Last week, I talked to a guy who owns several truck stops, a diesel fuel wholesaling company, and a portfolio of industrial real estate. He told me that he could buy truck parking lots and rent them at a cap rate of 8% per year… in New Jersey! That’s a better return than I can get on single family rentals in south Florida, and with none of the property maintenance headaches (he’s literally renting out land).

I went down the rabbit hole and discovered 3 things:

The vast majority of trucking parking lots in the U.S. are small (1-5 acre) lots that are owned by mom and pop investors,

There is rapidly growing institutional interest in buying truck parking lots, and

Institutions are having difficulty investing in truck parking lots because the market is so fragmented and there are very few large portfolios available for them to buy.

I immediately start daydreaming about rolling up small truck parking lots at high cap rates, bundling them together, and then selling them off as a lower cap rate portfolio to some industrial REIT.

Since cities want the tax dollars from expensive properties, they tend not to approve the demolition of existing industrial buildings if there is no plan to replace them. That means the supply of land in dense urban areas is slowly being diminished, without replacement. So truck parking lots in large cities have a strong business moat & limited competition.

But my daydream gets even better. The average home insurance premium in Florida rose 42% from 2022 to 2023, and a similar story is true for commercial and industrial real estate in Florida. That means good real estate investments in Florida are hard to come by right now. Except… truck parking lots are not buildings… The cost of property insurance for these lots is minuscule compared to the revenue they bring in. You still need general liability insurance, but the cost of that insurance hasn’t been driven up by hurricanes, tornadoes, and roofing fraud to the same degree that the cost of property insurance has been.

So here’s the strategy:

Buy up small 1-5 acre parcels of industrial zoned land in Miami (these lots are too small for most brokers to care about and are frequently not listed on costar, which means there is serious potential to buy mispriced assets).

Choose land with easy access to nearby highways, the cargo port, the airport, and/or large distribution centers, since that is where the highest demand for truck parking is.

Also try to find land that is in the path of development so that when I’m ready to sell, I can stoke a bidding war between industrial REITS and industrial developers who want to buy the land.

Regrade the land if necessary, finish with gravel or pavement, and set up fences & cameras for security.

Rent out the land. Minimize vacancy by finding short term tenants on Truck Parking Club (basically Airbnb for truck parking) between my longer term tenants.

And in fact, my pool of potential tenants is actually much larger than just truckers. Construction companies need industrial land to store heavy equipment. Contractors need to store bulk materials. And logistics companies need to store shipping containers. That’s why institutional investors have started calling these industrial land parcels “industrial outdoor storage” (IOS) instead of truck parking lots. IOS is a $200 billion market in the U.S.

One major hiccup in the IOS roll-up strategy though is financing. Many banks won’t finance raw industrial land, especially if the land is not already generating cash flow. And rolling up enough lots to be interesting to an institutional investor would take tens of millions of dollars. That’s a lot of fundraising.

Also, because you don’t have to do much to turn land into a parking lot, it’s questionable whether an IOS roll-up could benefit from my favorite real estate tax strategy: opportunity zones. That’s a shame because a lot of industrial land in Miami is already in an opportunity zone.

Still, the combination of strong moat / limited competition, diminishing supply, increasing demand, low insurance costs, and lots of institutional buyers willing to buy a roll-up at a higher cap rate than I can buy individual lots makes the business of truck parking compelling enough for me to dig into more. Next week I’ll be publishing a podcast interview with the New Jersey truck stop owner I mentioned before, but if you happen to know anyone who owns IOS lots in Miami specifically, I’d love an introduction.

Santa undoubtedly learned how to deliver billions of packages around the world, by aircraft, in a single night, by emulating FedEx.

In 1971, Yale alumni Fred Smith founded FedEx with the goal of providing an end-to-end, air cargo delivery network for the U.S. To make the deliveries efficient, FedEx relied on a hub-and-spoke distribution system where all packages would be rapidly shifted among airplanes at one central airport each night. That meant the entire customer experience relied upon the FedEx night shift completing their job of shifting packages as quickly as possible. But for some time, they just couldn’t manage to do it — the night shift would rarely complete its mission on time.

FedEx’s management team tried changing the night shift’s processes, how packages would be stacked and organized during the shift, how packages would be loaded, what type of equipment was used to help move the packages, how packages were labeled and tracked — nothing worked. The management team appealed to the night shift’s sense of mission, but that didn’t work either.

Finally, a FedEx manager got the bright idea that it was counterproductive to pay the night shift by the hour when the company wasn’t trying to maximize billable hours but rather accomplish a specific task (shifting the packages among all the planes) as quickly as possible. So FedEx started paying the night shift employees on a per shift basis rather than a per-hour basis, and employees were allowed to go home when all the planes were loaded. And, overnight, FedEx’s night shift became a paragon of efficiency, and FedEx’s problem was solved.

“Incentives are superpowers… Never, ever, think about something else when you should be thinking about the power of incentives.”

Charlie Munger

For fun, here is a modern day example of an equally terrible incentive mistake that many companies are still making:

Many large tech companies compensate their engineering employees with stock options. Those stock options benefit underperforming employees the same as over-performing employees, which has several undesirable psychological consequences that impact the company’s bottom line:

Employees don’t “feel” a direct connection between their performance and their compensation. The stock option is perceived as part salary and part casino winnings, rather than as compensation that depends on the employee’s actual quality of work.

The highest performing employees can feel that they are not being compensated fairly, since their compensation is tied to the same stock performance as the worst performing employees.

Stock options are supposed to create loyalty from employees. However, in a bull market, they can have the opposite effect. Employees can get rich quickly even if they haven’t provided significant value, and then retire early, leaving the company shareholder’s worse off not only because the employee was compensated for more value than they provided but also because the company has lost an employee who must now be replaced.

In a bear market, stock options can become worthless even for highly productive employees. That can disincentivize a company’s most valuable employees and lead to some of them leaving to join other companies that offer stock options with lower strike prices for the current market.

What’s better than turning lead ($1 / lb) into gold ($22,000 / lb)?

Turning graphite ($10 / lb) into diamond (~$1 million / lb). And Howard Tracy Hall was the first person to invent a way to do that.

Howard monetized his invention by creating Hall Labs almost 70 years ago. Since then, Hall Labs has evolved into a conglomerate that is part industrial empire, part family office, and part venture studio. And I flew to Utah to interview the heir-patriarch & Chairman of the company.

Hall Labs owns a portfolio of almost 1,000 patents and has built and exited multiple $100+ million spin-offs. These spin-offs have large, patent-protected moats, and nearly all of them are also opportunity zone businesses which come with tax advantages for investors.

Hall’s biggest portfolio company is Vanderhall, an EV powersports company that is profitable after only $25 million of funding. Vanderhall is considering an IPO soon.

Hall’s biggest current bet is on built-to-rent apartment complexes that don’t have to connect to any public utilities.

Hall Labs is currently run by Howard Tracy’s son, Dave Hall. I interviewed Dave about how Hall Labs allocates money and people to different portfolio companies, how they raise money from opportunity zone investors, how they hire talented engineers on an hourly basis with no benefits, and why most startups purporting to solve the housing problem are bullshit. You can listen to my full interview here.

The IRS does not allow investors to directly 1031 exchange into a REIT, but you can indirectly 1031 into a REIT by first 1031 exchanging into a Delaware Statutory Trust (DST) which is already in the acquisition pipeline of a REIT and then later 721 exchanging your DST interest for ownership units in an UPREIT.

An UPREIT is an operating partnership owned by a REIT. That means technically, you still won’t own shares in a REIT. However, you get all of the same benefits because whenever you are ready to sell your REIT holdings, you can convert the UPREIT ownership units into REIT stock (usually 1-to-1) and then sell your new REIT shares in the liquid public markets.

In more detail, here’s how the process works, step by step:

Step 1: Do a 1031 exchange into a DST

Delaware Statutory Trusts (DSTs) are legally recognized trusts that typically manage the real estate of many investors, thereby allowing individuals to exchange their single property for an ownership interest in a much larger real estate portfolio without incurring any capital gains tax.

DSTs are like closed funds in that after they raise their initial capital, they do not raise any additional capital in the future. That means you’ll need to find a DST sponsor which is planning to create a DST but which hasn’t already collected a round of capital. There are sponsors who create a new DST every few months, so you shouldn’t have difficulty finding a DST that can accommodate you. The trick is to find one which offers a good deal after all the fees are accounted for.

Since your end goal is to hold a REIT investment, you’ll need to choose a DST which has a relationship with one or more REITs that could acquire it down the road.

After you find a DST that fits your needs, you can then do a 1031 exchange into the DST. DSTs do not file tax returns, and as such, you will report your share of the DST’s income on your personal tax return for as long as it takes the DST to be acquired by a REIT.

Step 2: The DST does a 721 exchange into an UPREIT

UPREIT stands for Umbrella Partnership Real Estate Investment Trust. An UPREIT is an operating partnership that owns and manages the real estate of a REIT and is itself owned by a REIT.

721 exchanges are the lesser known cousins of 1031 exchanges. In a 721 exchange, an investor contributes property to a partnership in exchange for an ownership stake in that partnership. Like a 1031 exchange, 721 exchanges are not taxable. However, to keep your tax deferral, you typically have to wait 2-3 years after 1031 exchanging into a DST before the DST will give you the option to convert your DST interest into ownership units in an UPREIT.

Step 3: When you want to exit, convert your UPREIT ownership units into REIT shares

REITs that operate through an UPREIT usually have identical investment returns whether you hold UPREIT ownership units or actual REIT stock. That means you can just hold the UPREIT units for as long as you want to invest in the REIT. If and when you eventually want to sell, you can easily convert your UPREIT units into REIT stock. If you chose a REIT which is publicly traded, you can then take advantage of the public market liquidity to sell your REIT shares.

It’s important to note that when you convert your UPREIT units to REIT shares, your deferred capital gains will be recognized, so it’s important to only do this once you are ready to sell.

The downside of 1031 exchanging into a REIT

The process outlined above can help you 1031 exchange into a REIT. This process can be very helpful if you need to sell (or have already sold) a property but can’t find a new property to 1031 exchange into. However, it also has downsides. After you convert your DST ownership interest into ownership units of an UPREIT, you can never go back. Your equity is now locked into the UPREIT, and the only way to get it out is to convert your UPREIT units into REIT shares which is a taxable event which you can’t 1031 your way out of since the IRS would deem the gain to be coming from the sale of a security interest in a partnership rather than from the sale of real property. It might still be worth it for you do a 1031 exchange into a REIT, but there are alternatives you should also consider before making a decision.

