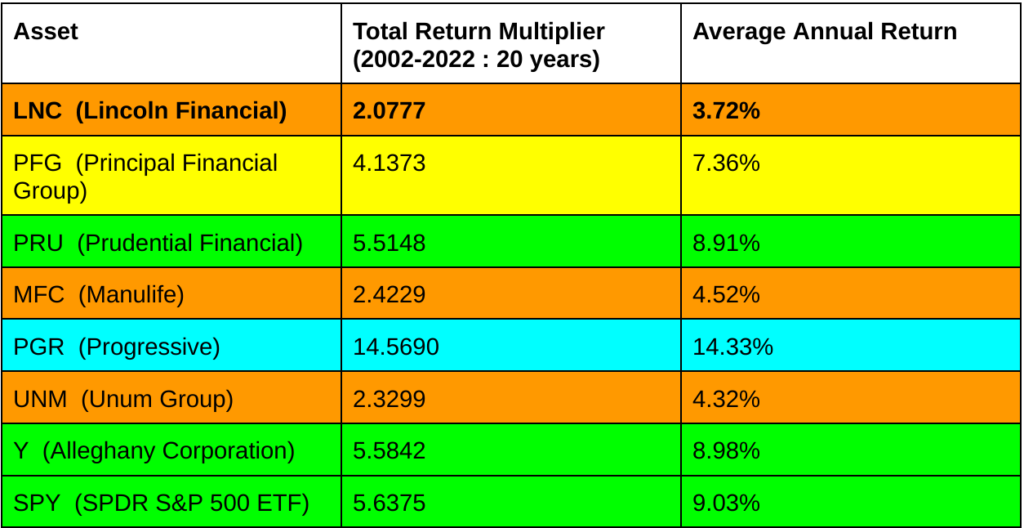

Case Study 7: Lincoln Financial

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Underperformed every competitor analyzed (many substantially)

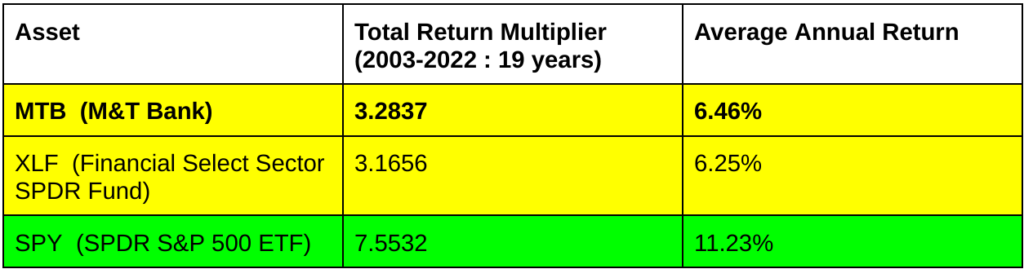

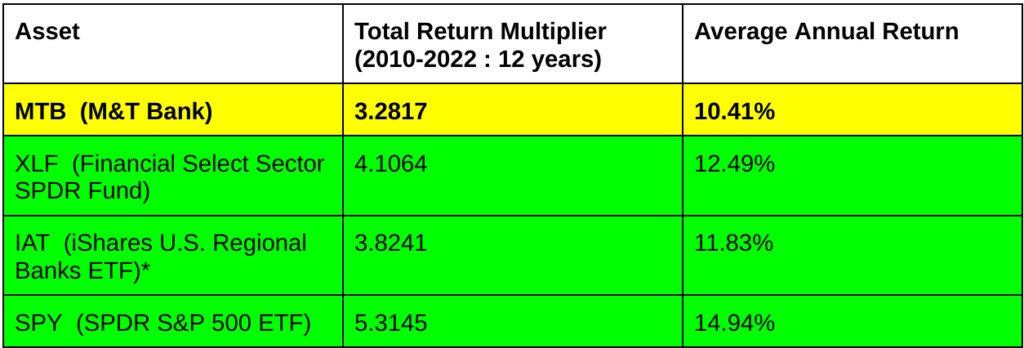

Case Study 8: M&T Bank

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Similar performance to sector ETF (even though M&T Bank got a government bailout during the 2008 crisis and not every company in the ETF did)

Unlike the situation we saw earlier with Bank of America, M&T Bank underperformed the S&P 500 even over a time window that includes the financial crisis. However, they still appear to perform similarly to the financial sector as a whole. Given that M&T also received more government assistance than your average finance company though, we have another opportunity to test our hypothesis. If stadium names are in fact generally bad purchases, then when we re-run our analysis for the period after the financial crisis, we should expect to see MTB flip to substantial underperformance relative to XLF. Let’s test.

