“Kara sold her software company for $1.33 billion and paid ZERO capital gains taxes. I don’t mean the tax bill was deferred to a later year. I mean the tax bill was erased from existence. Permanently.”

Back in the good old days (1862-1986), the Homestead Act allowed U.S. citizens to claim up to 160 acres of government-surveyed land for free. Unfortunately that opportunity doesn’t exist anymore. However, something even better does: Opportunity Zones (OZs). That’s not hyerpbole either. Opportunity zone tax breaks ARE actually more valuable than getting 160 acres of undeveloped land, and I’m going to show you how.

People who have heard of opportunity zones before often have two misconceptions.

The first misconception is that opportunity zone tax loopholes are only useful to people who are already wealthy. That’s wrong. It will help if you have at least a few thousand dollars, but you certainly don’t need millions. In fact, opportunity zones are probably the most useful to ambitious people who want to create companies but haven’t started yet.

The second misconception is that the opportunity zone tax loophole is only useful for real estate investing. That’s also completely wrong. In 2019, the IRS published a 544 page document with painfully detailed commentary on all sorts of various things you can do with opportunity zones. That information made it very clear that many businesses and business owners (whether investors or founders) can benefit from opportunity zone tax breaks if they are willing to follow the relevant rules.

In fact, the very generality of opportunity zones sometimes confuses people. How can one tax rule be equally useful to Amazon, a Silicon Valley startup, a local ice cream shop, a crypto trader, a hotel investor, a one-woman services business, and an aspiring entrepreneur who hasn’t even created a company yet?

The answer is that there are actually a LOT of tax rules related to opportunity zones, most of which are unfamiliar even to professional investors. These rules are Legos that can be assembled to provide all sorts of different benefits to all sorts of different people and businesses. I’m going to teach you to wield these rules as a secret weapon to obliterate tax bills, get subsidized assets from the government, and destroy your competitors who aren’t using opportunity zone strategies.

This letter is different than my typical letters. It’s 5 times longer and 50 times more valuable. It’s a precise guide to opportunity zone strategies that can save you literal bricks of cash that would otherwise disappear to taxes. Some of the strategies are a bit complicated, but the cost reduction they provide is bigger than the differences that frequently dictate which of two competitor businesses survive. As Robert Frost once said:

“Two roads diverged in a yellow wood. At the end of one were the basic bitches, and at the end of the other was a qualified low-income census tract designated as an opportunity zone, and I took that less-traveled road.”

Maybe those weren’t his exact words, but it was something like that.

By the end of this letter, you will know:

- How to pay zero taxes on a $1 billion cash exit

- How you and your business can avoid paying taxes on 25 years worth of *realized* capital gains

- How to eliminate depreciation recapture taxes

- How a startup can raise more money, faster, at a higher valuation

- How to find investors desperate to invest in your small business, even if you’re not growing like a VC-fueled Silicon Valley startup

Let’s dig in.

How opportunity zones work

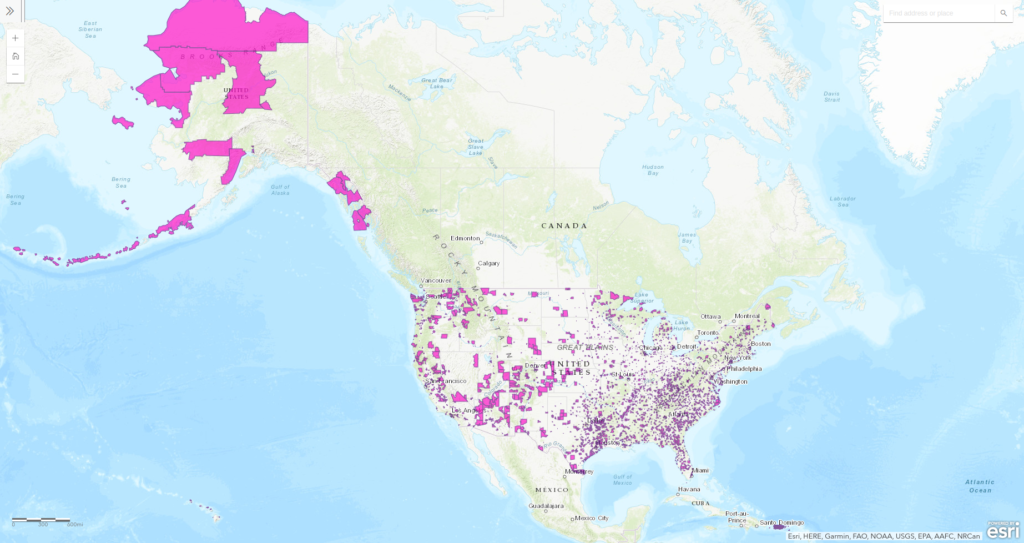

An opportunity zone is just a low-income census tract that has been designated as an opportunity zone by a state government. Here is a map showing all opportunity zones in the country:

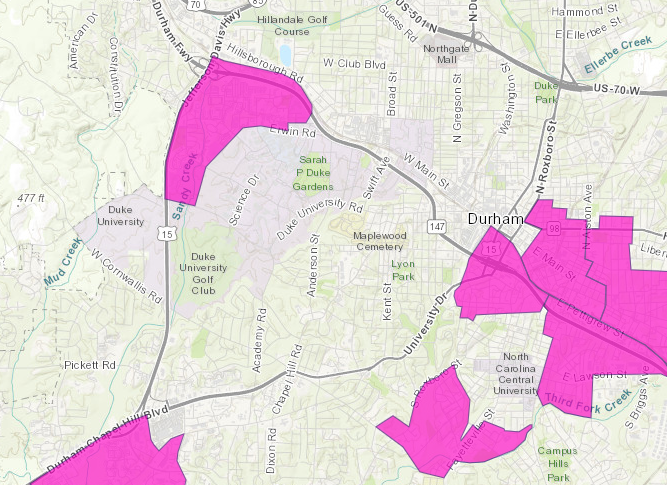

The various tax rules related to opportunity zones are all government incentives for investors and companies to come in and create jobs, infrastructure, and wealth in these areas. Some zones are vast swaths of barren land in the middle of nowhere. Others are run-down areas in the middle of cities. And still others are right next to universities where college student populations depress income levels even if the areas are developed. For instance, here is an opportunity zone located right next to Duke University in North Carolina:

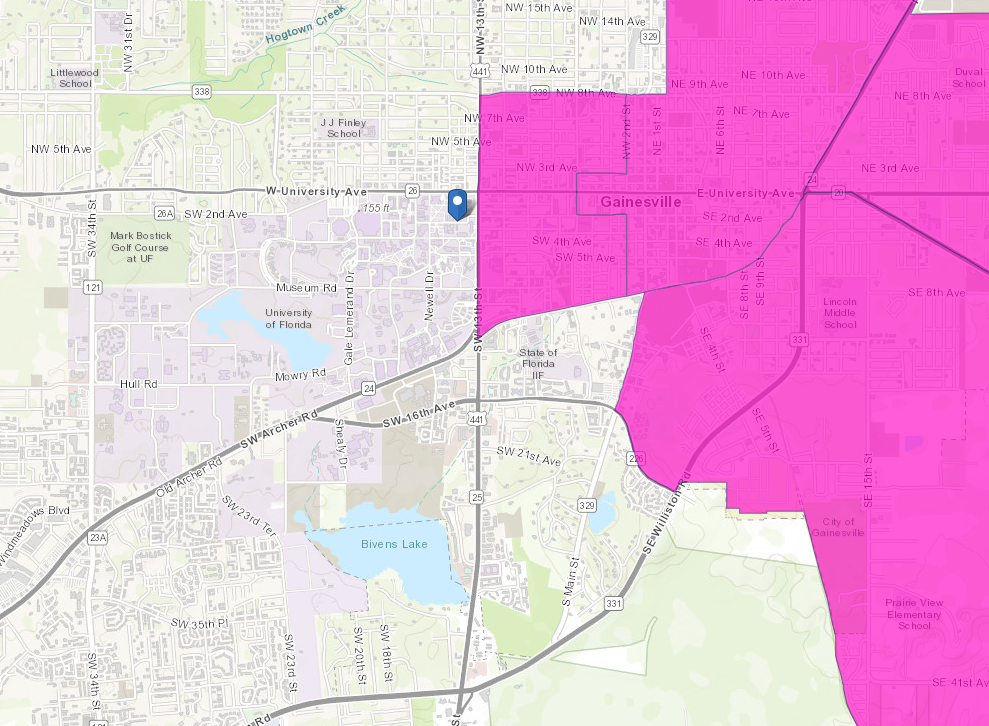

And here is a big block of opportunity zones right next the University of Florida:

The essence of the opportunity zone tax loophole is that if you reinvest capital gains into businesses or property located in an opportunity zone, then you can defer some taxes and eliminate other taxes altogether. However, there are certain strategies that will allow you to benefit from this loophole even if you don’t have any meaningful capital gains right now. I’ll explain how that works later in this letter.

The basic setup is that any person or company which can meet four sequential requirements will benefit from privileged tax treatment:

- Sell property, stock, crypto, NFTs, or anything else that results in a capital gain before December 31, 2026.

- Reinvest the amount of the capital gain (e.g. if you bought stock for $500 and sold it for $600, then reinvest the $100 gain) into a type of investment fund called a “qualified opportunity fund” (QOF) within 180 days of when the gain was realized. A QOF is a special-purpose business entity that must invest into businesses or property within one or more opportunity zones.