Alternative #1: Do a 1031 into a Delaware Statutory Trust

This was step 1 from above, and you can actually just stop here. Doing a 1031 into a DST helps you solve the problem of not being able to find a property to buy within the 1031 time window, while at the same time allowing you to do a future 1031 exchange on any gains (unlike a REIT or UPREIT).

DSTs have their own limitations, including:

DSTs are restricted from borrowing any new funds or renegotiating the terms of existing loans after they close, which can limit their ability to optimize their use of leverage, and

DSTs are not allowed to make capital calls or retain significant cash, which can put the real estate held by DSTs at risk in the event of financial crises or other serious market conditions.

Those limitations are manageable in some situations, but if you don’t like them, then there is another option.

Alternative #2: Invest into a Qualified Opportunity Fund (QOF)

Opportunity zones are specific census tracts that exist in every state. A qualified opportunity fund (QOF) is an LLC or other business entity which invests in real estate or businesses located in opportunity zones. If you invest capital gains into a QOF, then you can defer capital gains until 2027. That may sound much worse than a 1031 exchange (which allows you to defer capital gains indefinitely), but it’s actually better because of what comes next. You can hold an opportunity fund investment until 2046, and when you sell you don’t owe ANY capital gains tax. I’m not talking about a deferral of capital gains tax like a 1031. I’m talking about a permanent erasure of capital gains tax liability, as if Thanos snapped his fingers and made it disappear.

Opportunity zone funds are also very flexible. You can invest into an existing QOF or you can create your own QOF. If you create your own QOF, you can double the amount of time you have to acquire a property from the 6 months allowed by a 1031 up to 12 months or even more. For new construction projects, you can even qualify for 36+ months of total time to find and build your project!

And you aren’t even restricted to real estate with opportunity zones. You can actually invest in your own small business using a QOF. Most of the time, it’s even possible for you to invest in a QOF if you already have your funds locked up with a qualified 1031 custodian.

If you are trying to figure out how to avoid a big capital gains tax bill using a 1031 exchange, DST, or QOF, email me your questions through the form below. Unlike most forms on the internet, this one guarantees a response from an actual person with deep financial and tax knowledge.

How to Make 52% Profit Margins by Renting Chickens

“The standard package includes a 6 month rental of 2 chickens and a chicken coop for $485. After delivery and other expenses, the gross profit margin is 39%. And that’s just for the standard package. For the Deluxe package, the gross margin is over 52%.”

Phil Tompkins left a 20 year career in IT to look for a home-based business idea he could start with his wife, Jenn. The idea he ended up with was renting chickens to rich urban hipsters. Here’s what the standard offering included:

1 copy of the book “Fresh Eggs Daily: Raising Happy, Healthy Chickens Naturally” sent to the customer in advance of chicken delivery

2 hens, a chicken coop with water and food bowls, and 100 pounds of chicken food — all delivered anywhere within 50 miles of Phil and Jenn’s home

6 months of time with the chickens

Pickup of the hens and coop at the end of the 6 month rental period

The cost of that “standard package” is $485, and the couple called their new business “Rent-The-Chicken”.

How did Rent-The-Chicken get customers?

Initially, Phil and Jenn struggled to find anyone who would rent chickens from them. However, after persuading one friend to rent a chicken for free as a test, a local newspaper one county over heard about the business and contacted the husband and wife entrepreneurs for an interview.

At the time, the company did not even have a logo, but the newspaper ran the story over a holiday weekend, and it went viral. It was picked up by the Associated Press, and the couple was then invited to do video interviews, radio interviews, podcast interviews, blog interviews, and more newspaper interviews. That was the late summer and fall of 2013, and the wave of media publicity brought in a wave of customer orders.

However, the chicken entrepreneurs soon discovered that their initial idea about who would be their ideal customers (rich urban hipsters) was completely wrong. The people who actually wanted to rent chickens were empty nesters (parents whose children have grown up and left home) and young families with parents who wanted to provide their kids with a fun, educational experience about where their food comes from.

The business now uses organic social (Facebook and Instagram) as its primary marketing strategy. Due to the novel & charming nature of the business, it also continues to get free news coverage periodically in mainstream TV, newspaper, and other media channels. Recent egg price inflation has also spurred a lot mainstream news stories about how you can rent a chicken to get your own eggs at home. Side note: those news stories are pure clickbait since the cost of renting chickens is several times higher than the cost of just buying 6-months worth of eggs at the grocery store, even after inflation.

What are the unit economics of renting out chickens?

Let’s break down the revenue, expenses, and profit margin for a single “standard package” chicken rental.

Below is a table summarizing the business expenses directly attributable to a single rental (excluding the cost of the hens and coops which are re-used).

Expense Item

Estimated Total Cost

Cost Estimate Justification

1 copy of the “Fresh Eggs Daily: Raising Happy, Health Chickens Naturally” book with shipping

$15

I found a copy of the book for $13.56 + $2.64 shipping ($16.21 total) on AbeBooks.

Since Phil and Jenn are sending a copy of the book with every order they make, they should be able to get books in bulk for a bit cheaper than that.

100 lbs chicken feed

$37

Tyrone Milling sells a 100 lb bag of chicken feed for $37

100 Mile (round-trip) delivery – vehicle costs

$63

The IRS posted a standard mileage rate (intended to reflect all costs associated with owning a vehicle, including gas, repairs, oil, insurance, registration, and depreciation) of $0.625/mile for the second half of 2022.

100 Mile (round-trip) delivery – labor costs

$45

The total loading, driving, and unloading time should be less than 3 hours to deliver to a destination within 50 miles of a farm (less than 100 miles round-trip).

Assuming an hourly worker is hired to drive, the cost per hour should be less than $15 in most markets. That makes 3 hours of time cost $45.

100 Mile (round-trip) pickup – vehicle costs

$63

100 Mile (round-trip) pickup – labor costs

$45

Unit Expenses (excluding hens & coop)

$268

n/a

In reality, Phil delivers the chickens himself so there are no labor costs per se. However, if you wanted to start your own chicken rental business, you could easily hire someone to take on that duty which is why I included labor costs for delivery in the list of expenses above.

The capital expenditures (capex) for a single rental set-up are summarized in the next table:

Capex Item

Estimated Total Cost

Cost Estimate Justification

Chicken coop

$100

I found a reference chicken coop on Amazon selling for $150, and the coops shown in the pictures on the RentTheChicken.com look simpler and cheaper. Even the upgraded “Deluxe coop” offered by Phil and Jenn appears to be something that could easily be made for under $100.

2 hens

$40

Hens can be purchased in bulk for $20 each

Unit Startup Capex

$140

n/a

Commercial egg-laying hens are typically kept for 2-3 years because after that, egg and shell quality decline. That means a hen can probably be rented out for about five 6-month stints before being retired. It’s also reasonable to assume that a chicken coup will last for at least as long. That means our total unit expense should include a depreciation expense worth 1/5 the unit startup capex amount. This is summarized in the next table.

Financial Metric

Amount

Revenue

$485

– Operating Expenses (excluding hens & coop)

$268

– Depreciation of hens & coop (assuming each is rented 5 times)

$28

Total Cost of Goods Sold (COGS)

$296

Gross Profit

$189

Gross Profit Margin

39.0%

A gross profit margin of 39% is already good, but there are several reasons why the actual gross margin could be even higher:

Not every customer will actually be 50 miles away. Some will be closer. That would reduce delivery and pickup costs which account for $216 of the $296 COGS (73%). If we consider a circle with a 50 mile radius, the average distance to a point in that circle will be 33 miles. That means if customers are uniformly distributed over the service area, the true unit transportation cost might be closer to $144 rather than $216. That would imply a gross profit margin of 53.8%.

Multiple customer deliveries and/or pickups could be scheduled for the same day, cutting down on transportation costs.

A more fuel-efficient, lower-maintenance vehicle could be used for deliveries and pickups, cutting down on transportation costs. Remember, we just used the IRS’s average vehicle number, so there is substantial room for achieving lower transportation costs by choosing the right vehicle.

Manufacturing of coops could be optimized, reducing the cost per coop.

Coops might last longer than the 5 uses anticipated by our model. If they don’t currently last longer, they could be manufactured more durably so that they do.

Additionally, all of this is just for the “standard package”. Rent-The-Chicken also offers a “standard upgrade” package and a “Deluxe” package, both of which have higher margins.

The Deluxe package sells for $685. It comes with 4 hens and 200 pounds of chicken feed, with everything else the same as the standard package. Total COGS (cost of goods sold) is $341 which means gross profit is $344, and the gross profit margin is 50.2%.

Or, if we use our assumption that the average customer is located 33 miles away rather than 50 miles away, then the COGS for the Deluxe package is $269, the gross profit is $416, and the gross profit margin is 60.7% (about the same as Amazon AWS).

Franchising

Rent-The-Chicken has expanded across the U.S. and into Canada through a franchising business model. Franchisees (called “affiliates” on RentTheChicken.com) are small farmers and homesteaders who rent out chickens and coops under the “Rent-The-Chicken” brand in exchange for a 10% royalty on sales. The map below shows the location of all current franchisees.

Intellectual property royalties are essentially 100% gross profit, which makes franchising an amazing business model. In exchange for those royalties, Rent-The-Chicken also handles marketing and customer service. However, given the limited amount of marketing conducted by Rent-The-Chicken (basically just organic social), I estimate the net profit margin of their franchising business (after all expenses except taxes) would still be over 90% even if you replaced Jenn’s marketing and customer support roles with paid employees.

By the way, if you enjoy learning about interesting business models like chicken rentals and chicken rental franchises, subscribe to my free newsletter to get more content like this on a weekly basis.

Appendix A: Growing profits with location-based pricing

Once Rent-The-Chicken was franchised into different markets, the number of package options and the pricing of those options was modified to reflect the different buying power in different markets. For anyone running a business across multiple geographic locations, this type of price optimization is one of the easiest ways to increase your profitability.

The table below shows how Rent-The-Chicken set prices for each U.S. franchisee’s location.