Case Study 8A: M&T Bank (Post-Bailout)

Exactly as expected, MTB consistently underperformed both the finance industry specifically and the market generally after the financial crisis. I even included another bank-specific ETF here (which wasn’t included in the previous comparison since it didn’t exist in 2003). MTB also underperformed that bank-specific ETF.

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Underperformed sector ETFs

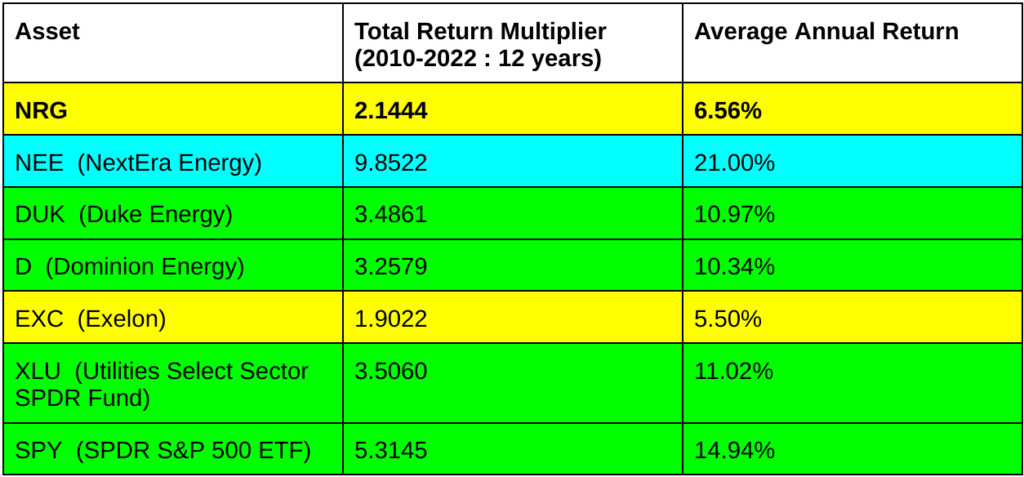

Case Study 9: NRG

NRG is an energy company with its name on a stadium, so you already know what to expect from our previous discussion.

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Substantial underperformance of most competitors

- Substantial underperformance of sector ETF

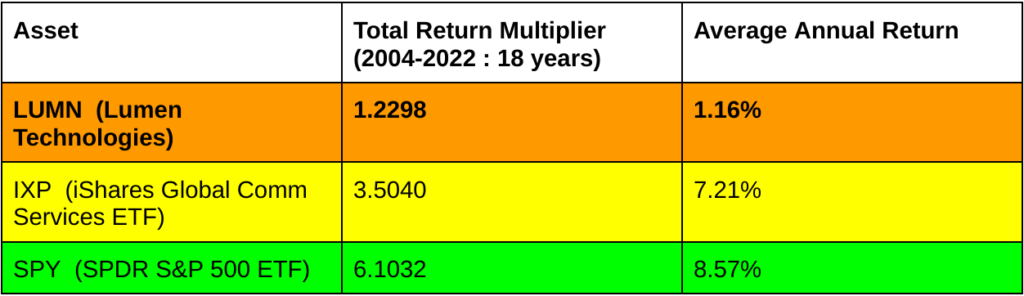

Case Study 10: Lumen Technologies

To accurately analyze Lumen Technologies, we have to account for several events. In 2002, a new stadium opened in Seattle with the name “Seahawks Stadium”. In 2004, Qwest Communications International bought the naming rights to the stadium which was renamed “Qwest Field”. In 2011, the stadium was rebranded to “CenturyLink Field” after Qwest was acquired by CenturyLink. In 2017, the company extended their naming agreement until 2033. Then in 2020, the stadium was rebranded to “Lumen Field” after CenturyLink restructured into three entities: Lumen Technologies, CenturyLink, and Quantum Fiber.