- Hold your QOF investment(s) for at least 10 years.

- Sell your QOF investment(s) before December 31, 2047.

If all four conditions are met, then you receive two tax advantages at different times.

The first tax advantage is a deferral of tax on the initial capital gains that you reinvested into the QOF. The deferral pushes that tax bill back until you file your return for 2026 (about 5 years from the time I’m writing this). In the meantime, those capital gains can be put to work in investments that go up in value. That brings us to the second tax advantage.

The second tax advantage is a complete elimination of capital gains tax on any increase in value of those QOF investments. Technically, this is accomplished by a law which resets the “tax basis” of the investment to “market value” when you sell. That should perk up the ears of anyone familiar with depreciation recapture because it means that you don’t have to ever repay depreciation deductions! More on that later though.

Example 1: simple QOF investment math

Bob has $2 million invested in the stock market. $1 million of that is unrealized capital gains. It doesn’t matter whether those are short or long term capital gains–either can be reinvested into a QOF.

Bob sells his entire stock portfolio in May 2022. If the gains are long-term capital gains, then Bob would owe $200k = 20% of $1M in capital gains tax for 2022 (if the gains were short term, that bill would be almost twice as much). However, Bob chooses to invest $1M in a qualified opportunity fund in August 2022. Since that is less than 180 days after he recognized his $1M gain, he has eliminated his entire $200k capital gains tax bill for 2022.

Over the next 5 years, Bob’s QOF investment goes up in value from $1M to $2M. He has to file 2026 taxes now, which means he owes his $200k tax bill. Note that it is still $200k, not $400k, despite the QOF investment doubling in value. For simplicity, I’ll assume Bob pays the $200k with money he has in a bank account outside the QOF. (There are ways to take tax-free distributions from a QOF to pay that $200k tax bill, but those would complicate our discussion more than is necessary.)

Bob continues to hold his QOF investments all the way until 2047 when he sells them for $6 million. That means over 25 years, his $1 million has turned into $6 million (a $5 million gain). If the long-term capital gains tax is still 20% in 2047, then Bob would normally owe $1 million = 20% of $5 million in taxes. However, because this gain was held for more than 10 years through a QOF, Bob owes ZERO dollars in taxes.

There is no deferral happening here. Bob never has to pay that million dollar tax bill — the tax bill is simply erased from existence as if Thanos had snapped his gauntleted fingers.

Example 2: the tax-free billion-dollar exit

Kara is an aspiring entrepreneur who wants to create a new word game app. She wants to put $1000 of her own money into the company to start it.

Kara could just transfer $1000 from her bank account to the business’s bank account. However, if her company becomes very successful and is eventually acquired, she would have to pay a huge amount in capital gains tax. So instead, Kara checks her Robinhood account. She’s been holding two shares of Tesla stock since right after the stock split in 2020 which means she’s sitting on $1120 of unrealized capital gains. She forms an LLC to serve as her QOF and deposits the $1120 into her new LLC bank account. Her LLC then forms a wholly-owned C corporation subsidiary which will be the startup that actually builds the new app. Importantly, she starts working at a coworking center located in an opportunity zone so that her C corporation immediately starts off as a QOZB (qualified opportunity zone business).

Kara’s company begins to grow. Over the next two years, she takes on one outside investor through another QOF which takes 20% of her corporation. She scales up to a team of 8 people. Five people work from her original coworking space (although now in a larger, dedicated office) and 3 people work remotely from another coworking space in a different opportunity zone. The app’s computing & data storage needs are supported entirely by cloud infrastructure rather than company-operated servers. By this time, the app is generating over $50 million / year in revenue.

Over the next 10 years, Kara’s company grows by acquiring other game & puzzle apps run by lean teams and relocating their teams to office spaces in opportunity zones. By the end of this period, the company is bringing in over $500 million in annual revenue. At this point, she decides to sell her company. She asks Goldman Sachs to look for buyers and eventually gets an all-cash offer from the New York Times for $1.33 billion. She takes the deal.

At the time of sale, 20% of the corporation has been sold to an outside investor and another 5% has been given to various employees over the years. That leaves Kara (through her QOF) with a 75% stake in the corporation.

75% of $1.33 billion is $1 billion: Kara has a $1 billion exit. Ordinarily, Kara would owe long-term capital gains taxes on that entire amount of $1 billion minus her $1120 of initial capital. At today’s long-term capital gains rate of 20%, that’s a two hundred million dollar tax bill! If Biden succeeds in raising the long-term capital gains rate to 39%, that would be a $390 million tax bill! However, since Kara’s initial investment was through a QOF, she owes ZERO TAXES.