Location

Standard Package

Standard Upgrade Package

Deluxe Package

Eglu Go Up Package

Out of Area Package

Phoenix, AZ

$825

$925

$1025

—

—

Tucson, AZ

$485

$585

$685

—

—

Los Angeles, CA (zone 1)

—

$585

$685

—

—

Los Angeles, CA (zone 2)

—

$615

$715

—

—

Los Angeles, CA (zone 3)

—

$645

$745

—

—

Connecticut

$485

$585

$685

$885

—

Philadelphia, PA

$635

$735

$835

—

—

Athens, GA

$485

$585

$685

—

—

Atlanta, GA

$585

$685

$785

—

—

Chicago, IL

$995

$1095

$1195

$1395

—

South Bend, IN

$495

$595

$695

$895

—

Omaha, NE

$485

$585

$685

$885

—

Sioux City, IA

$595

$695

$845

—

—

Baltimore, MD

$485

$585

$685

$885

—

Boston, MA

—

$595

$735

—

—

southern New Hampshire

—

$595

$735

—

—

New Jersey

—

$585

$685

$885

—

Albany, NY

$665

$765

$815

$1065

—

Syracuse, NY

$485

$585

$685

$885

—

Finger Lakes Region, NY

$585

$685

$785

$945

—

Long Island, NY

—

—

$1185*

—

—

Rochester, NY

$585

$685

$785

$985

—

Raleigh, NC

$485

$585

$685

$885

—

Columbus, OH

$485

$585

$685

—

—

Cleveland, OH

$535

$635

$785

—

—

Harrisburg, PA

$485

$585

$685

—

—

Gettysburg, PA

$485

$585

$685

—

—

Laurel Highlands, PA

$485

$585

$685

$885

—

Pittsburgh, PA

$485

$585

$685

$885

—

South Carolina

—

—

—

—

$1350

Florida

—

—

—

—

$1350

Middle Tennessee

$485

$585

$685

$885

—

Austin, TX

$735

$835

$985

—

—

College Station, TX

$535

$635

$785

—

—

Dallas, TX

$665

$765

$915

—

—

Houston, TX

$665

$765

$915

—

—

Burlington, VT

—

$685

$785

—

—

St Johnsbury, VT

—

$585

$685

—

—

Winchester, VA

$485

$585

$685

$885

—

*The Long Island package includes less food than the typical Deluxe package (only 100 lbs for 4 chickens)

Appendix B: Farmer Brad Chicken Rentals

Rent-The-Chicken is not the only chicken rental business that exists. Another is “Farmer Brad Chicken Rentals”. Farmer Brad’s chicken rental prices are provided in the table below.

Basic Chicken Package (2 hens)

Deluxe Chicken Package (4 hens)

Bantam Rental

3 month rental

$300

$450

n/a

6 month rental

$450

$600

$200

Buyout

$350 (3 month buyout)

$300 (6 month buyout)

$325 (3 month buyout)

$300 (6 month buyout)

$200

Appendix C: Hatch-The-Chicken

Rent-The-Chicken has started growing their business through additional types of animal experiences beyond renting egg-laying chickens. They now also offer a “Hatch-The-Chicken” experience where they rent you a mini incubator for 5 weeks, provide you with 7 fertile eggs to hatch, and then come pick up the hatchlings at the end of the 5-week period. They offer this service for $210 (which is another reason I suspect the unit transportation costs on their main chicken rental business are lower than the $216 estimate I used earlier in this article).

Like the original “Rent-The-Chicken” product, “Hatch-The-Chicken” has many young families as customers. However, Hatch-The-Chicken has also generated significant institutional demand. It is being sold with much success to daycare providers, preschools, private elementary schools, summer camps, and senior living facilities.

Rent-The-Chicken cofounders Phil and Jenn have also mentioned on a podcast that they were planning to launch a “Hatch-The-Duck” product, but do not appear to have actually done so yet. That could be an opportunity for you to launch your own business in that niche.

It costs $9,900 to die in the United States. That’s the national median funeral cost including burial in 2022.

For that price, you get a $2,500 casket, a $2,000 burial plot, $775 of embalming services, and $4,625 of miscellaneous fees that are mostly hot air. Since hot air has great margins and since the death rate isn’t reduced by recessions, funeral homes might seem like the perfect recession-proof business. In this article, I’m going to explain why they aren’t, but I’ll also tell you about two other death care businesses that are.

Why aren’t funeral homes recession-proof businesses?

Funeral homes make most of their money by selling caskets, transporting bodies, embalming & other “cosmetic body prep” services. If the funeral home owns the cemetery, it will also make money on selling you a grave plot, grave digging services, and a headstone.

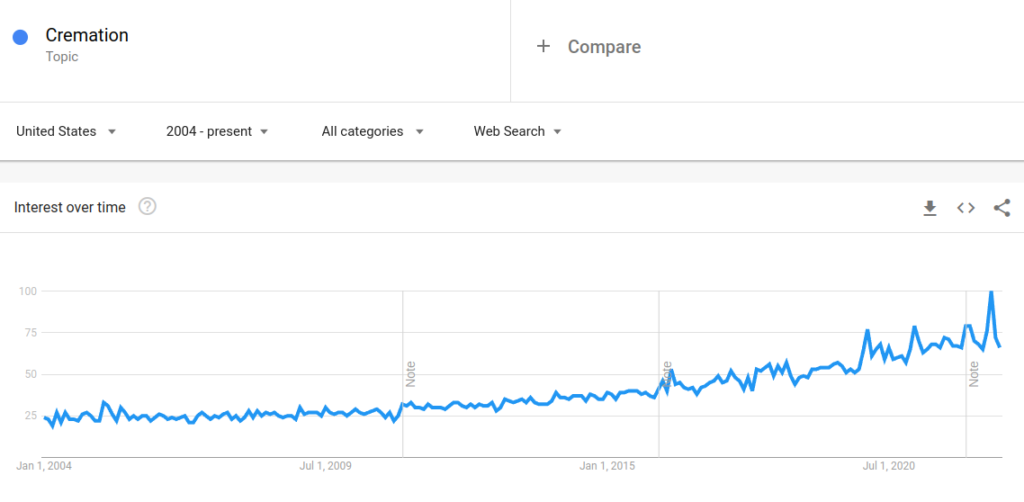

All those big money makers are dependent on people getting buried. Unfortunately, burials have been consistently losing market share to cremations almost every year for the past several decades. In 2006, 33.8% of people who died in the U.S. were cremated. In 2011, 42% were cremated. In 2016, 50.1% were cremated. In 2021, 57.5% were cremated.

There are three main reasons for this ongoing shift in American consumer preferences.

Cremation is cheaper than burial.

There is less religious stigma against cremation today than there was 30 years ago. This is partly because some religions like Catholicism have embraced cremation as acceptable within the last few decades. It is also partly because a smaller percentage of Americans are religious today than were religious 30 years ago.

Americans care more about environmental sustainability today than they did 30 years ago, and burials have a higher environmental cost than cremations.

As cremations continue to chew into the market share of burials, profit margins of funeral homes go down. That poses a headwind to the entire industry that will likely continue for decades.

To make matters worse (for the funeral industry), more and more Americans are opting for non-traditional “wakes” or “life celebrations” at home rather than somber, multi-hour ceremonies at funeral homes that charge a high hourly rate to use their space. This poses a second significant headwind to funeral home businesses.

Finally, a third headwind exists for funeral homes that own cemeteries with lots of unused plots. The decreasing rate of burials means that cemetery plots can stay empty for longer periods of time, and some may never be filled at all. Yet it’s difficult to sell unused parts of cemeteries, and if you can sell them at all it will be at a steep discount to other real estate nearby. That means many funeral homes are stuck with real estate assets that aren’t generating any income which brings down their rate of return-on-assets.

Fortunately, we’ve already seen an industry with all of the recession-resistance and none of the headwinds of funeral homes.

The economics of crematoriums

A crematorium is a body-disposal facility. Some are owned by funeral homes while others are independently operated and contract their services to one or more funeral homes. Given the headwind to on-site funeral home ceremonies discussed earlier, the best type of crematorium to start today would be a small facility which focused purely on cremations without taking on the overhead of large real estate spaces.

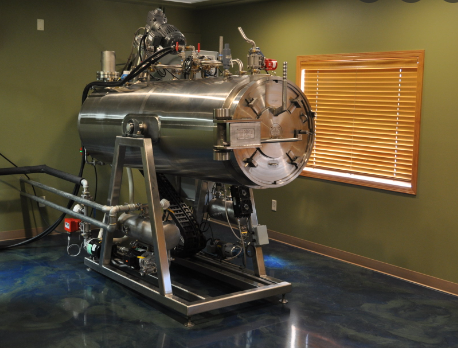

Alibaba currently has cremation machines (shown above) for sale for $45,000 plus shipping. You’ll also need a facility with appropriate ventilation for the fumes created by the machine.

Crematoriums are regulated at the state level, and most states will require that the individual operating a crematorium have a funeral directors license.

Crematoriums have a strong industry tailwind from the increasing popularity of cremation. Crematoriums are also incredibly recession-proof for two reasons:

Overall death rate does not decrease during recessions.

Cremation is cheaper than burial, so financially distressed families are even more likely to choose cremation than burial during recessions.

However, one of the current industry tailwinds of cremation has the potential to flip into a headwind: Environmentalism.

Cremations DO have a lower environmental cost than traditional burials. However, they still emit about as much CO2 as a 600 mile car trip, they are energy-intensive, and they can release toxic air pollution from the mercury in some dental fillings. That means that there is potential for a public backlash against cremations in the future. Additionally, some local governments have already temporarily suspended crematoriums’ ability to operate during times when air pollution is particularly bad. Fortunately, there is an newer alternative option: liquid cremation.

Liquid cremation: the perfect recession-proof business

Liquid cremation, wet cremation, water cremation, aquamation, flameless cremation, resomation, alkaline hydrolysis — these are all the same thing: Dissolving bodies in a 5% solution of potassium hydroxide at between 200-300 degrees Fahrenheit.

The process decomposes a body into a non-toxic solution of amino acids that can be processed by municipal water supply systems. I.e. it’s safe to dump the resulting liquid down the drain.

Metal implants are left intact and can be recycled. Bones are also left behind and can be ground into powder which is then returned to families in place of ashes from a traditional cremation.

Liquid cremation is completely sterile. The alkaline solution kills any pathogens and sterilizes the bones. That means there is no risk of diseases contaminating a water supply as there is with unembalmed burials. There is also no risk of carcinogenic embalming fluids contaminating a water supply as there is with embalmed burials. In fact, liquid cremation might be the best possible body disposal method because it is both highly sterile and very environmentally friendly. When compared against traditional cremation, three of the biggest environmental benefits are:

Liquid cremation requires only 10-15% of the energy used by traditional cremation.

Liquid cremation does not require combustion. All energy requirements can be met by cleanly produced electricity.

Liquid cremation produces zero gaseous emissions. (In contrast, traditional cremations release CO2, carbon monoxide, mercury, or other combustion byproducts).