Ordinarily, I wouldn’t include a company that went through so many restructuring events because even if you can adjust stock prices accurately, you don’t know whether the merger event changed the management style. For example, Proctor & Gamble have been excluded because after they acquired Gillette, the new top level management did not clearly signal agreement with the original Gillette management’s decision to invest in the naming of Gillette stadium. In contrast, after each of the events Lumen and its predecessors was involved in, the post-event management team decided to reinvest additional dollars into the stadium sponsorship deal. For that reason, it seems fair to include them in our analysis. Here’s how they performed:

VERDICT: Underperformed

- Substantial underperformance of S&P 500

- Substantial underperformance of sector ETF

It’s also worth noting that in recent years Lumen has pivoted substantially into cloud and software more than its roots in telecom. If we were to compare them to their current competitors (which include companies like Microsoft and Oracle) rather than their historical competitors, their relative underperformance would have been even worse than it is in the chart above.

Total Return Statistics

Of the 10 companies we just analyzed, 9 underperformed a basic portfolio consisting of a 50/50 split allocation between their industry peers (represented as a sector ETF where one existed and by an equal weight index of direct competitors where one did not) and the S&P 500. Six of the companies underperformed the S&P 500 by more than 50%. Furthermore, if we adjust our analysis to only look at banks after they received financial assistance from the government, all 10 companies underperformed. That’s compelling, but not quite statistically significant. However, if we loosen our sampling criteria a bit, then we can look across a broader set of 98 publicly traded companies that bought naming rights for NFL, NBA, MLB, or NHL stadiums between 1973 and 2019. We stop in 2019 to avoid needing to analyze weird effects of massive government subsidies & fiscal stimulus during 2020 and 2021.

From this larger set of companies, two stand out for substantial overperformance: Qualcomm (QCOM) and Target (TGT). Given our earlier results being very subpar, it’s worth looking at what’s going on with these examples.

Qualcomm

Several things pop out of the details of Qualcomm’s agreement to purchase the naming rights to the San Diego Chargers’ stadium in 1997. The first is that Qualcomm paid a truly tiny sum ($18 million) for 20 years of naming rights. The second is that they paid this entire $18 million sum upfront rather than spreading it out over the duration of the agreement. The context for how this deal happened is that the city of San Diego was desperate for funding to finish an expansion of the stadium. Qualcomm stepped into the gap and got a 5-10x cheaper price than other companies paid around that time for similar name deals. In other words, Qualcomm didn’t go looking for a stadium naming deal. Instead, they acted opportunistically to seize an opportunity to make a deal with a desperate local government at a price that was only 10-20% of what other companies were paying for the same types of deals.

Target

Target has been very reluctant to release any financial information regarding their 1990 deal to name a Minneapolis NBA arena the “Target Center”. However, piecing together what we do know, it seems likely that the 25 year agreement carried a price tag of about $1-1.5 million per year. That’s about 25-50% of what companies were paying a decade later, adjusted for inflation, and just 10-20% of what companies were paying in 2021. Additionally, the Target agreement was deeper than just a name. The agreement also included provisions for certain NBA players to visit Target stores. Some basic modeling of retail customer behavior and attendance to NBA autograph events suggests that this provision alone might have been worth a substantial portion of the agreement. Target also hasn’t disclosed details about specific merchandise partnerships, but it’s quite possible that Target may also get a direct benefit in terms of discounts and/or exclusivity for certain branded merchandise. Finally, consider the fact that the Target Center is a mere 0.4 mile walk from Target HQ. How much cost could Target reduce in corporate employee churn & payroll by offering perks for NBA game tickets & events with players? All of that is in addition to the “standard” naming deal benefits including TV and in-person branding.

A Robust Pattern

Based on our analysis of Qualcomm and Target (and verified against a few other companies that outperformed but to a much lesser degree), we can define a clear set of properties that constitute a “good deal” when it comes to naming rights. If we then analyze our set of 98 companies and eliminate all companies that meet those “good deal” criteria, we find that the remainder systematically underperform in a significant way. That’s a pretty interesting result for anyone interested in long/short hedged strategies. It also means that if I personally held any Crypto.com stock in the private market, I’d dump it because its stadium deal doesn’t meet the “high quality” deal criteria. Complete data & results for this extended study, along with a model investment strategy based on it, will be included in my next issue of the Axiom Alpha Market Intelligence newsletter (a paid subscription for deep market data & analysis). For the more casual reader, you can subscribe to the Axiom Alpha Letter (of which this article is an example issue) for free!

Disclaimer: Nothing in this article should be considered investment or financial advice. This content is for information & educational purposes only. Neither Homology Group Inc. nor any of its representatives will be liable to you for any actions you take or don’t take based upon the information in this article or other Axiom Alpha content. Axiom Alpha is a brand name of Homology Group Inc.