This strategy is applicable to the MAJORITY OF STARTUPS. Most modern tech startups are asset-light internet companies or internet service agencies which can easily comply with opportunity zone business requirements. Most media businesses (including social media, newsletter & influencer businesses) are also flexible enough to comply with opportunity zone business requirements. Most e-commerce businesses can qualify. Many small local businesses can qualify if they are willing to be flexible on location. Real estate businesses can often qualify. Even some asset-heavy businesses such as manufacturers can qualify.

Let’s talk about exactly how to execute on this. (Also, this article is a real issue of the Axiom Alpha newsletter so if you want to learn about more financial strategies like this, subscribe to join our community of entrepreneurs & investors!)

How to create a QOF

A qualified opportunity fund (QOF) is a business entity used for a specific purpose and which satisfies certain conditions. Here are the five requirements and best practices to create your own qualified opportunity fund:

- The QOF should be an LLC, LP, or C corporation. If it is an LLC or LP, then it must have at least two members/partners (single-member LLCs are not allowed).

- It is incorporated in a U.S. state, DC, or a U.S. territory. If the business is incorporated or formed in a U.S. territory (rather than a state or DC), then it must be formed for the purpose of investing in opportunity zones only within that territory.

- The business entity may be a pre-existing business entity. However, to minimize the chance of an audit, it’s highly recommended to form a new entity and include in its formation document that the entity is formed for the specific purpose of investing in qualified opportunity zone property.

- The business entity must elect QOF status by filing form 8996 annually with its tax return.

- At least 90% of its assets must be “qualified opportunity zone property” which can be any combination of (1) stock in a QOZB corporation, (2) partnership interest in a QOZB structured as an LLC or other pass-through partnership entity, and/or (3) qualified opportunity zone business property. However, this requirement doesn’t take effect immediately which means the QOF has time to find qualifying investments without rushing. Additionally, the 90% rule temporarily loosens if you deposit more cash into the QOF.

What is “qualified opportunity zone business property” (QOZB Property)?

(I know… I’m sorry for the word salad. Blame Congress.)

Qualified opportunity zone business property is tangible property that (1) has been or will be owned or leased (starting in 2018 or later) by a corporation or partnership, (2) is used in the active business of such corporation or partnership, and (3) falls into one of the allowed categories. The most common allowed categories are the following:

- OZ real estate that you purchase and then “substantially improve” within 31 months. In this context, substantial improvement means spending as much in renovations as the cost of the original real estate minus the land value. Note: the 31 month requirement can be extended for government-caused permitting delays.

- New construction real estate in an OZ.

- Leased real estate in an OZ. You must have started leasing the property no earlier than 2018. Nobody is required to “substantially improve” such leased property in order for it to qualify as QOZB Property.

- OZ real estate that you purchase from a local government who obtained the property through an involuntary transaction (e.g. due to nonpayment of tax by the homeowner).

- OZ real estate that you purchase after it has been vacant for several years.

- Any type of (new or used) machinery, equipment, or other tangible property which (1) can be depreciated or amortized and (2) has never been used in that particular opportunity zone by any business before. The property can be either owned or leased. There are even several safe harbor rules to include in this definition certain property which spends substantial time outside of an OZ. (e.g. a company truck which is normally parked at an office in an OZ but which is frequently driven out of the OZ for business).

- Inventory produced by the business.

Some examples of property that are NOT qualified opportunity zone business property are:

- Undeveloped land in an OZ which is not put to any significant active use. For example, someone purchases land primarily just to benefit from appreciation of the land over time, but they also let people pay $10 to park there during football games. (This fails to be QOZB Property because it fails requirement 2 above — it isn’t being used in an “active” business.)

- OZ real estate leased out under a triple net lease. The IRS reasons that triple net leases are not an “active” business since the entire burden of property ownership is essentially transferred to the lessee.

- A used commercial riding lawnmower bought from a landscaping company currently located in the same opportunity zone.

How to meet the QOF partnership requirement

Earlier, I mentioned that single member LLCs cannot be QOFs which is an annoyance to many people. However, the solution is very simple. Find a friend (or form an empty shell corporation if you have no friends) to buy a tiny fraction of the QOF (e.g. 0.01% or $1 or something like that). Wa-La — you now have a 2-member LLC which will be taxed as a partnership rather than a disregarded entity. I didn’t mention this technicality in my example of Kara, but she would have had to do this for her QOF.

How to create a QOZB

To create a qualified opportunity zone business, you’ll need to create a business entity that meets seven requirements:

- The QOZB should be an LLC, LP, or C corporation. If it is an LLC or LP, then it must have at least two members/partners (single-member LLCs are not allowed).

- It is an active business. Most “normal” businesses are active businesses. However, as previously mentioned, leasing real estate under a triple-net-lease is not.