In addition to the environmental benefits, it takes the same amount of time to perform a liquid cremation as a traditional cremation. The cost to perform a liquid cremation can also be less than a traditional cremation, especially if energy prices are high.

How to start a liquid cremation business

Starting a liquid cremation business is in many ways easier than starting a traditional cremation business. Liquid cremation is still a new concept, and there are many fewer competitors offering the service (but Google search trends still show a growing interest in liquid cremation over the years). The machines required are also smaller & lighter than traditional cremation machines. However, since liquid cremation is so new, there are fewer suppliers so the machine are still more expensive ($150k-400k for a human-sized machine or around $60k for a pet sized aquamation machine).

If you’re an engineer, then selling glorified steel drums for hundreds of thousands of dollars is a business opportunity worth considering in itself. If you’re not an engineer, you can still start a liquid cremation business without a ton of money by either financing or leasing an aquamation machine.

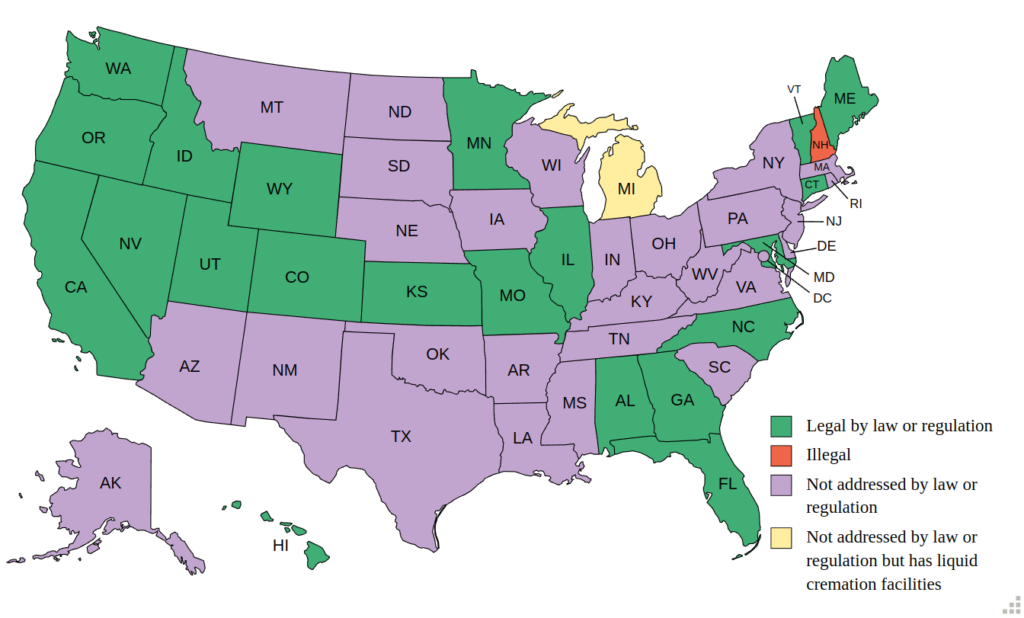

When deciding on where to locate your business, you’ll have to consider the legal landscape. Twenty-one states have currently legalized liquid cremation, one state has made it illegal, and the remaining twenty-eight states are legally ambiguous with no law or regulation explicitly addressing the topic. The trend in general though is towards more and more states adding explicit provisions to legalize the process.

Liquid cremation for pets however is legal in every state.

“That’s a pretty interesting result to anyone running a hedged long/short investment portfolio, especially with energy prices so high. It also means that if I personally held any private stock in Crypto.com, I’d be looking to offload it as quickly as possible since its stadium deal structure didn’t meet our “high-quality deal criteria”.

American Airlines Arena before its rebrand to FTX Arena in 2021

In January 2021, the fintech company “Q2 Holdings, Inc.” agreed to pay an estimated $26 million to name a Texas major league soccer stadium “Q2 Stadium”. That was just the beginning of what became a record-setting year for stadium name deals. Some of the largest deals included:

Intuit buying the naming rights to the L.A. Clippers’ new arena for $500 million

FTX buying the naming rights to the Miami Heat’s home arena for $135 million

Crypto.com buying the naming rights to the L.A. Lakers’ home arena for $700 million

These companies are willing to shell out massive piles of cash in order to build their brand and market themselves as important, trustworthy companies. However, given the massive size of the expenditures, it’s worth the time of any investor, executive, or board member of one of these companies to quantitatively estimate the ROI. In this article, I do exactly that by pulling data from SEC filings, historical stock performance, local government records of cities that have stadiums, company announcements, and media coverage of sponsorship deals. By the end of this article, you will know:

How companies that bought stadium naming rights in the past have performed relative to their competitors and the overall market.

How to know if you should sell a company that announces a naming rights purchase.

How to decide whether a company you run or advise should buy the naming rights to a sports venue (e.g. high school stadium, college stadium, major league stadium, etc).

Let’s jump in.

What do you actually get when you buy “naming rights”?

A naming rights deal is about intangible assets. A typical deal might include the sale of something like this list of assets:

The right to specify the name of the stadium

The right to have your chosen stadium name and/or your company logo written up to a certain size on various parts of the stadium’s exterior (e.g. the roof and/or over the main entrance)

The right to various signage throughout the interior and exterior of the stadium for use as advertisements

The right to advertise your company as “the official provider of <thing or service> to <name of team that uses the stadium>”

The right to have certain parts of the stadium painted and/or lit with your company’s colors

The right to have the stadium name used in all official press releases of the stadium’s home team

The right to have the in-game announcer say the stadium name and/or other sponsored messages about your company a certain number of times throughout every home game

The right to have your company logo and/or name on the backdrop of certain press conferences held at the stadium

The right to exclude anyone else from advertising on or within certain parts of the stadium

Discounted options on buying certain TV commercial slots during televised games

The right to use certain retail or vendor spots within the stadium and/or adjacent buildings

The right to exclude competitor companies from advertising in the stadium and/or adjacent buildings

Of course, deals will differ from one to another, but that list gives a pretty good idea of the type of assets that are often included in a naming rights purchase agreement.

How stadium name deals are structured

With rare exceptions, stadium names are not paid for with a single lump sum. Instead, the headline dollar amount (e.g. “SoFi buys stadium naming rights for $625 million”) is actually paid in quarterly installments over the course of decades. For instance, SoFi’s purchase will be paid over the course of 20 years.

Equally important to know is that despite these deals being referred to as “purchases”, naming rights are almost never actually purchased — they are rented. Returning to the example of SoFi, the “purchase” agreement is actually an agreement for the stadium to have the name “SoFi Stadium” for 20 years (i.e. the same length of time that SoFi is making payments). In other words, SoFi agreed to rent the intangible asset of “naming rights” for the L.A. stadium for about $30 million per year, for 20 years. That is a hefty subtraction of free cash flow for a very long time. And as anyone who has owned a business knows, free cash flow is the lifeblood of a company.

To accept that kind of rigid constraint, you better be damn sure that the ROI you’ll get will be substantially better than what you’d get from instead using an elastic marketing budget on digital ads. If a $30 million Facebook ad campaign doesn’t work, you can shut it off in a day and only lose $82,000. If a $30 million stadium marketing campaign doesn’t work, you’re stuck with not just $30 million this year but also for the next 19 years. That’s a lot of risk which can meaningfully degrade a company’s long-term performance if taken recklessly. However, an even more significant consideration is that how a company’s management team makes one $100M+ budget decision reflects on how they make all decisions. If stadium names don’t provide a good ROI, then a company that buys them probably makes lots of other bad purchases too. If stadium names *do* provide a good ROI, then a company that buys them probably has good decision making processes in place, which means they’re likely to make other good decisions as well. To figure out which situation is more likely, let’s take a look at the historical ROI of some companies that have bought stadium naming rights in the past.

These companies were randomly sampled from the set of publicly traded U.S. companies which are current or recently terminated sponsors of NFL stadiums, have been public for the majority of the deal duration, and have been involved in the deal for at least 5 years. The time window over which each company is analyzed starts briefly before major news coverage of the deal began. The time windows all end in 2022. The stock performance of each company (adjusted for any splits and dividends) is compared against various benchmarks such as the S&P 500, a subset of closest competitors, and same-sector ETFs which have existed throughout the entire time window under study.

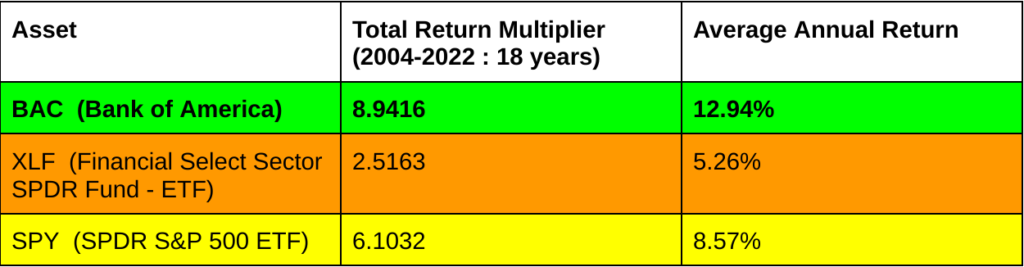

Case Study 1: Bank of America

VERDICT: Overperformed

Substantially outperformed S&P 500

Substantially outperformed sector ETF

On first look, it appears that Bank of America must have had great managers with great judgement about where to spend money. How else could they have performed so much better than both a financial sector ETF and the S&P 500 for almost two decades?

However, as you read through the next few case studies, you might start to wonder (as I did) whether Bank of America’s performance might not be as good as it first appears. The most obvious potential source of bias is the fact that the time period of our study includes the financial crisis. During the financial crisis, the federal government gave billions of dollars of assistance to Bank of America and certain other large banks. Not every company included in the XLF financial sector ETF received the same level of assistance. The discrepancy is even larger if we compare against the companies in SPY. To investigate this possibility, let’s re-run our analysis but this time just over the period after the financial crisis.