- At least 50% of the total gross income is derived from the conduct of a business in a qualified opportunity zone. There are several ways this requirement can be fulfilled (only one needs to be met): (a) at least 50% of the hours worked by partners, contractors, and employees could take place in an OZ, (b) at least 50% of compensation to partners, contractors, and employees could be for services performed within an opportunity zone, (c) the tangible property and management operations within an opportunity zone are necessary for the generation of at least 50% of the gross income of the business, or (d) the “facts and circumstances” (legal jargon) dictate that at least 50% of gross income is derived from active opportunity zone business operations.

- At least 40% of the intangible property (e.g. patents, trademarks, etc) must be actively used inside a qualified opportunity zone. This is a slightly gray area since it’s difficult to assign a location to something like the use of a patent. In general though, things like using a trademark on the website of a business that has its office and employees in an OZ will probably count towards the 40%. On the other hand, a patent that was developed by a company operating outside of any OZ and which is later acquired by a QOZB might not count towards the required 40%.

- At least 70% of the tangible property owned or leased by the business must be qualified opportunity zone business property. (We covered the definition of qualified opportunity zone business property in the previous section on QOFs).

- No more than 5% of a QOZB’s assets can be “nonqualified financial property”. Nonqualified financial property includes most types of financial assets such as stocks and bonds but excludes cash, loans with a term of 18 months or less, and accounts receivable acquired in the ordinary course of business. There are some additional details around this rule, but they aren’t that important to most businesses. If you want to create any sort of business that relates to finance though, you’ll need to carefully look at all details.

- The business is not a “sin” business or a company that leases property to a “sin” business. Sin businesses are: any private or commercial golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack or other facility used for gambling, or any store the principal business of which is the sale of alcoholic beverages for consumption off the premises.

Example 1

A landscaping company is set up as a C corporation. The company rents a small office with an adjacent fenced area of land where they store all of their trucks, driving lawn mowers, and other equipment. The office & land are inside an opportunity zone. All administrative work is done from the office. Every day, employees come pick up equipment and use it to service customers both inside and outside of the opportunity zone before returning the equipment at the end of the day. The business is a QOZB (unless it does something unexpected like buy a million dollars of stock which might jeopardize the 5% limit on nonqualified financial property).

Example 2

Amanda & Mike live together in an opportunity zone. They decide to create a Youtube channel together. They create a 2-member LLC (they are the two members) to run their Youtube business. They operate from a home-based office and earn revenue through youtube ads, sponsors, and Amazon affiliate sales. The business is a QOZB.

Example 3

Joe sets up a C corporation that buys some barren land in an OZ in Colorado. He contracts engineers and developers to level the land, to build a small office building, and to add gravel roads and RV sized parking spaces. He also plumbs in a septic system and RV hookups for water, sewage, and electricity. He then begins operating the new RV park. The RV park is a QOZB.

Example 4

The IRS’ Final Regulations on QOZB’s gave a rather interesting but nuanced example of an intellectual property holding company with a headquarters in an QZ which DID qualify as a QOZB despite concerns about the 40% intangible property rule. This is a very relevant example for many tech companies which may be able to structure either themselves or a subsidiary as a similar IP holding company that can generate major tax breaks.

How startups & small businesses can find eager investors

There are a lot of investors who are aware of opportunity zones but don’t want more real estate exposure and don’t know of any good businesses which are both QOZBs and currently raising money. In fact, many investors don’t fully understand the regulations. They think of QOZBs as being hair salons in bad neighborhoods. Now that you know how flexible the definition is, you can use it to your advantage. If you can become a QOZB, then go knock on some doors or cold email some inboxes. Target family offices in your area. Family offices are special investment businesses which manage the wealth of one very wealthy individual or family. They are always looking for new investment opportunities, and because they Many family offices are more flexible than VCs and would be very interested in investing in a QOZB. You can also approach angel investors and alumni from any universities you’ve attended.

You can pitch that your business will be a QOZB and that you will set up a QOF through which they can easily invest. If you actually want to run with this strategy and have questions, feel free to email me using the form at the end of this letter.

How a company can directly benefit from an OZ

We’ve talked about how the people who start and invest in companies can benefit from OZ tax breaks, but OZs can also help companies themselves. One way OZ tax rules can help is by making it easier to get investors as I just mentioned. However, another way is for a company to simply use the rules in the same way a human would: by reinvesting realized capital gains.

Capital gains for a company could be from selling real estate it previously used in its business, from selling stock in a subsidiary, or from selling a partnership interest in a joint venture.

For companies that have more than a couple months of cash in the bank, it’s also very advantageous to hold a portion of that excess value in stocks or other assets expected to generate more return than the 0.1% interest rate a bank might offer. From time to time, such holdings would be adjusted which can generate capital gains for the company.