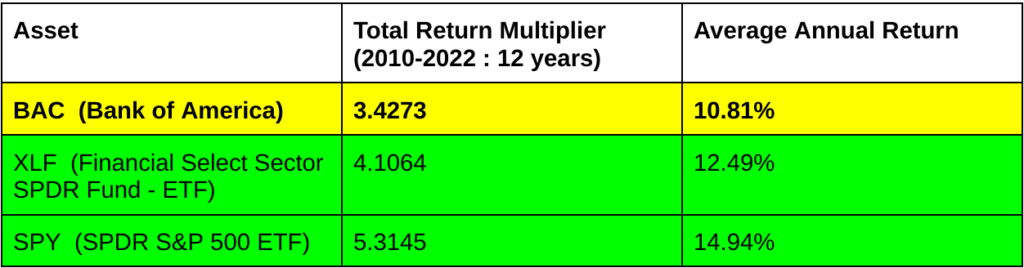

Case Study 1A: Bank of America (Post-Bailout)

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed sector ETF

These results are quite different from what we had before. This time, Bank of America’s stock noticeably underperformed both the financial sector specifically and the larger stock market in general. This isn’t enough data to definitively say that Bank of America’s overperformance measured in our first case study was entirely due to special treatment by the government. However, that explanation does seem entirely possible given the systematic underperformance after the special treatment was over.

Case Study 2: FedEx

*Note: UPS is a close competitor of FedEx but is omitted from comparison because it had not yet IPO’d at the time this comparison starts.

VERDICT: Underperformed

Moderate to substantial underperformance of most competitors

Similar performance to XLI (not the best comparison ETF, but the closest available that existed for the full length of the study)

Similar performance to S&P 500

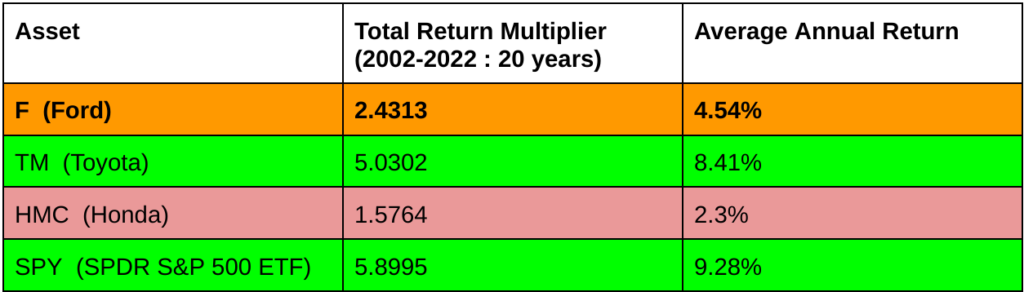

Case Study 3: Ford Motor Company

VERDICT: Underperformed

Substantial underperformance of S&P 500

Mixed performance relative to competitors

It’s hard to compare Ford to direct competitors since many competitors either have not been publicly traded since 2002, are foreign companies (and hence excluded from this study in an attempt to provide a more apples-to-apples comparison), have undergone substantial mergers or restructuring events, and/or also sponsor major league sports venues. However, despite those issues, it’s still clear that Ford has not performed well over the past two decades.

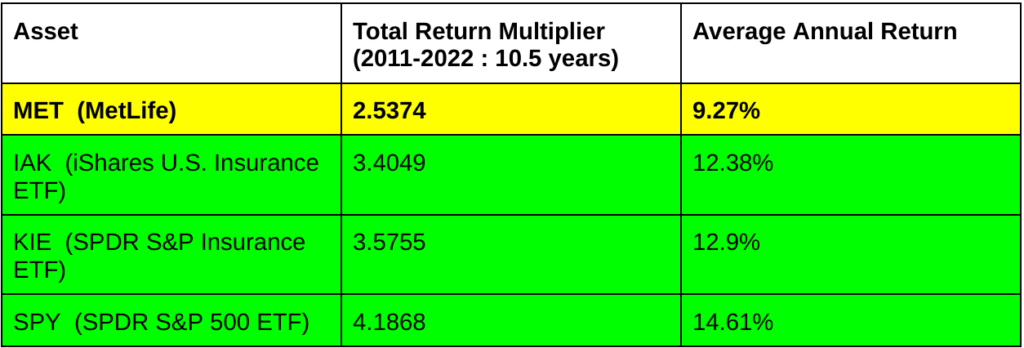

Case Study 4: MetLife

VERDICT: Underperformed

Substantial underperformance of S&P 500

Moderate underperformance of insurance sector ETFs

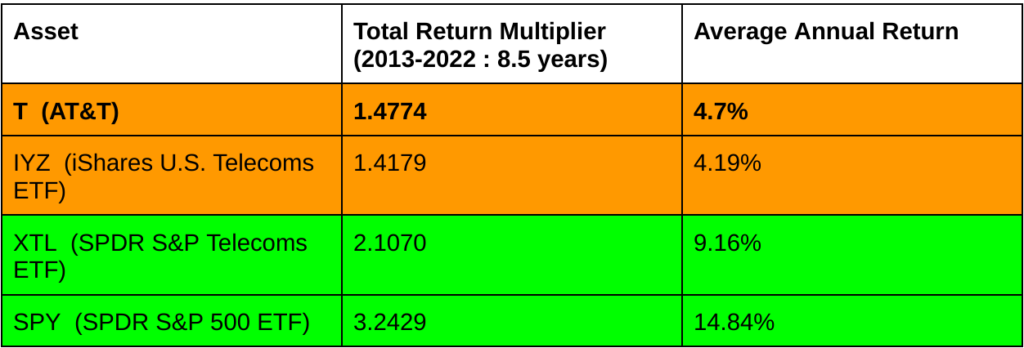

Case Study 5: AT&T

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed sector ETFs on average

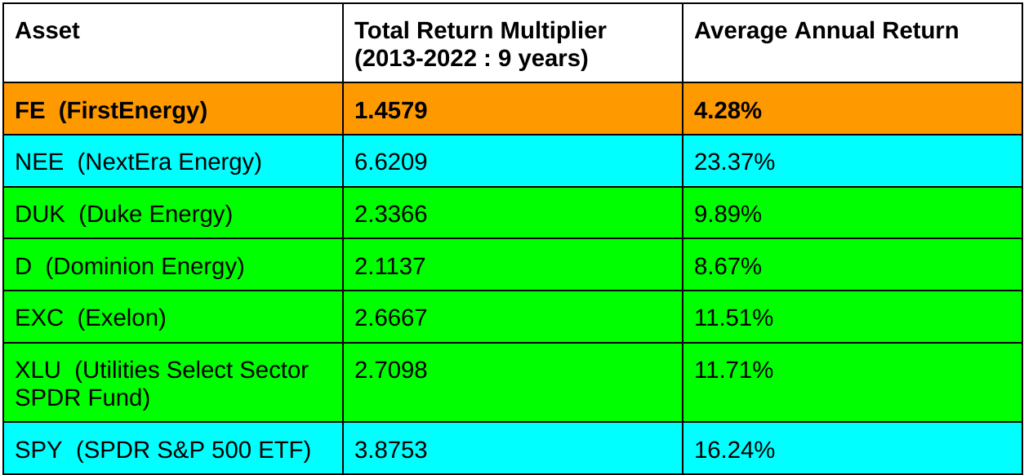

Case Study 6: FirstEnergy Corp

VERDICT: Underperformed

Substantial underperformance of S&P 500

Substantial underperformance of competitors

Substantial underperformance of sector ETF

It’s worth noting also that as of 2022, FirstEnergy is involved in serious legal issues after it came out that the company had spent $64 million dollars bribing state government officials. There seems to be a pattern of energy companies that sponsor major league stadiums getting involved in scandals. For a brief period, the Astros baseball team played their home games in “Enron Field”. Chesapeake Energy also put their name on an Oklahoma NBA arena before it later become involved in a price-fixing scandal. In fact, if you take away just one thing from this article, it should be to never buy stock in energy companies with their names on stadiums. And if you run a hedge fund, you might consider them as short positions against an energy-heavy portfolio. (To access my complete model & analysis for such a strategy, subscribe to Axiom Alpha Market Intelligence and I’ll include it with the next issue).

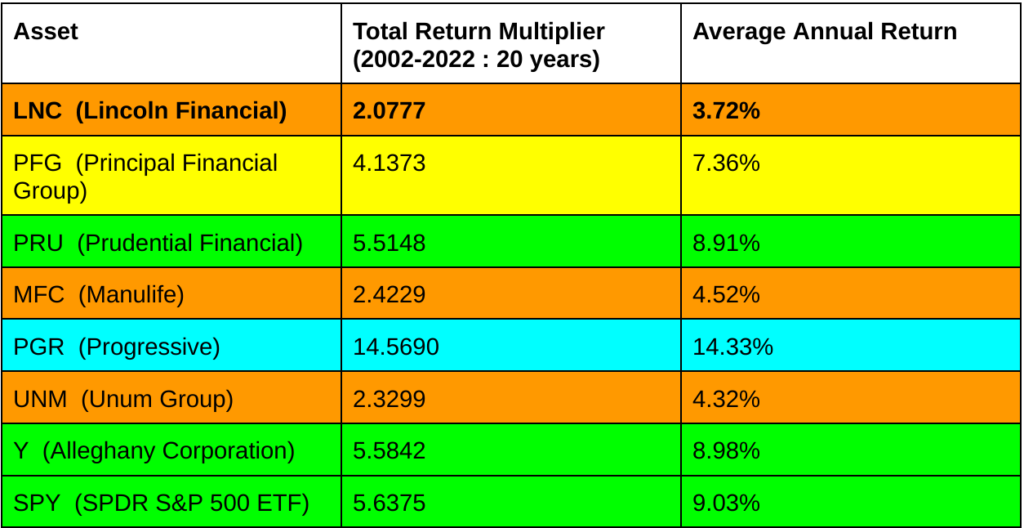

Case Study 7: Lincoln Financial

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed every competitor analyzed (many substantially)