Once the company has capital gains to reinvest, it might purchase a new office building or warehouse in an opportunity zone through a QOF. Alternatively, it might start a new line of business through a two-tier QOF-QOZB subsidiary. Doing so is prudent for new lines of business which are somewhat experimental or adjacent to the company’s primary line of business. Then if the new line of business doesn’t work out for the company for some reason or if the company falls on hard times and needs cash, it can sell the subsidiary tax-free.

Big corporations also frequently have venture capital arms where they invest in new companies in their industry. This gives them a way to hedge the risk that one of those companies becomes a serious threat to their own. It also gives them a foot in the door to acquire that startup if they do become a threat or if they have some technology that the big corporation needs. If the startup can qualify as a QOZB, then the big corporation would be foolish not to invest through a QOF to obtain the extra tax benefit.

The more successful a business becomes, the more capital gains it is likely to have and thus the more incentive it has to take advantage of opportunity zones. However, even small companies can directly profit from OZs by compartmentalizing any aspect of their business which is separable from the whole into a QOF-QOZB two-tier subsidiary. In fact, you as a founder can even simultaneously hold your main company through a QOF while your main company itself has one or more QOF subsidiaries. I know that sounds a bit convoluted, but it’s very possible to do and can enable both you and your company to retain huge amounts of money that would otherwise be paid in taxes. However, if your company gets big enough to justify owning real estate, you can get all of that plus MORE by combining the benefit of tax-free gains with the benefit of real estate depreciation.

The double benefit of OZ real estate

Penelope buys a residential duplex for $1.25 million in 2022. According to the tax appraisal, 20% of the value ($250k) is attributable to the land while 80% of the value ($1 million) is attributable to the building. Penelope operates the property as a rental property until the year 2047 when she sells the property for $3.75 million ($2.5 million over her original purchase price).

Assuming Penelope qualifies (via her income or real estate professional status), she can take a deduction of 3.64% of the building’s value each year for 27.5 years. Since Penelope bought in 2022 and sold in 2047 (a 25 year holding period), her cumulative deduction is 91% of the building value. That’s $910k = 91% of $1 million.

However, when Penelope sells her property, she isn’t just taxed on the $2.5 million appreciation of the property. She is also taxed on $910k of “depreciation recapture” (and this recapture is taxed at a rate up to 25% rather than the maximum 20% long term capital gains rate). That’s how ordinary real estate depreciation works — it’s merely a tax deferral mechanism not a tax elimination mechanism.

Now let’s compare what would happen if Penelope were to do exactly the same thing except this time she bought her property through a QOF.

In this case, since 25 years is more than 10 years, we already know that Penelope won’t owe capital gains taxes on the $2.5 million of appreciation. However, the OZ tax rule doesn’t just apply to capital gains. It also applies to depreciation recapture. This means Penelope doesn’t have to pay 20% long term capital gains on her $2.5 million appreciation AND she doesn’t have to pay 25% depreciation recapture gains on the $910k of deductions she took. Penelope pays ZERO taxes on anything AND she still gets to deduct depreciation.

That is unlike any other tax loophole. The no-payback deductions alone are equivalent to getting a massive government subsidy on purchases of OZ property. Imagine getting to buy a stock that generates dividends, write off the cost of the stock, receive dividends for 25 years, and eventually sell the stock at a gain without paying any taxes on that gain or repaying the deduction. That’s exactly what this is but for real estate & rental income rather than a stock & dividends.

How to use QOFs for a startup if you don’t have capital gains

If you have $1000 in your bank account and want to create a startup with that $1000, you won’t be able to benefit from the QOF tax-free exit. The reason is that you can only invest money coming from capital gains into the fund. Unfortunately that means just having money isn’t enough to create your tax-privileged startup. However, there are some creative ways you can try to get around this.

The fortunate thing is that most startup founders don’t put much of their own money into a startup (because most founders don’t even have much money). That means you don’t need much capital gain to benefit from the eventual tax break. In fact, hypothetically you could probably make do with as little as $10. Many founders will have that already in the form of unrecognized gains from crypto or Robinhood stocks. If you truly have zero capital gains though, then try this:

Buy 10 different stocks. Choose randomly if you know nothing about stocks. The more volatile the stocks, the better. Watch them each day and whenever one is up by more than 3%, sell it and then reinvest the principal (but not the gain) into a new stock. Don’t sell anything at a loss until the next year.

That’s not the best strategy for investing generally, but it’s a great way to get at least $10 in realized capital gains. Once you have those realized capital gains, you can contribute it to your startup through a QOF. Of course, you may need more than just $10, and that’s fine. As long as you have SOME realized capital gains, you can contribute the remaining money needed to your startup as a loan rather than as an equity purchase. QOZBs can take loan money without any issue about whether or not the loan money comes from capital gains or not.