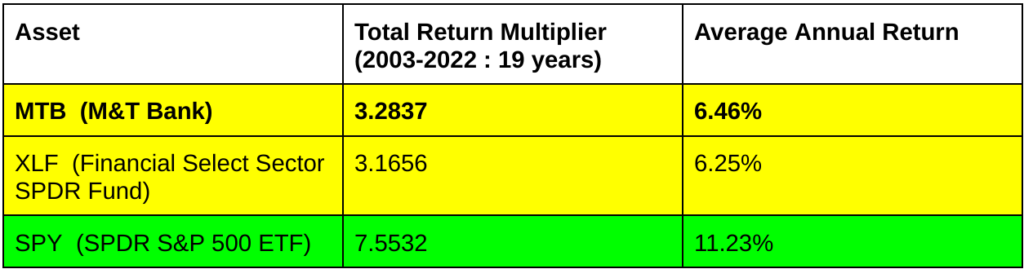

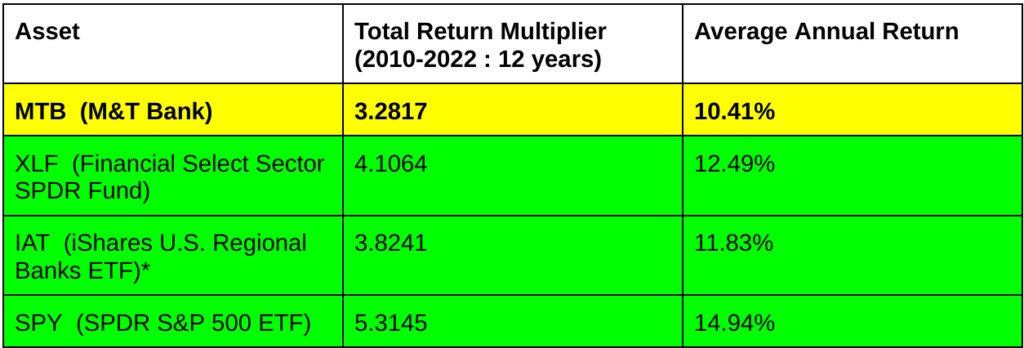

Case Study 8: M&T Bank

VERDICT: Underperformed

Substantial underperformance of S&P 500

Similar performance to sector ETF (even though M&T Bank got a government bailout during the 2008 crisis and not every company in the ETF did)

Unlike the situation we saw earlier with Bank of America, M&T Bank underperformed the S&P 500 even over a time window that includes the financial crisis. However, they still appear to perform similarly to the financial sector as a whole. Given that M&T also received more government assistance than your average finance company though, we have another opportunity to test our hypothesis. If stadium names are in fact generally bad purchases, then when we re-run our analysis for the period after the financial crisis, we should expect to see MTB flip to substantial underperformance relative to XLF. Let’s test.

Case Study 8A: M&T Bank (Post-Bailout)

Exactly as expected, MTB consistently underperformed both the finance industry specifically and the market generally after the financial crisis. I even included another bank-specific ETF here (which wasn’t included in the previous comparison since it didn’t exist in 2003). MTB also underperformed that bank-specific ETF.

VERDICT: Underperformed

Substantial underperformance of S&P 500

Underperformed sector ETFs

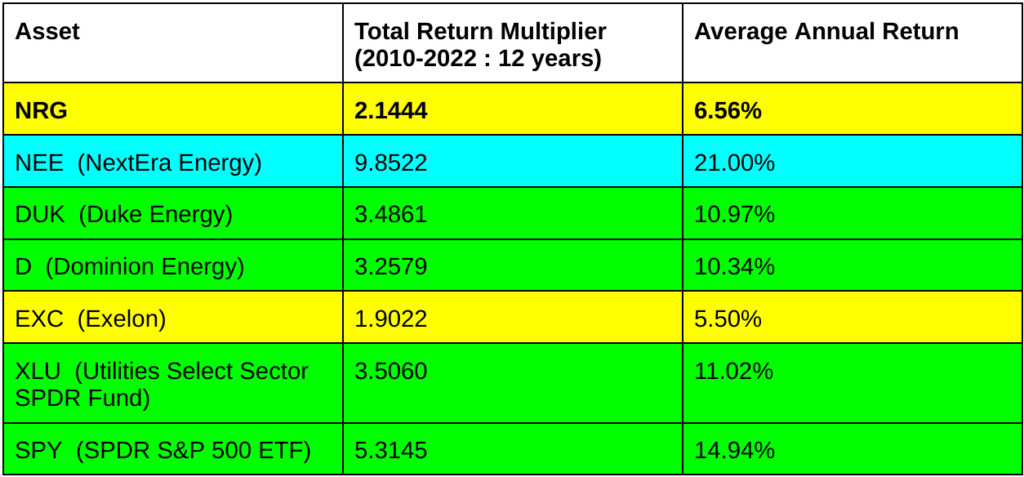

Case Study 9: NRG

NRG is an energy company with its name on a stadium, so you already know what to expect from our previous discussion.

VERDICT: Underperformed

Substantial underperformance of S&P 500

Substantial underperformance of most competitors

Substantial underperformance of sector ETF

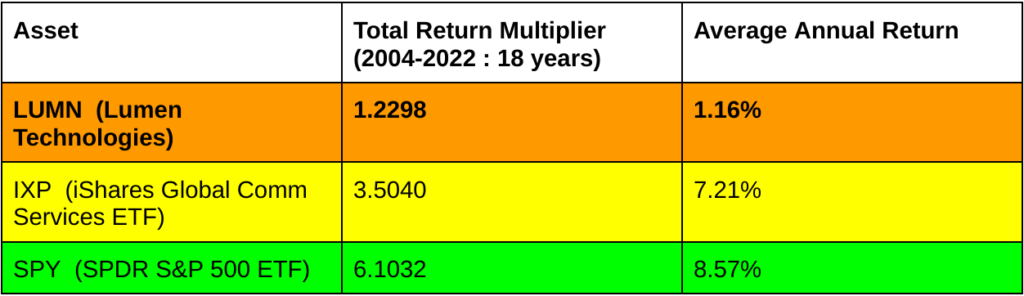

Case Study 10: Lumen Technologies

To accurately analyze Lumen Technologies, we have to account for several events. In 2002, a new stadium opened in Seattle with the name “Seahawks Stadium”. In 2004, Qwest Communications International bought the naming rights to the stadium which was renamed “Qwest Field”. In 2011, the stadium was rebranded to “CenturyLink Field” after Qwest was acquired by CenturyLink. In 2017, the company extended their naming agreement until 2033. Then in 2020, the stadium was rebranded to “Lumen Field” after CenturyLink restructured into three entities: Lumen Technologies, CenturyLink, and Quantum Fiber.

Ordinarily, I wouldn’t include a company that went through so many restructuring events because even if you can adjust stock prices accurately, you don’t know whether the merger event changed the management style. For example, Proctor & Gamble have been excluded because after they acquired Gillette, the new top level management did not clearly signal agreement with the original Gillette management’s decision to invest in the naming of Gillette stadium. In contrast, after each of the events Lumen and its predecessors was involved in, the post-event management team decided to reinvest additional dollars into the stadium sponsorship deal. For that reason, it seems fair to include them in our analysis. Here’s how they performed:

VERDICT: Underperformed

Substantial underperformance of S&P 500

Substantial underperformance of sector ETF

It’s also worth noting that in recent years Lumen has pivoted substantially into cloud and software more than its roots in telecom. If we were to compare them to their current competitors (which include companies like Microsoft and Oracle) rather than their historical competitors, their relative underperformance would have been even worse than it is in the chart above.

Total Return Statistics

Of the 10 companies we just analyzed, 9 underperformed a basic portfolio consisting of a 50/50 split allocation between their industry peers (represented as a sector ETF where one existed and by an equal weight index of direct competitors where one did not) and the S&P 500. Six of the companies underperformed the S&P 500 by more than 50%. Furthermore, if we adjust our analysis to only look at banks after they received financial assistance from the government, all 10 companies underperformed. That’s compelling, but not quite statistically significant. However, if we loosen our sampling criteria a bit, then we can look across a broader set of 98 publicly traded companies that bought naming rights for NFL, NBA, MLB, or NHL stadiums between 1973 and 2019. We stop in 2019 to avoid needing to analyze weird effects of massive government subsidies & fiscal stimulus during 2020 and 2021.

From this larger set of companies, two stand out for substantial overperformance: Qualcomm (QCOM) and Target (TGT). Given our earlier results being very subpar, it’s worth looking at what’s going on with these examples.

Qualcomm

Several things pop out of the details of Qualcomm’s agreement to purchase the naming rights to the San Diego Chargers’ stadium in 1997. The first is that Qualcomm paid a truly tiny sum ($18 million) for 20 years of naming rights. The second is that they paid this entire $18 million sum upfront rather than spreading it out over the duration of the agreement. The context for how this deal happened is that the city of San Diego was desperate for funding to finish an expansion of the stadium. Qualcomm stepped into the gap and got a 5-10x cheaper price than other companies paid around that time for similar name deals. In other words, Qualcomm didn’t go looking for a stadium naming deal. Instead, they acted opportunistically to seize an opportunity to make a deal with a desperate local government at a price that was only 10-20% of what other companies were paying for the same types of deals.

Target

Target has been very reluctant to release any financial information regarding their 1990 deal to name a Minneapolis NBA arena the “Target Center”. However, piecing together what we do know, it seems likely that the 25 year agreement carried a price tag of about $1-1.5 million per year. That’s about 25-50% of what companies were paying a decade later, adjusted for inflation, and just 10-20% of what companies were paying in 2021. Additionally, the Target agreement was deeper than just a name. The agreement also included provisions for certain NBA players to visit Target stores. Some basic modeling of retail customer behavior and attendance to NBA autograph events suggests that this provision alone might have been worth a substantial portion of the agreement. Target also hasn’t disclosed details about specific merchandise partnerships, but it’s quite possible that Target may also get a direct benefit in terms of discounts and/or exclusivity for certain branded merchandise. Finally, consider the fact that the Target Center is a mere 0.4 mile walk from Target HQ. How much cost could Target reduce in corporate employee churn & payroll by offering perks for NBA game tickets & events with players? All of that is in addition to the “standard” naming deal benefits including TV and in-person branding.

A RobustPattern

Based on our analysis of Qualcomm and Target (and verified against a few other companies that outperformed but to a much lesser degree), we can define a clear set of properties that constitute a “good deal” when it comes to naming rights. If we then analyze our set of 98 companies and eliminate all companies that meet those “good deal” criteria, we find that the remainder systematically underperform in a significant way. That’s a pretty interesting result for anyone interested in long/short hedged strategies. It also means that if I personally held any Crypto.com stock in the private market, I’d dump it because its stadium deal doesn’t meet the “high quality” deal criteria. Complete data & results for this extended study, along with a model investment strategy based on it, will be included in my next issue of the Axiom Alpha Market Intelligence newsletter (a paid subscription for deep market data & analysis). For the more casual reader, you can subscribe to the Axiom Alpha Letter (of which this article is an example issue) for free!

Disclaimer: Nothing in this article should be considered investment or financial advice. This content is for information & educational purposes only. Neither Homology Group Inc. nor any of its representatives will be liable to you for any actions you take or don’t take based upon the information in this article or other Axiom Alpha content. Axiom Alpha is a brand name of Homology Group Inc.

How to Sell Your Company for $1 Billion & Pay ZERO Capital Gains Tax

“Kara sold her software company for $1.33 billion and paid ZERO capital gains taxes. I don’t mean the tax bill was deferred to a later year. I mean the tax bill was erased from existence. Permanently.”

Back in the good old days (1862-1986), the Homestead Act allowed U.S. citizens to claim up to 160 acres of government-surveyed land for free. Unfortunately that opportunity doesn’t exist anymore. However, something even better does: Opportunity Zones (OZs). That’s not hyerpbole either. Opportunity zone tax breaks ARE actually more valuable than getting 160 acres of undeveloped land, and I’m going to show you how.

People who have heard of opportunity zones before often have two misconceptions.

The first misconception is that opportunity zone tax loopholes are only useful to people who are already wealthy. That’s wrong. It will help if you have at least a few thousand dollars, but you certainly don’t need millions. In fact, opportunity zones are probably the most useful to ambitious people who want to create companies but haven’t started yet.

The second misconception is that the opportunity zone tax loophole is only useful for real estate investing. That’s also completely wrong. In 2019, the IRS published a 544 page document with painfully detailed commentary on all sorts of various things you can do with opportunity zones. That information made it very clear that many businesses and business owners (whether investors or founders) can benefit from opportunity zone tax breaks if they are willing to follow the relevant rules.

In fact, the very generality of opportunity zones sometimes confuses people. How can one tax rule be equally useful to Amazon, a Silicon Valley startup, a local ice cream shop, a crypto trader, a hotel investor, a one-woman services business, and an aspiring entrepreneur who hasn’t even created a company yet?

The answer is that there are actually a LOT of tax rules related to opportunity zones, most of which are unfamiliar even to professional investors. These rules are Legos that can be assembled to provide all sorts of different benefits to all sorts of different people and businesses. I’m going to teach you to wield these rules as a secret weapon to obliterate tax bills, get subsidized assets from the government, and destroy your competitors who aren’t using opportunity zone strategies.

This letter is different than my typical letters. It’s 5 times longer and 50 times more valuable. It’s a precise guide to opportunity zone strategies that can save you literal bricks of cash that would otherwise disappear to taxes. Some of the strategies are a bit complicated, but the cost reduction they provide is bigger than the differences that frequently dictate which of two competitor businesses survive. As Robert Frost once said:

“Two roads diverged in a yellow wood. At the end of one were the basic bitches, and at the end of the other was a qualified low-income census tract designated as an opportunity zone, and I took that less-traveled road.”

Maybe those weren’t his exact words, but it was something like that.

By the end of this letter, you will know:

How to pay zero taxes on a $1 billion cash exit

How you and your business can avoid paying taxes on 25 years worth of *realized* capital gains

How to eliminate depreciation recapture taxes

How a startup can raise more money, faster, at a higher valuation

How to find investors desperate to invest in your small business, even if you’re not growing like a VC-fueled Silicon Valley startup

Let’s dig in.

How opportunity zones work

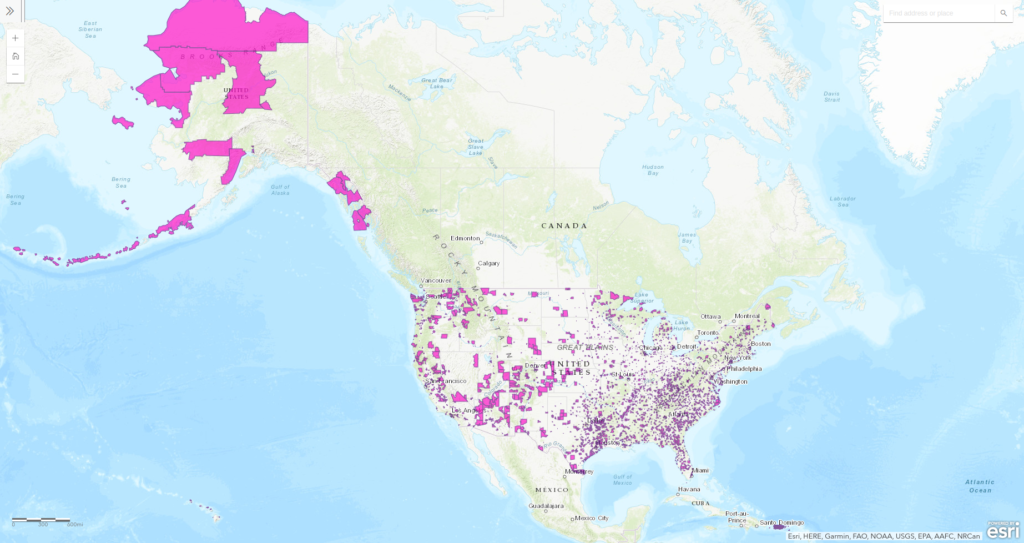

An opportunity zone is just a low-income census tract that has been designated as an opportunity zone by a state government. Here is a map showing all opportunity zones in the country:

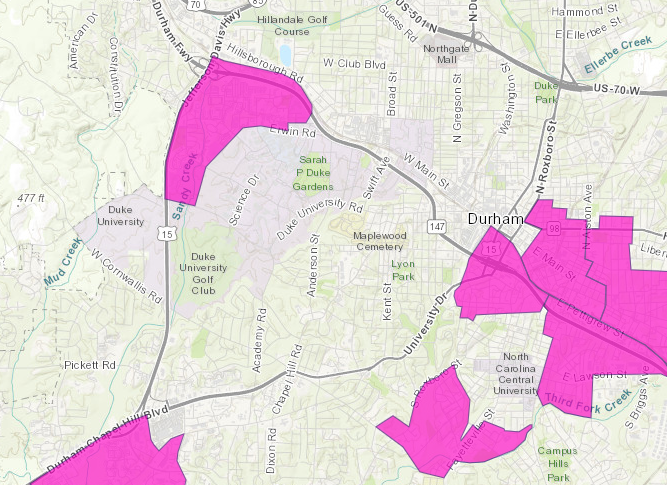

The various tax rules related to opportunity zones are all government incentives for investors and companies to come in and create jobs, infrastructure, and wealth in these areas. Some zones are vast swaths of barren land in the middle of nowhere. Others are run-down areas in the middle of cities. And still others are right next to universities where college student populations depress income levels even if the areas are developed. For instance, here is an opportunity zone located right next to Duke University in North Carolina:

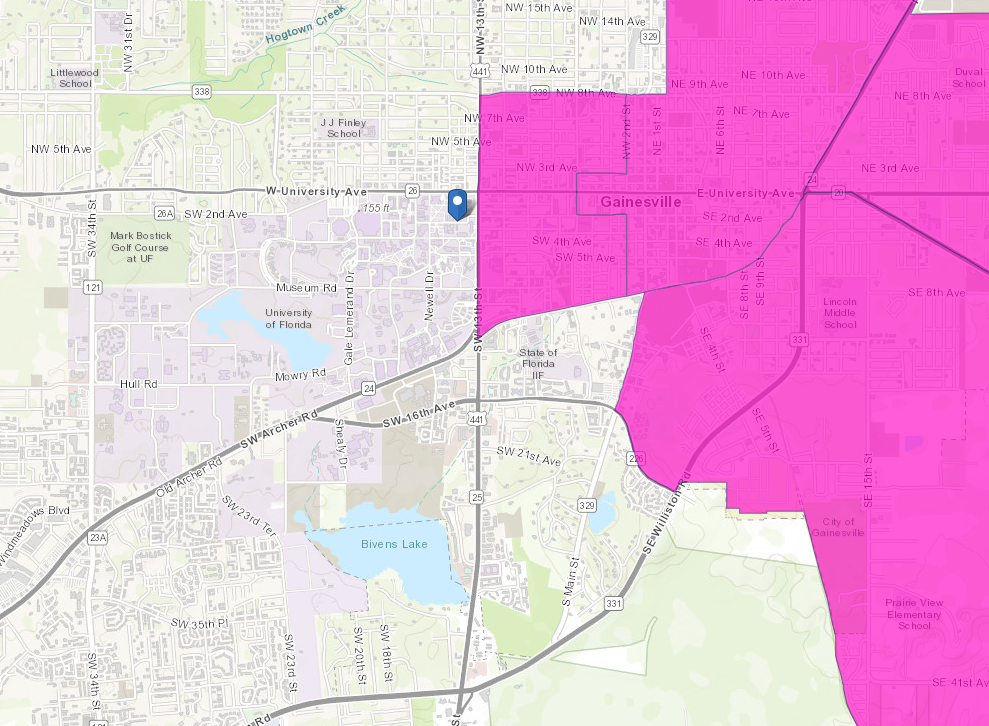

And here is a big block of opportunity zones right next the University of Florida:

The essence of the opportunity zone tax loophole is that if you reinvest capital gains into businesses or property located in an opportunity zone, then you can defer some taxes and eliminate other taxes altogether. However, there are certain strategies that will allow you to benefit from this loophole even if you don’t have any meaningful capital gains right now. I’ll explain how that works later in this letter.

The basic setup is that any person or company which can meet four sequential requirements will benefit from privileged tax treatment:

Sell property, stock, crypto, NFTs, or anything else that results in a capital gain before December 31, 2026.

Reinvest the amount of the capital gain (e.g. if you bought stock for $500 and sold it for $600, then reinvest the $100 gain) into a type of investment fund called a “qualified opportunity fund” (QOF) within 180 days of when the gain was realized. A QOF is a special-purpose business entity that must invest into businesses or property within one or more opportunity zones.

Hold your QOF investment(s) for at least 10 years.

Sell your QOF investment(s) before December 31, 2047.

If all four conditions are met, then you receive two tax advantages at different times.

The first tax advantage is a deferral of tax on the initial capital gains that you reinvested into the QOF. The deferral pushes that tax bill back until you file your return for 2026 (about 5 years from the time I’m writing this). In the meantime, those capital gains can be put to work in investments that go up in value. That brings us to the second tax advantage.

The second tax advantage is a complete elimination of capital gains tax on any increase in value of those QOF investments. Technically, this is accomplished by a law which resets the “tax basis” of the investment to “market value” when you sell. That should perk up the ears of anyone familiar with depreciation recapture because it means that you don’t have to ever repay depreciation deductions! More on that later though.

Example 1: simple QOF investment math

Bob has $2 million invested in the stock market. $1 million of that is unrealized capital gains. It doesn’t matter whether those are short or long term capital gains–either can be reinvested into a QOF.