Note: If you are finance nerd who regularly trades stocks or crypto, you can do better than this by simply using wash sale gains that would normally be an annoyance. If you don’t know what that means but want to use the strategy in this section, email me what your situation is, and I’ll give you my thoughts. If you don’t execute on the strategy appropriately, you risk losing your tax privileges under the “anti-abuse” regulations for OZs.

Future political risks & opportunities

Political winds can always change the tax law. Opportunity zone tax laws had huge bipartisan support when they passed a few years ago so it’s unlikely that those will be substantially changed. However, there are definitely strong political battles ongoing about taxes. Here are 6 changes to the tax law that can indirectly affect opportunity zone businesses & investments:

- Long-term capital gains may lose their tax-privileged status and become taxable at ordinary income rates. This change is currently included in Biden’s proposed tax changes. If this happens, it makes the tax-free haven of OZ investments substantially more valuable since you would save about twice as much in taxes as currently.

- The corporate tax rate may increase. For the same reason as above, this would make OZ investments much more valuable to corporations which have capital gains.

- Individual ordinary income tax rates may increase. If this happens in conjunction with long term capital gains being classified as ordinary income (both things are included in Biden’s current proposal), it would make OZ investments more valuable. Additionally, in this scenario it’s likely that the maximum real estate depreciation recapture tax rate would increase from 25% to the ordinary income tax rate. That would strongly incentivize real estate investors to move into OZs. That in turn would create an opportuntiy for QOZBs already set up to quickly & easily accept more investment. It also could lead to significant local disparities in real estate performance as investors pile into opportunity zones and dump buildings in adjacent, non-OZ census tracts. This is an opportunity for fast-moving QOZB small businesses and startups but also a risk to real estate investors holding property in OZ-adjacent census tracts.

- Tax deferred 1031 exchanges may be eliminated or capped at a low threshold. If you are a real estate investor, diversifying into opportunity zone investments is a valuable way to hedge this risk. Additionally, holding OZ property would be an interesting way to speculate on legislative elimination of 1031 exchanges. If 1031 is eliminated, investor demand will shift heavily towards OZ’s which will drive up your property value and enable you to profitably exit your OZ investment early (without the tax benefits but with lots of profit). If 1031 is not eliminated, you still own the OZ property and can generate both cash flow and long-term tax-free gains. It’s a win-win scenario for people and companies getting into OZs early enough.

- In April 2022, a new bipartisan bill was introduced to Congress which would modify the opportunity zone laws in a few ways. These bills are currently just early-stage proposals, but here are the most important changes they could have: (1) phasing out certain opportunity zones based on new income criteria and updated 2020 census data, (2) adding new reporting requirements for QOFs, and (3) extending the tax deferral window from 2026 to 2028. The first two are minor annoyances but are easily handled with appropriate planning. The third point is very interesting because not only would it increase the direct tax deferral benefit, it would also reactivate an old opportunity zone benefit which already expired under the current law. If reactivated, the new version of that benefit would give anyone who gets into OZ’s before the end of 2022 a 15% discount on their deferred taxes when they eventually paid them. It would also give a 10% benefit to anyone who gets into OZ’s before the end of 2023.

- If Biden’s “billionaire” tax proposal (which has been cleverly named so that people don’t realize it doesn’t only apply to billionaires) is passed, it could have a substantial effect on OZs. In its current form, the tax is actually a prepayment of a portion of capital gains tax. This leaves open the possibility for wealthy individuals and companies to avoid the billionaire minimum tax by migrating assets into OZ property and businesses which are not subject to capital gain tax if held long enough.

The summary version of all those points is that political winds towards higher & more taxes just make opportunity zones more valuable. Furthermore, the fact that opportunity zones have strong bipartisan support means they are probably the best safe harbor for wealthy individuals and companies to ride out a decade or two of tax law tightening.

If you found this letter valuable, subscribe to the Axiom Alpha email list to receive future letters before they become public on this blog.

And if you’re interested in using QOFs or QOZBs, shoot me an email with a brief description of what you’re interested in doing. My company consults & partners with entrepreneurs and investors to help them make more money by structuring businesses & deals, helping them to develop and execute tax and financial strategies, and helping them identify new opportunities. Unlike many internet forms, this one will get you a real response from a real human being with deep financial competency.

Appendix A: Business model risk factors

There are three important issues that startups are likely to come across if they want to maintain QOZB status as they grow.

1. Avoid cloud infrastructure agreements that may be deemed “leases”

Cloud computing & data storage is provided through “service contracts” or “service level agreements” (SLAs) which can have very different terms. The more control over the hardware and the more liability for performance that you assume rather than the cloud provider, the higher the risk that the IRS will deem the agreement to actually be a “lease” even if it’s called a “service contract”.

Since a successful asset-light software business will typically use far more cloud machinery than onsite machinery, it’s very important for such a business to NOT have cloud infrastructure count as “leased tangible property” since most of that property is not located within opportunity zones. Feel free to email me if you’re thinking of adopting a QOZB strategy and want to get an idea of whether your company’s cloud usage is likely to be problematic or not.

2. Be cautious with acquisitions

If you anticipate growing your company through acquisitions, then you’ll need to take precautions. There are four possible routes to take without entirely losing your OZ benefits.

The first route is to not use this hierarchy of ownership:

You –> QOF –> main company C corp

but instead this hierarchy of ownership:

You –> holding company C corp –> QOF –> main company C corp

Any acquisitions of other businesses would then be done through the holding company above the level of the QOF. This is a very flexible approach because it also frees you to form other operating subsidiaries of the holding company if your company needs to expand to include offices or teams outside opportunity zones. The main drawback is that you no longer can sell your (top level holding) company tax-free. However, your holding company will still have the ability to sell its QOF subsidiaries (including your original main company) tax-free.

The second route is to structure any acquisitions as asset purchases. That can be very difficult to do if you’re acquiring a large company with a lot of employees and/or tangible assets, but if you’re acquiring relatively lean startups with few employees and few tangible assets, it’s very feasible to accomplish this. There are some considerations regarding the “location” of intangible intellectual property such as patents and trademarks that you’ll need to account for though so consult with an expert if you reach this stage if you don’t want to read the hundreds of pages of regulation yourself.

The third route is one that only works in very specific situations. Whatever business entity you setup as the QOZB is only allowed to hold a maximum of 5% of its assets as “nonqualified financial property”. However, if your QOZB company is large enough and your acquisition target small enough, then you can just buy the company through a conventional acquisition. Furthermore, if your QOZB business is considered a startup company under the OZ regulations, the 5% rule is loosened somewhat. That loosening means you can potentially use this route for early acquisitions and then later restructure your company to comply with the 5% rule by the time you’re required to do so. In addition, the 5% rule actually only applies to the initial cost basis of an acquisition so any unrealized gains post-acquisition won’t push you over the 5% limit.

The fourth route is to convert the acquisition target into an LLC and then acquire 100% of it so that it is taxed as a disregarded entity and does not show up on your books as either “stock” or “partnership interest” (both of which are nonqualified financial property).

3. Don’t buy back stock

If you form a corporation that is a QOZB, avoid buying back any stock. There are numerous pitfalls if you buy back stock, and some will unavoidably wreck your tax advantages. If you reach a point where you reallyyyy want to buy back stock, then first read the precise rules about how to avoid problems in regulation CFR 1.1400Z2(d)-1.

Appendix B: Relevant Laws & Regulations

I provide this appendix as a reference source for use only if needed. I wouldn’t advise reading anything you don’t have to since the treasury decision document alone is over 500 pages.

Statutes:

- (26 U.S.C. 1400Z-1) Designation of opportunity zones

- (26 U.S.C. 1400Z-2) Special rules for capital gains invested in opportunity zones

- (26 U.S.C. 1397C) Requirements (2), (4), and (8) of subsection (b) must be met for a business to be a QOZB

- (26 U.S.C. 144) Subitem (c)(6)(B) lists “sin businesses” which are excluded from being QOZBs

Regulations:

- (26 CFR 1.1400Z2(a)-1) Definitions of various opportunity zone related terms, operational rules for determining eligibility & recognition of gains, special rules for various situations (including how OZ rules interact with tax rules for corporate reorganizations), and general rules of capital gains tax deferrment, reduction, and elimination

- (26 CFR 1.1400Z2(b)-1) Rules for events do or do not trigger taxability of deferred capital gains, rules for holding periods, and special reporting requirements applicable to direct and indirect owners of QOF partnerships

- (26 CFR 1.1400Z2(c)-1) Rules for resetting the basis of QOF investments held for at least 10 years

- (26 CFR 1.1400Z2(d)-1) Qualified opportunity funds & qualified opportunity zone businesses

- (26 CFR 1.1400Z2(d)-2) Qualified opportunity zone business property

- (26 CFR 1.1400Z2(f)-1) Various administrative rules such as anti-abuse rules, penalties, etc

IRS forms & instructions:

- (Form 8996 Instructions) Qualified Opportunity Fund form instructions

- (Form 8996) QOF form

Treasury Decisions:

- (TD 9889) Final regulations regarding opportunity zones, QOZBs, QOFs, investments in QOFs, and related issues

Revenue Rulings:

- (Rev. Rul. 2011-24) IRS precedent for determining when a service contract may be considered a lease