Bob sells his entire stock portfolio in May 2022. If the gains are long-term capital gains, then Bob would owe $200k = 20% of $1M in capital gains tax for 2022 (if the gains were short term, that bill would be almost twice as much). However, Bob chooses to invest $1M in a qualified opportunity fund in August 2022. Since that is less than 180 days after he recognized his $1M gain, he has eliminated his entire $200k capital gains tax bill for 2022.

Over the next 5 years, Bob’s QOF investment goes up in value from $1M to $2M. He has to file 2026 taxes now, which means he owes his $200k tax bill. Note that it is still $200k, not $400k, despite the QOF investment doubling in value. For simplicity, I’ll assume Bob pays the $200k with money he has in a bank account outside the QOF. (There are ways to take tax-free distributions from a QOF to pay that $200k tax bill, but those would complicate our discussion more than is necessary.)

Bob continues to hold his QOF investments all the way until 2047 when he sells them for $6 million. That means over 25 years, his $1 million has turned into $6 million (a $5 million gain). If the long-term capital gains tax is still 20% in 2047, then Bob would normally owe $1 million = 20% of $5 million in taxes. However, because this gain was held for more than 10 years through a QOF, Bob owes ZERO dollars in taxes.

There is no deferral happening here. Bob never has to pay that million dollar tax bill — the tax bill is simply erased from existence as if Thanos had snapped his gauntleted fingers.

Example 2: the tax-free billion-dollar exit

Kara is an aspiring entrepreneur who wants to create a new word game app. She wants to put $1000 of her own money into the company to start it.

Kara could just transfer $1000 from her bank account to the business’s bank account. However, if her company becomes very successful and is eventually acquired, she would have to pay a huge amount in capital gains tax. So instead, Kara checks her Robinhood account. She’s been holding two shares of Tesla stock since right after the stock split in 2020 which means she’s sitting on $1120 of unrealized capital gains. She forms an LLC to serve as her QOF and deposits the $1120 into her new LLC bank account. Her LLC then forms a wholly-owned C corporation subsidiary which will be the startup that actually builds the new app. Importantly, she starts working at a coworking center located in an opportunity zone so that her C corporation immediately starts off as a QOZB (qualified opportunity zone business).

Kara’s company begins to grow. Over the next two years, she takes on one outside investor through another QOF which takes 20% of her corporation. She scales up to a team of 8 people. Five people work from her original coworking space (although now in a larger, dedicated office) and 3 people work remotely from another coworking space in a different opportunity zone. The app’s computing & data storage needs are supported entirely by cloud infrastructure rather than company-operated servers. By this time, the app is generating over $50 million / year in revenue.

Over the next 10 years, Kara’s company grows by acquiring other game & puzzle apps run by lean teams and relocating their teams to office spaces in opportunity zones. By the end of this period, the company is bringing in over $500 million in annual revenue. At this point, she decides to sell her company. She asks Goldman Sachs to look for buyers and eventually gets an all-cash offer from the New York Times for $1.33 billion. She takes the deal.

At the time of sale, 20% of the corporation has been sold to an outside investor and another 5% has been given to various employees over the years. That leaves Kara (through her QOF) with a 75% stake in the corporation.

75% of $1.33 billion is $1 billion: Kara has a $1 billion exit. Ordinarily, Kara would owe long-term capital gains taxes on that entire amount of $1 billion minus her $1120 of initial capital. At today’s long-term capital gains rate of 20%, that’s a two hundred million dollar tax bill! If Biden succeeds in raising the long-term capital gains rate to 39%, that would be a $390 million tax bill! However, since Kara’s initial investment was through a QOF, she owes ZERO TAXES.

This strategy is applicable to the MAJORITY OF STARTUPS. Most modern tech startups are asset-light internet companies or internet service agencies which can easily comply with opportunity zone business requirements. Most media businesses (including social media, newsletter & influencer businesses) are also flexible enough to comply with opportunity zone business requirements. Most e-commerce businesses can qualify. Many small local businesses can qualify if they are willing to be flexible on location. Real estate businesses can often qualify. Even some asset-heavy businesses such as manufacturers can qualify.

Let’s talk about exactly how to execute on this. (Also, this article is a real issue of the Axiom Alpha newsletter so if you want to learn about more financial strategies like this, subscribe to join our community of entrepreneurs & investors!)

How to create a QOF

A qualified opportunity fund (QOF) is a business entity used for a specific purpose and which satisfies certain conditions. Here are the five requirements and best practices to create your own qualified opportunity fund:

The QOF should be an LLC, LP, or C corporation. If it is an LLC or LP, then it must have at least two members/partners (single-member LLCs are not allowed).

It is incorporated in a U.S. state, DC, or a U.S. territory. If the business is incorporated or formed in a U.S. territory (rather than a state or DC), then it must be formed for the purpose of investing in opportunity zones only within that territory.

The business entity may be a pre-existing business entity. However, to minimize the chance of an audit, it’s highly recommended to form a new entity and include in its formation document that the entity is formed for the specific purpose of investing in qualified opportunity zone property.

The business entity must elect QOF status by filing form 8996 annually with its tax return.

At least 90% of its assets must be “qualified opportunity zone property” which can be any combination of (1) stock in a QOZB corporation, (2) partnership interest in a QOZB structured as an LLC or other pass-through partnership entity, and/or (3) qualified opportunity zone business property. However, this requirement doesn’t take effect immediately which means the QOF has time to find qualifying investments without rushing. Additionally, the 90% rule temporarily loosens if you deposit more cash into the QOF.

What is “qualified opportunity zone business property” (QOZB Property)?

(I know… I’m sorry for the word salad. Blame Congress.)

Qualified opportunity zone business property is tangible property that (1) has been or will be owned or leased (starting in 2018 or later) by a corporation or partnership, (2) is used in the active business of such corporation or partnership, and (3) falls into one of the allowed categories. The most common allowed categories are the following:

OZ real estate that you purchase and then “substantially improve” within 31 months. In this context, substantial improvement means spending as much in renovations as the cost of the original real estate minus the land value. Note: the 31 month requirement can be extended for government-caused permitting delays.

New construction real estate in an OZ.

Leased real estate in an OZ. You must have started leasing the property no earlier than 2018. Nobody is required to “substantially improve” such leased property in order for it to qualify as QOZB Property.

OZ real estate that you purchase from a local government who obtained the property through an involuntary transaction (e.g. due to nonpayment of tax by the homeowner).

OZ real estate that you purchase after it has been vacant for several years.

Any type of (new or used) machinery, equipment, or other tangible property which (1) can be depreciated or amortized and (2) has never been used in that particular opportunity zone by any business before. The property can be either owned or leased. There are even several safe harbor rules to include in this definition certain property which spends substantial time outside of an OZ. (e.g. a company truck which is normally parked at an office in an OZ but which is frequently driven out of the OZ for business).

Inventory produced by the business.

Some examples of property that are NOT qualified opportunity zone business property are:

Undeveloped land in an OZ which is not put to any significant active use. For example, someone purchases land primarily just to benefit from appreciation of the land over time, but they also let people pay $10 to park there during football games. (This fails to be QOZB Property because it fails requirement 2 above — it isn’t being used in an “active” business.)

OZ real estate leased out under a triple net lease. The IRS reasons that triple net leases are not an “active” business since the entire burden of property ownership is essentially transferred to the lessee.

A used commercial riding lawnmower bought from a landscaping company currently located in the same opportunity zone.

How to meet the QOF partnership requirement

Earlier, I mentioned that single member LLCs cannot be QOFs which is an annoyance to many people. However, the solution is very simple. Find a friend (or form an empty shell corporation if you have no friends) to buy a tiny fraction of the QOF (e.g. 0.01% or $1 or something like that). Wa-La — you now have a 2-member LLC which will be taxed as a partnership rather than a disregarded entity. I didn’t mention this technicality in my example of Kara, but she would have had to do this for her QOF.

How to create a QOZB

To create a qualified opportunity zone business, you’ll need to create a business entity that meets seven requirements:

The QOZB should be an LLC, LP, or C corporation. If it is an LLC or LP, then it must have at least two members/partners (single-member LLCs are not allowed).

It is an active business. Most “normal” businesses are active businesses. However, as previously mentioned, leasing real estate under a triple-net-lease is not.

At least 50% of the total gross income is derived from the conduct of a business in a qualified opportunity zone. There are several ways this requirement can be fulfilled (only one needs to be met): (a) at least 50% of the hours worked by partners, contractors, and employees could take place in an OZ, (b) at least 50% of compensation to partners, contractors, and employees could be for services performed within an opportunity zone, (c) the tangible property and management operations within an opportunity zone are necessary for the generation of at least 50% of the gross income of the business, or (d) the “facts and circumstances” (legal jargon) dictate that at least 50% of gross income is derived from active opportunity zone business operations.

At least 40% of the intangible property (e.g. patents, trademarks, etc) must be actively used inside a qualified opportunity zone. This is a slightly gray area since it’s difficult to assign a location to something like the use of a patent. In general though, things like using a trademark on the website of a business that has its office and employees in an OZ will probably count towards the 40%. On the other hand, a patent that was developed by a company operating outside of any OZ and which is later acquired by a QOZB might not count towards the required 40%.

At least 70% of the tangible property owned or leased by the business must be qualified opportunity zone business property. (We covered the definition of qualified opportunity zone business property in the previous section on QOFs).

No more than 5% of a QOZB’s assets can be “nonqualified financial property”. Nonqualified financial property includes most types of financial assets such as stocks and bonds but excludes cash, loans with a term of 18 months or less, and accounts receivable acquired in the ordinary course of business. There are some additional details around this rule, but they aren’t that important to most businesses. If you want to create any sort of business that relates to finance though, you’ll need to carefully look at all details.

The business is not a “sin” business or a company that leases property to a “sin” business. Sin businesses are: any private or commercial golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack or other facility used for gambling, or any store the principal business of which is the sale of alcoholic beverages for consumption off the premises.

Example 1

A landscaping company is set up as a C corporation. The company rents a small office with an adjacent fenced area of land where they store all of their trucks, driving lawn mowers, and other equipment. The office & land are inside an opportunity zone. All administrative work is done from the office. Every day, employees come pick up equipment and use it to service customers both inside and outside of the opportunity zone before returning the equipment at the end of the day. The business is a QOZB (unless it does something unexpected like buy a million dollars of stock which might jeopardize the 5% limit on nonqualified financial property).

Example 2

Amanda & Mike live together in an opportunity zone. They decide to create a Youtube channel together. They create a 2-member LLC (they are the two members) to run their Youtube business. They operate from a home-based office and earn revenue through youtube ads, sponsors, and Amazon affiliate sales. The business is a QOZB.

Example 3